The American labor market has demonstrated a surprising level of resilience, as a US jobs surge unexpectedly in March defied the prevailing gloom surrounding geopolitical instability and tightening policy. The growth comes at a time when many analysts expected the combined weight of international conflict and domestic economic pressures to stifle hiring.

This unexpected uptick in employment suggests that the domestic economy may be more insulated from external shocks than previously feared. But, the surge arrives amidst a high-stakes tug-of-war between the White House and the Federal Reserve over the trajectory of interest rates and the broader strategy for national economic growth.

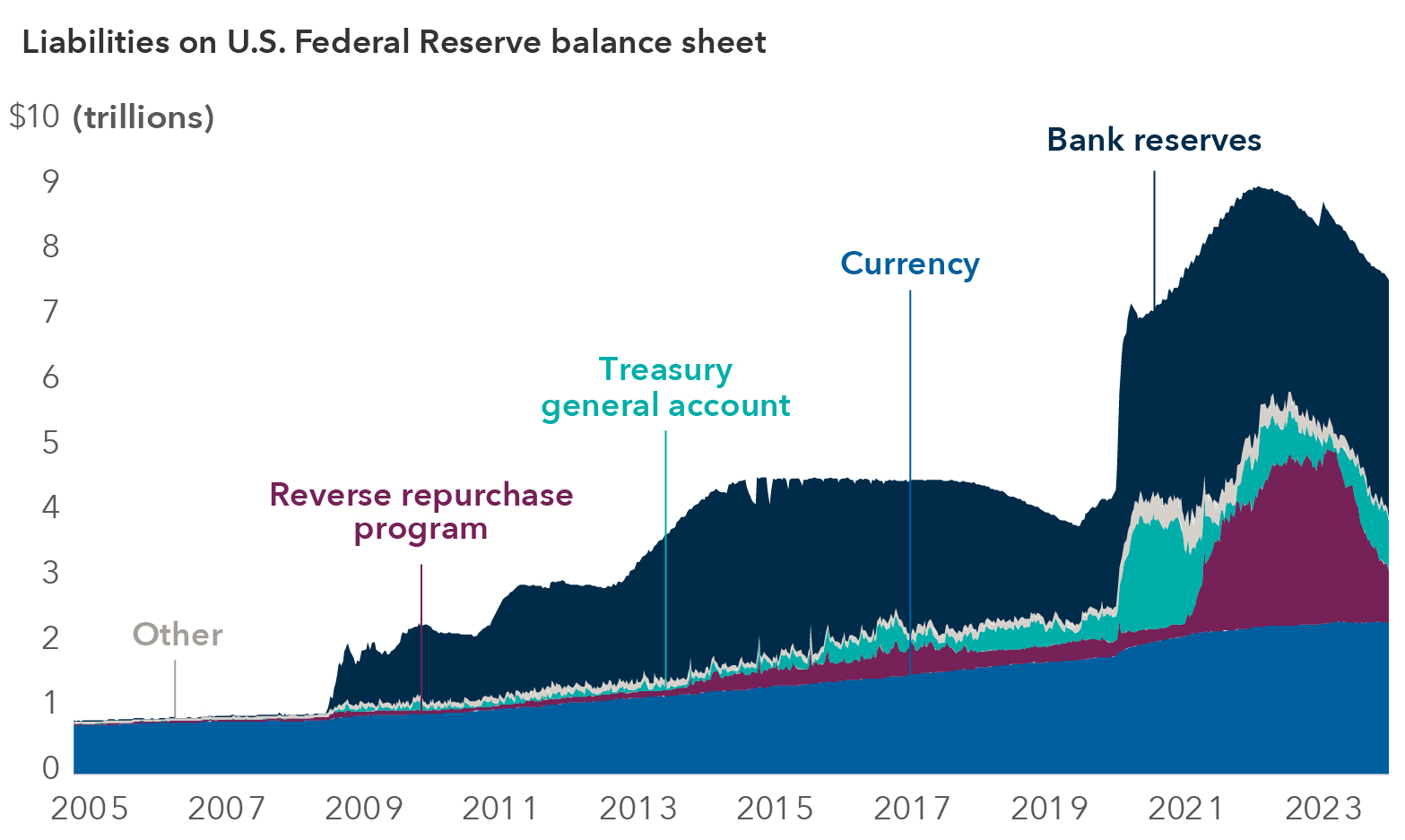

For the Federal Reserve, the data presents a complex puzzle. While the job market remains robust, the central bank continues to grapple with an inflation target of 2% that remains elusive. This tension has created a precarious environment for policymakers who must decide whether to prioritize immediate growth or long-term price stability.

