UBS has seen its market risk-weighted assets (RWAs) slide to their lowest level in six quarters, dropping below benchmarks set before the industry-wide shift toward stricter trading book regulations. This decline marks a pivotal moment for the Swiss banking giant as it navigates a new era of capital calculation.

According to recent financial data, the bank’s market risk charges plummeted by 15.8% in the fourth quarter of 2025. This sharp contraction brings the total market RWAs down to $23.8 billion, a figure that underscores a significant lean in the bank’s risk profile following the adoption of new regulatory frameworks.

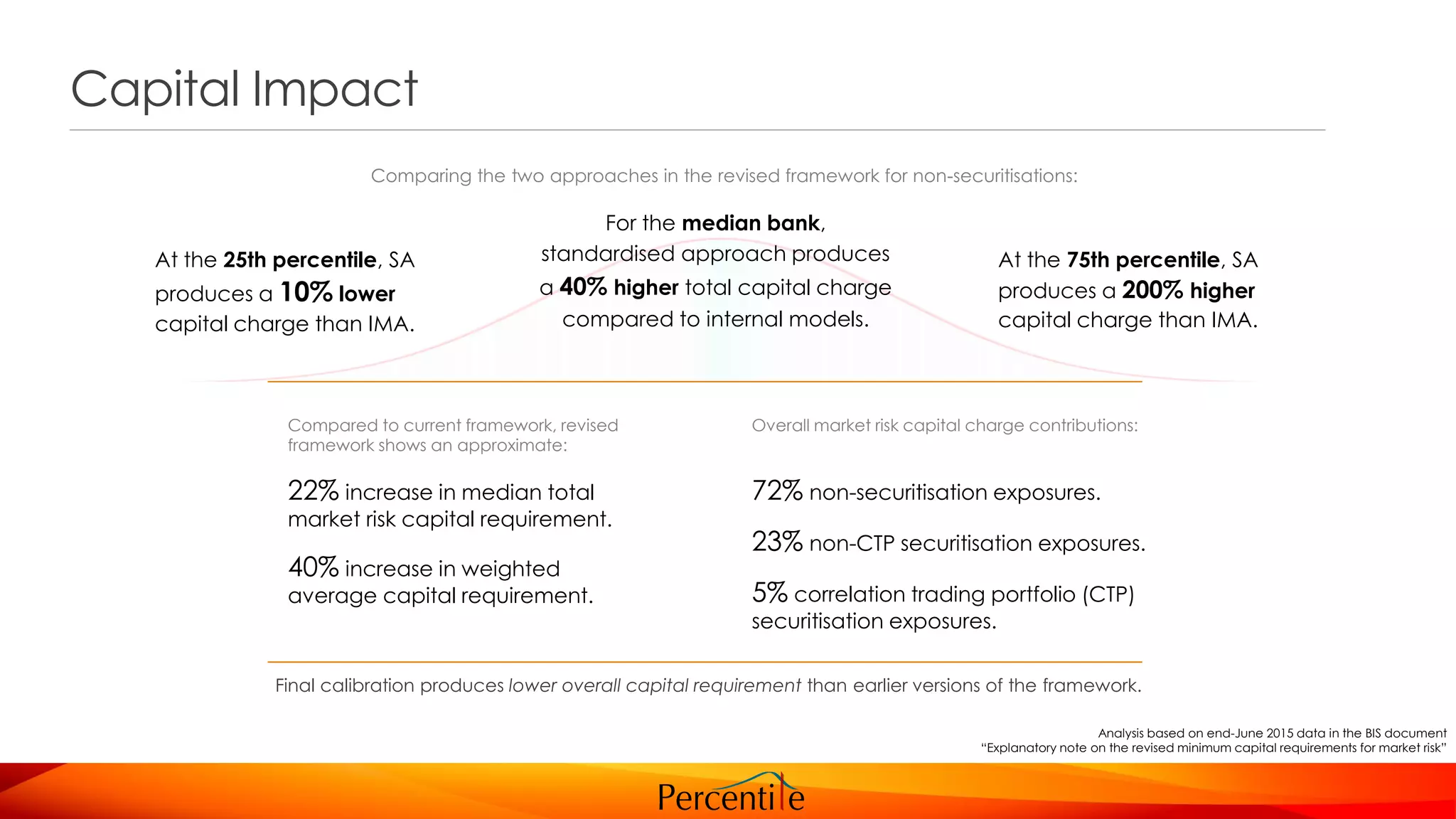

The current figures represent the lowest RWA levels since the second quarter of 2024, when the bank reported $22.5 billion. However, that earlier low was achieved under a different regime—a hybrid system that blended internal models with standardised formulas. The current drop is more notable because it occurs under the Basel III revised standardised approach, which became the mandatory calculation method on January 1, 2025.

Decoding the Shift to the Revised Standardised Approach

To understand why this drop matters, one must first understand the concept of risk-weighted assets. In plain English, RWAs are not the actual dollar amount of a bank’s investments, but rather those investments adjusted for risk. If a bank holds a “safe” asset, the risk weight is low; if it holds a volatile derivative, the weight is high. The resulting RWA figure determines how much capital the bank must hold in reserve to prevent a collapse during a market crash.

For years, large banks like UBS relied heavily on “internal models”—essentially their own mathematical formulas—to prove to regulators that their risks were lower than the standard rules suggested. This often allowed banks to hold less capital.

The transition to the revised standardised approach, often associated with the Fundamental Review of the Trading Book (FRTB), was designed to eliminate the inconsistencies of those internal models. By forcing banks to use a more uniform, regulator-approved formula, the Basel Committee aimed to make the global banking system more transparent and stable.

For UBS, the fact that its market RWAs have fallen to $23.8 billion under this more rigid system suggests a deliberate optimization of its balance sheet. The bank is effectively achieving a leaner risk profile even while playing by a stricter set of rules.

The Impact on Capital Efficiency

