For millions of drivers, the trip to the gas station has become a source of monthly anxiety. As global crude oil markets fluctuate and seasonal demand shifts, the cost of filling a tank often feels like a variable that consumers simply cannot control. Although there is no magic switch to lower the price per gallon at the pump, financial stability often comes down to a simple equation: offsetting unavoidable costs with strategic savings elsewhere.

One of the most effective ways of offsetting rising gas prices is by auditing fixed vehicle expenses—specifically auto insurance. Because insurance premiums are subject to “price optimization,” where companies may raise rates for loyal customers who rarely shop around, many drivers are overpaying for coverage they no longer need or could find cheaper elsewhere.

By treating car insurance as a flexible cost rather than a fixed one, drivers can often uncover monthly savings that effectively neutralize the sting of higher fuel costs. This approach moves the conversation from “how do I pay for gas” to “how do I optimize my total cost of vehicle ownership.”

The volatility of the pump

Gasoline prices are influenced by a complex web of factors, including geopolitical instability, refinery capacity, and the cost of Brent and West Texas Intermediate (WTI) crude oil. When these benchmarks rise, the impact is felt almost immediately at local stations.

For the average commuter, a 50-cent increase per gallon can translate into an additional $20 to $40 in monthly spending, depending on the vehicle’s fuel efficiency and the distance traveled. Because these costs are non-negotiable, the most sustainable financial response is to find a “buffer” in the household budget.

Why insurance is the ideal offset

Unlike fuel, which is a commodity with a market price, auto insurance is a service with high price variance. Two drivers with identical profiles, driving the same car in the same zip code, can see vastly different premiums depending on the provider. This disparity exists because insurance companies use proprietary algorithms to assess risk and predict customer churn.

According to the Insurance Information Institute, factors such as credit scores, driving history, and even the type of vehicle significantly impact premiums. However, the simple act of comparing quotes often reveals that a driver is paying a “loyalty penalty”—a higher rate maintained because the insurer assumes the customer is unlikely to switch.

When a driver switches providers or renegotiates their policy, the savings can often exceed the monthly increase in fuel costs. For some, this can mean saving $30, $50, or even $100 per month, effectively making the increase in gas prices a non-issue for their monthly cash flow.

Calculating the potential impact

To understand how this works in practice, consider a driver who sees their monthly fuel expenditure rise due to market volatility. By auditing their insurance, they can create a financial wash.

| Expense Item | Previous Monthly Cost | New Monthly Cost | Net Change |

|---|---|---|---|

| Fuel (Gasoline) | $120 | $150 | + $30 |

| Auto Insurance | $110 | $75 | – $35 |

| Total Vehicle Spend | $230 | $225 | – $5 |

Steps to reduce insurance premiums

Lowering your insurance bill requires more than just a quick search; it requires a strategic review of your coverage. To maximize savings, drivers should focus on the following areas:

- Reviewing Deductibles: Increasing a deductible from $500 to $1,000 can significantly lower the monthly premium, provided the driver has enough emergency savings to cover the higher out-of-pocket cost in the event of a claim.

- Evaluating Coverage Levels: For older vehicles with low market value, maintaining full collision and comprehensive coverage may no longer be financially logical.

- Bundling Policies: Combining auto insurance with homeowners or renters insurance often triggers a multi-policy discount.

- Updating Mileage: With the rise of remote perform, many drivers are traveling fewer miles than they were three years ago. Updating this information with an insurer can lead to lower rates.

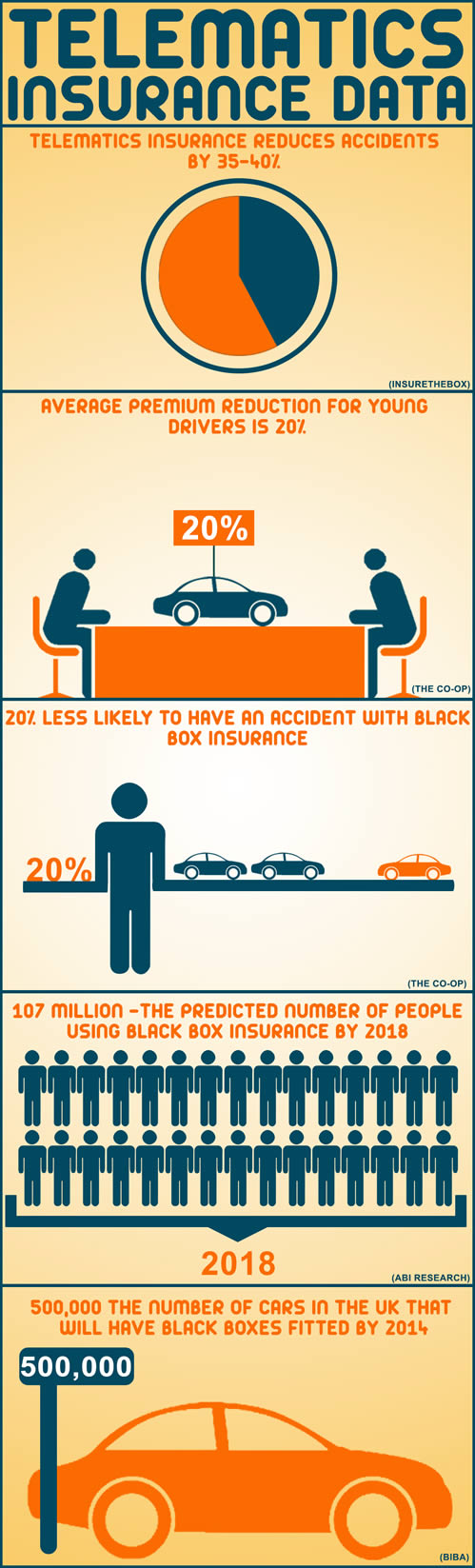

The role of telematics

Many modern insurers now offer telematics programs—apps or plug-in devices that monitor driving behavior. While some drivers are wary of the privacy implications, those with safe driving habits can often secure substantial discounts that further offset other vehicle expenses. These programs reward low speeds, smooth braking, and fewer nighttime trips.

The broader economic context

This strategy of “budget balancing” is a microcosm of how households are currently dealing with broader inflationary pressures. When one essential cost rises, the only way to maintain a standard of living without increasing debt is to aggressively prune other expenditures.

While shopping for insurance is a one-time or annual event, the savings it provides create a recurring monthly surplus. This transforms a volatile expense like gasoline into a manageable part of a larger, optimized budget.

Disclaimer: This article is for informational purposes only and does not constitute professional financial or legal advice. Insurance rates and availability vary by state and individual profile.

Looking ahead, energy analysts are monitoring upcoming OPEC+ production quotas and refinery maintenance schedules for the coming quarter, which will likely dictate the next major shift in pump prices. Maintaining a lean insurance policy remains one of the few proactive steps drivers can take to protect their wallets from these global shifts.

Have you found a way to lower your monthly vehicle costs? Share your experience in the comments below or share this guide with someone looking to save.