2024-04-29 11:03:53

Financial analysis… Corporate delinquency rate also rises

While the amount of loans received by companies from financial institutions reached 1,900 trillion won, the proportion of loans from ‘vulnerable companies’ that lacked the ability to repay principal and interest was found to have increased to the level during the 2008 global financial crisis. The sense of crisis is growing as the delinquency rate of corporate loans, including those in the construction industry, which has been hit hard by the aftermath of high interest rates, has also risen sharply over the past year.

According to ‘Domestic Corporate Debt Status and Implications through Comparative Analysis by Crisis and Industry’ published by the Korea Institute of Finance on the 27th, the balance of corporate loans from domestic financial institutions as of the end of last year was KRW 1889.6 trillion. Corporate loans increased by an average of 10.8% every quarter from the end of 2019, when the novel coronavirus infection (Corona 19) spread, to the end of last year. This is about twice as high as before COVID-19 (March 2010 to the end of 2019, 5.3%).

The Korea Institute of Finance selected vulnerable companies with poor repayment ability by considering interest coverage ratio, loan repayment ratio, debt/liquidity ratio, etc. As a result, their borrowing ratio was found to be lower than that of the 1997 foreign exchange crisis, but close to or slightly higher than that of the 2008 financial crisis.

Senior Research Fellow Shin Yong-sang said, “The high interest rate situation has continued since the second half of last year (July to December), and the domestic market, including real estate, is still in recession,” and added, “It is time to monitor whether risk-related indicators will further worsen.” did.

39% of corporate loans, a sharp increase of KRW 567 trillion in 4 years, are in the real estate-construction industry

There are many non-bank loans such as Saemaeul Geumgo.

Construction costs are soaring due to continued high interest rates.

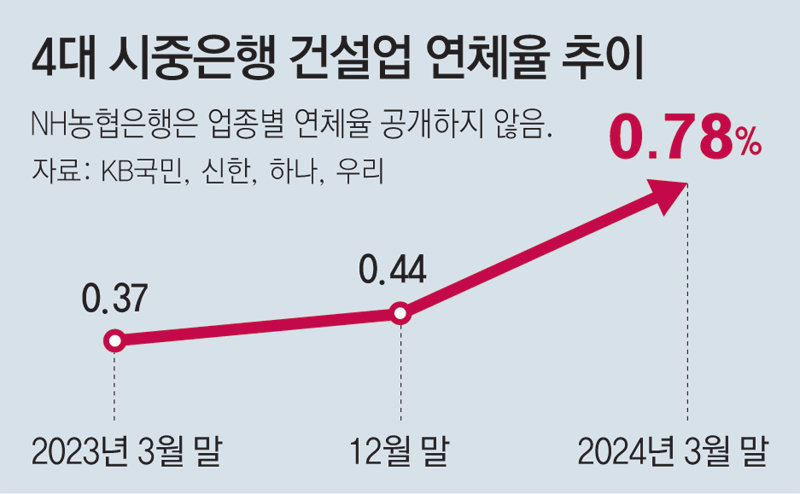

Delinquency rates in the construction industry at the four major banks doubled in one year

Domestic companies were found to have received additional loans worth 570 trillion won over the four years until the end of last year following the novel coronavirus infection (Corona 19). Of these, approximately 40% was the increase in loans to the low-productivity real estate-related industry.

According to the Korea Institute of Finance on the 28th, loans across all domestic industries increased by 567.4 trillion won from the end of 2019 to the end of last year. By industry, the increase in the real estate industry (KRW 175.7 trillion) and construction industry (KRW 44.3 trillion) accounted for 38.8% of the total. In particular, in the case of the real estate industry, non-bank loans were found to have doubled in size since COVID-19. Shin Yong-sang, senior research fellow, explained, “The rapid increase in corporate loans from mutual financial institutions such as Saemaeul Geumgo led the increase in the non-bank sector.”

However, as the U.S. Federal Reserve (Fed) began to implement intensive austerity measures starting in March 2022 and the high interest rate trend was prolonged, construction industry loans, especially real estate project financing (PF), quickly became non-performing. As of the end of March, the average delinquency rate in the construction industry for the four major banks, including KB Kookmin, Shinhan, Hana, and Woori, was 0.78%, up 2.1 times from a year ago (0.37%). In the case of Shinhan Bank (1.18%) and Hana Bank (1.13%), the delinquency rate in the construction industry exceeded 1%. An official from a commercial bank explained, “Not only Taeyoung Construction but also some local construction companies entered workouts (corporate improvement work), resulting in an increase in non-performing loans and an increase in the delinquency rate.”

As the Fed’s interest rate cut was delayed, the risk of real estate PF insolvency spreading increased. Previously, the Bank of Korea predicted in its March monetary and credit policy report, “In a situation where the sales market is contracted, the financial risk of the construction and real estate industries is likely to increase as the cost burden of continued high interest rates and rising construction costs increases.” .

Although financial authorities are encouraging banks and second-tier financial institutions to resolve non-performing loans, the industry is concerned that new non-performing loans are accumulating faster. As of the end of the first quarter of this year (January to March), the ratio of non-performing loans (non-performing loans overdue for more than three months) of the five major commercial banks averaged 0.28%, up 0.01 percentage points from the same period last year. An official at a bank said, “The ratio of non-performing loans is at the highest level in three years, so we are keeping our guard up internally.”

Kim Sang-bong, a professor of economics at Hansung University, said, “Government measures such as interest reductions are taking place one after another, but they are not supported by the economic situation and improvements in corporate management.” He added, “It is inevitable that the delinquency rate and non-performing loan rate will rise, especially for small and medium-sized businesses.”

Reporter Kang Woo-seok [email protected]

-

- great

- 0dog

-

- I’m so sad

- 0dog

-

- I’m angry

- 0dog

-

- I recommend it

- dog

Hot news now

2024-04-29 11:03:53