The Federal Reserve’s Balancing Act

President Donald Trump has consistently advocated for the Federal Reserve to lower borrowing costs aggressively. From the administration’s perspective, a sharp reduction in interest rates would lower the cost of capital for businesses, sparking further investment and accelerating economic expansion.

Yet, Fed Chair Jerome Powell has maintained a more cautious stance. Powell has characterized the current state of the economy as being in a delicate balance, noting that while job creation has been muted in certain sectors, the economy has avoided widespread layoffs. The primary obstacle to rate cuts remains the persistence of inflation, which continues to track above the bank’s 2% goal.

As a former financial analyst, I have seen this dynamic play out before: the clash between political desire for short-term stimulation and the central bank’s mandate for systemic stability. If the Fed lowers rates too quickly while inflation is still high, it risks a “wage-price spiral” that could erode consumer purchasing power more severely than high borrowing costs ever would.

Geopolitical Volatility and the Iran Conflict

Adding a layer of uncertainty to these labor dynamics is the ongoing war in Iran. While the March employment figures were positive, economists warn that the full impact of the conflict may not yet be reflected in the data. The Bureau of Labor Statistics typically conducts its employer and household surveys around the middle of the month, meaning the March report was finalized only a few weeks after the conflict began.

The primary concern for the US economy is not the conflict itself, but the potential for a sustained spike in global oil prices. Energy costs act as a regressive tax on both businesses and consumers; when oil prices climb, the cost of transporting goods and producing food rises almost immediately.

This “cost-push inflation” can lead to a wider economic slowdown. As households spend more on gasoline and groceries, their discretionary spending on other goods and services drops, which could eventually lead businesses to freeze hiring or begin cutting staff to protect margins.

Domestic Policy Headwinds

Beyond the conflict in Iran, the labor market is navigating a series of internal policy shifts that have contributed to a static environment in several key industries. A concerted crackdown on immigration and the implementation of various tariffs have created friction in the supply chain and labor availability.

Tariffs, while intended to protect domestic industry, often increase the cost of raw materials for manufacturers, squeezing the very businesses the policies aim to support. Similarly, restrictive immigration policies can lead to labor shortages in agriculture, construction, and hospitality, forcing employers to either raise wages—which feeds back into inflation—or leave positions unfilled.

The following table outlines the competing forces currently shaping the US economic landscape:

| Growth Drivers | Economic Headwinds |

|---|---|

| Unexpected March jobs surge | Inflation above 2% target |

| Pressure for lower borrowing costs | Rising oil prices due to Iran conflict |

| Resilient consumer demand | Immigration restrictions & tariffs |

What So for the Average Worker

For the average job seeker, the March surge is a positive signal, suggesting that companies are still willing to take on recent talent despite the uncertainty. However, the “delicate balance” Powell describes means that job security may remain fragile in sectors most sensitive to energy prices and import costs.

The real test will be whether this hiring momentum can survive a prolonged period of high energy costs. If oil prices remain elevated, the “unexpected surge” of March may be viewed in hindsight as a final burst of momentum before a geopolitical cooling effect takes hold.

Disclaimer: This article is provided for informational purposes only and does not constitute financial, investment, or legal advice.

The market now looks toward the next monthly employment report from the Labor Department to determine if the March surge was an anomaly or the start of a sustained trend. This upcoming data will be critical in determining whether the Federal Reserve shifts its stance on borrowing costs or remains steadfast in its fight against inflation.

Do you reckon the Fed should prioritize job growth or inflation control in the current climate? Share your thoughts in the comments below.