The insurance sector serves as a fundamental pillar of the global financial system, absorbing risk and providing a safety net for everything from residential property to complex corporate liabilities. However, the current macroeconomic climate has shifted the tide for many carriers. Fears of a prolonged economic slowdown, coupled with a deterioration in claims quality, have dampened investor sentiment across the board.

Recent data highlights a challenging period for the industry; over the last six months, the insurance sector has tumbled by 3.7%, a decline that outpaces the S&P 500’s 2.1% loss during the same window. For those looking to build a resilient portfolio, the cyclical nature of these stocks means that a perceived “bargain” can quickly become a “falling knife” if the underlying fundamentals are crumbling.

Navigating this volatility requires a disciplined approach to valuation and growth metrics. While some firms are weathering the storm, others are struggling with stagnant premium growth and eroding book values. Identifying the 3 insurance stocks we steer clear of involves looking past the surface-level dividends and examining the actual efficiency of capital allocation.

The primary concern for investors today is the “credit quality challenge”—the risk that the assets backing these policies are losing value or that the cost of claims is rising faster than the premiums being collected. When book value per share declines consistently, it often signals that the company is destroying shareholder value rather than creating it.

Stagnation and Credit Pressure: The Case of Lincoln Financial

Founded in 1905 in Fort Wayne, Indiana, the Lincoln National Corporation (NYSE: LNC) has long been a staple of the life and retirement space. Operating through four primary segments—Annuities, Life Insurance, Group Protection, and Retirement Plan Services—the company possesses a massive footprint. However, its current trajectory raises several red flags for analysts.

The most pressing issue is a lack of momentum. Net premiums earned have plateaued over the last five years, suggesting that the company is struggling to find incremental demand for its policies in a competitive market. This stagnation is compounded by a significant hit to the company’s internal value; book value per share has declined by 15.1% annually over the last five years, a clear indicator of credit quality challenges during this economic cycle.

a Return on Equity (ROE) of 11.1% suggests that management is struggling to identify investment opportunities that provide a sufficient premium over the cost of capital. Despite trading at a seemingly low valuation of 0.6x forward price-to-book (P/B) at a share price of $35.90, the erosion of the underlying book value makes this a risky entry point.

Growth Gaps and Value Erosion at Globe Life

Globe Life (NYSE: GL), which rebranded from Torchmark Corporation in 2019, operates as a holding company focusing on life and supplemental health insurance. While the company has a legacy dating back to 1900, its recent growth trajectory has failed to meet the benchmarks typically expected of high-performing financial institutions.

Over the last two years, annual revenue growth has hovered around 4.5%, a figure that lags behind the broader sector’s standards. More concerning is the lackluster growth in new insurance policies, which grew by only 4.8% annually—a pace that suggests a struggle to capture new market share.

This lack of growth is occurring while the company’s foundational value is slipping. Policy losses and capital returns have eaten into the balance sheet, leading to an annual decline in book value per share of 2.2% over the last five years. With a stock price of $143.53 and a valuation ratio of 1.7x forward P/B, Globe Life appears expensive relative to its growth profile and declining book value.