The 15.8% drop in risk charges isn’t just a statistical curiosity; it has direct implications for how the bank operates. When RWAs decrease, the “denominator” in the bank’s capital ratio shrinks. This typically results in a higher Common Equity Tier 1 (CET1) ratio, which is the gold standard for measuring a bank’s financial strength.

A higher capital ratio gives UBS several strategic advantages:

- Increased Lending Capacity: With lower capital requirements for market risk, the bank can potentially deploy more capital into growth areas.

- Dividend Flexibility: Stronger capital buffers often provide the board with more confidence to return value to shareholders through buybacks or dividends.

- Regulatory Breathing Room: Following the complex integration of Credit Suisse, maintaining a robust capital position is essential for satisfying Swiss regulators.

| Period | Market RWA Value | Calculation Method |

|---|---|---|

| Q2 2024 | $22.5 Billion | Mixed (Internal Models/Standardised) |

| Q4 2025 | $23.8 Billion | Revised Standardised Approach |

What This Means for the Broader Market

The movement in UBS’s RWAs reflects a broader trend among Global Systemically Important Banks (G-SIBs). As the industry moves away from internal models toward the Basel III “Endgame” standards, the “model arbitrage”—where banks could tweak their own formulas to lower capital requirements—is disappearing.

The fact that UBS has managed to bring its charges down to a six-quarter low suggests that the bank has successfully pruned its most “expensive” risks—those that carry heavy weights under the new standardised rules. This likely involved shifting away from certain complex trading instruments that are penalized under the revised approach in favor of more capital-efficient assets.

However, the transition is not without its challenges. Moving to a standardised approach removes a degree of nuance. While internal models could account for specific hedges that reduced risk, the standardised approach is often a “blunter” instrument, sometimes requiring more capital for risks that a bank’s own data suggests are manageable.

Disclaimer: This article is provided for informational purposes only and does not constitute financial, investment, or legal advice.

The next major checkpoint for the bank’s risk trajectory will be the upcoming annual capital adequacy filing, which will provide a comprehensive view of how these market risk reductions have impacted the bank’s overall CET1 ratio and its long-term strategic capital plan.

What are your thoughts on the shift toward standardised banking regulations? Let us know in the comments or share this story with your network.