The first victim of the perfect storm – an economic slowdown that makes people buy less, high interest rates that make debt more expensive, and inflation that eats away at our money – is the real estate industry. In the language of accountants, such a storm ensures that revenues will fall (fewer sales) and that expenses will rise (including construction inputs And also about the heavy financing.) As a result, it is suddenly not clear that the current flow – from sales, renting, realization of assets, etc., will be able to service the burgeoning debt. With all due respect to the enormous profits that many companies will continue to present in the financial statements due to the “increase in the value of the assets in the books” that produce For those competent appraisers, this is not real money going into the company’s coffers. If the value of the land has doubled on paper, it won’t help pay the interest.

● Prices will rise sharply: the apartment renters will be the biggest victims of the interest rate increases

● Apartment prices are falling, and the Ministry of Finance is demanding a change in the minimum entrepreneurial profit in building construction

● Dodo Zevida is on his way out of the Mavena group even though his value has doubled under him

Therefore, the real estate industry led the declines in the stock market on Wednesday as well. Above all, the leveraged entrepreneurs – the Tel Aviv Construction Index which fell by more than 1% (an 11% drop from the beginning of the month), but the other real estate indices also fell by a similar rate.

There is no restrictive regulation in the entrepreneurial market

There is no sector as mired in debt as the real estate industry. In 2022, real estate companies raised NIS 30 billion in bonds on the stock exchange – 36% of the total raised here. In January 2023, they raised another NIS 2.1 billion. This is not necessarily unusual, as most Israelis who buy an apartment will not do so without a mortgage, but it is very dangerous. And unlike the mortgage market, there is no similar regulation in the entrepreneurial market (which limits, for example, mortgage takers in the amount of credit according to the value of the property, disposable income, etc.). In recent years, the cheap and generous money encouraged quite a few entrepreneurs to take financing even at a rate of 90% or 100% of the deal. As long as prices went up, and they did for 15 years, it paid off big for them.

But if the wheel turns, and there are too many such signs, the panic in the market is obvious. Of course, when it comes to huge debts raised through bonds, investors who cannot be asked for a slight deferment or even a slight discount until the anger from the market passes – which is certainly possible to ask for and receive from the bank, for example, which does not want to see the company enter into a spiral and debt settlements.

At the same time, it is important to remember that quite a few entrepreneurs completed the necessary equity capital for the transaction from non-bank credit companies, which flourished together with the zero interest rate in the economy, and which usually provided credit at particularly alarming interest rates (in the absence of significant collateral on the money raised).

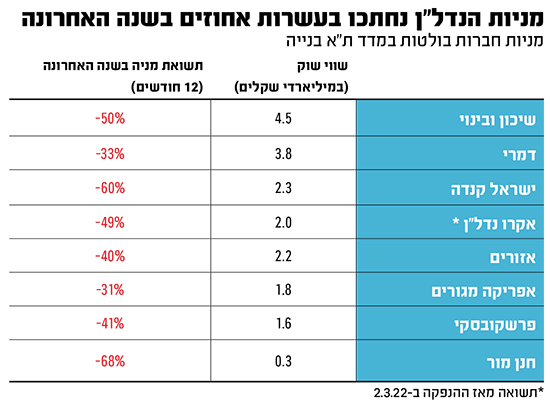

Exactly one year ago, for example, Akro arrived on the Tel Aviv Stock Exchange, riding on the residential real estate trend. The company raised half a billion shekels on the stock exchange in February 2022 and began trading at a value of 3.4 billion shekels – which jumped to 4 billion on the first day of trading. The enthusiastic investors heard from the company that it is expected to have a gross profit of NIS 6 billion, from spectacular projects that are located, for example, on Vysotsky, Weizman, Sharet and MAZA streets, the hottest heart of Tel Aviv.

A year later, the company’s stock fell another 2% on Wednesday, down 12.5% since the beginning of the month. Its value already touches NIS 2 billion – 50% of the issue price. In February 2023, it becomes clear that investors look less at the line of expected profit, but more at the line of liabilities. The one that includes a debt of 4 billion shekels, of which 1.8 are linked to the prime interest rate and another 250 million shekels linked to the index.

The Hajjaj company, another entrepreneur that operates mainly in the heart of the demand area, fell by 18% since the beginning of the month. This time, too, the investors stopped being flattered by the promises of an “expected profit of NIS 3.7 billion”, from projects in places like Babylon, Einstein, Shadl and Ibn Gvirol in Tel Aviv, and are even more troubled by various debts totaling NIS 1.9 billion.

If the market continues to be negative, it will be much more difficult to service the huge debt or raise new debt for it – when the company’s current bonds are trading at a (gross) yield of 7%.

At the same time, the Israeli real estate companies operating abroad were supposed to be the biggest beneficiaries of the devaluation of the shekel exchange rate. If the dollar and the euro jump, their incomes and the value of their assets jump accordingly. If the Israelis are afraid to put all their eggs in the local basket, in view of the storms in the economy and in general, they will be happy to invest in the old companies that operate mainly overseas.

The rapid shift of the investors from the rosy forecasts towards the huge debts and investments of the same companies is particularly noticeable among the local yielding real estate sector. To the companies that have become accustomed to updating them every quarter on the growth in the value of the assets, and with them, of course, on the growth of the huge (accounting) profits on the bottom line. This, in time that the incomes themselves from rentals have increased in a measured way several times. And the one who, by the way, was alarmed by this very recently is the Bank of Israel, which this month published a study on the performance of the public yielding real estate companies, which discovered, not surprisingly, that “the value of the properties embodies an expectation of an increase in value, and not necessarily a real increase in rents.” .

The Bank of Israel specifically stated that they “anticipate that there will be a decrease in the reported profitability of the companies in the field, and even the possibility of an increase in the reported leverage rates of some of the companies.” At the same time, as is the way of the Bank of Israel, which prefers to be especially careful and grasp the rope at both ends, they emphasized that “this is a quasi-bubble behavior, and not exactly a bubble.” We didn’t really understand either.

The market internalized the message. Even yielding real estate giants such as Azrieli or Melisron, for example, have decreased since the beginning of the year by 13-14%. Also because of the huge debts, most of them linked to the consumer price index, which are intended to finance, among other things, their huge venture – 664 thousand new square meters that Azrieli and 280,000 square meters of Melisron are now building and planning. If the global and local economy slows down, investors fear that even the real estate giants will find it difficult to occupy all these vast areas.

“Shekel immune” shares are also getting wet

And here, it is important to note that the deluge that has washed over the Tel Aviv Stock Exchange in recent days fairly dampens those “shekel immunity” as well. The real estate index “Yields Abroad”, which includes the Israeli companies that invest in real estate for rent mainly abroad (residential, commercial, offices, etc.), has decreased since the beginning of the month by more than 7%. On Wednesday it fell by about 2%, after a drop of almost 3% on Tuesday.

Electra Real Estate is an excellent example of the negative trend in the entire real estate sector, which is not only related to the weakening shekel. The company owns more than 35,000 apartments and houses for rent in 56 cities across the US, which pay it rents of about 70 million dollars each quarter. The same dollar that has soared in recent days, makes the company’s shekel debt much friendlier (only in September Last, for example, she raised another NIS 151 million in bonds on the Tel Aviv Stock Exchange), which did not help the sentiment in the stock.

On Wednesday, the company’s stock fell by about 2%, completing a decline of more than 12% since the beginning of February. Because when investors dump stocks, and when the public and the institutional bodies decide it’s worth staying away from the Israeli stock market, no one is immune. Even if he only speaks in foreign language.