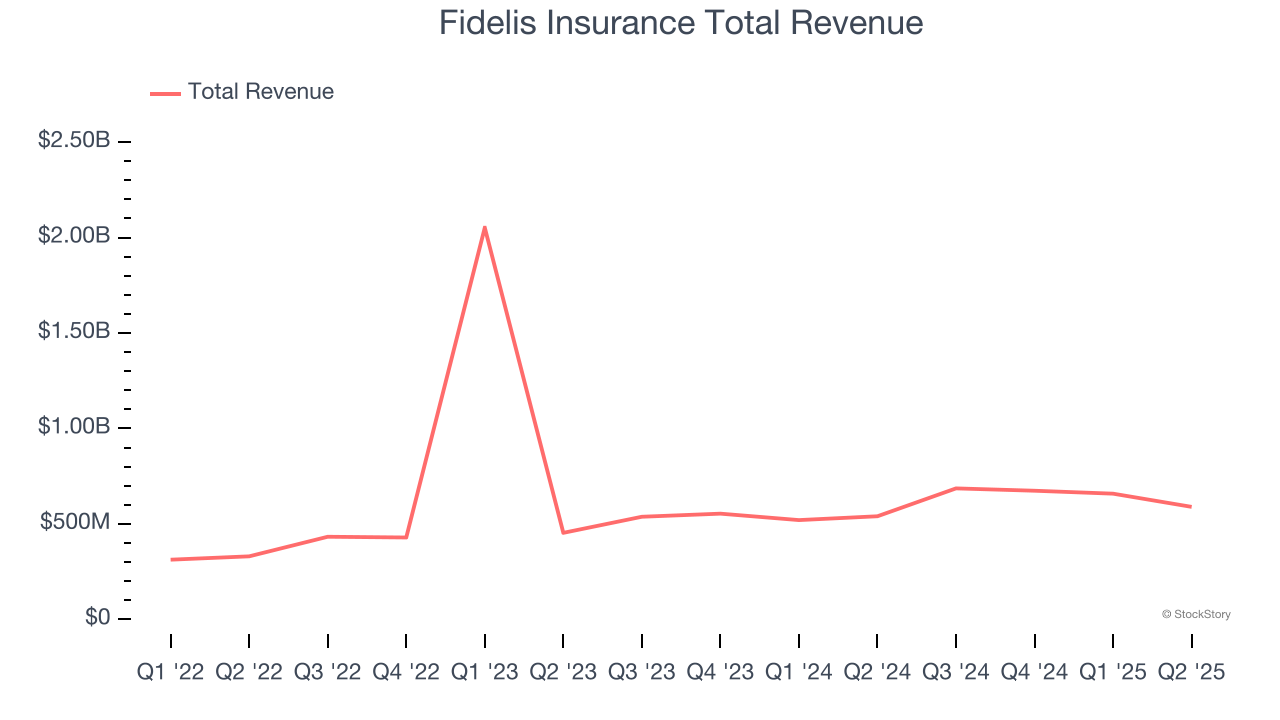

Efficiency Declines in Specialty Risk: Fidelis Insurance

Fidelis Insurance (NYSE: FIHL) represents a different kind of risk. Founded in Bermuda in 2014, it was designed to be a nimble player in the global specialty insurance and reinsurance markets. While specialty lines can offer higher margins, they are also more susceptible to volatility and sudden claims spikes.

The data for Fidelis reveals a troubling trend in operational efficiency. Over the last two years, the company’s pre-tax profit margin plummeted by 45.9 percentage points. This suggests that while the company is successfully growing its top line, that growth is not translating into profit. In fact, earnings per share fell by 4.7% annually even as revenue increased, indicating that the new business being written is significantly less profitable than previous cohorts.

While the company has seen an annual book value per share growth of 9.3% over the last two years, this remains below the rigorous standards set for the insurance sector. Trading at $19.22 per share, or 0.7x forward P/B, the stock may glance cheap, but the collapsing margins suggest a fundamental problem with the underwriting strategy.

Comparative Risk Metrics

| Company | Primary Concern | Book Value Trend (5yr) | Forward P/B |

|---|---|---|---|

| Lincoln Financial | Credit Quality/Stagnation | -15.1% Annually | 0.6x |

| Globe Life | Lackluster Policy Growth | -2.2% Annually | 1.7x |

| Fidelis Insurance | Profit Margin Collapse | +9.3% (2yr) | 0.7x |

For investors, the lesson here is that a low price-to-book ratio is not a safety net if the “book” itself is shrinking. In the insurance world, the balance sheet is the business. When that balance sheet is compromised by poor underwriting or bad investment calls, the stock price usually follows.

Disclaimer: This article is for informational purposes only and does not constitute financial advice. Investing in stocks involves risk. Please consult with a licensed financial advisor before making any investment decisions.

As the industry moves forward, the next critical checkpoint for these firms will be their upcoming quarterly earnings filings and the release of annual 10-K reports, which will provide a clearer picture of whether these book value trends are stabilizing or continuing to decline. Investors should closely monitor updates from the U.S. Securities and Exchange Commission (SEC) for official financial disclosures.

Do you agree with our assessment of these insurers, or do you see a value play here? Let us grasp in the comments and share this analysis with your network.