For prospective homeowners in France, the current landscape is a study in contradictions. While nominal property prices have seen a corrective dip, the cost of borrowing remains a significant hurdle. The central question for those eyeing an achat immobilier en 2026 is whether the decline in asking prices has been sufficient to offset the pressure of high, and potentially rising, interest rates.

To understand the current market, one must look past the “nominal” price—the number listed on a real estate portal—and examine “real” prices adjusted for inflation. When stripped of the inflationary noise, the French market reveals a surprising trend: in several regions, real estate values are at their lowest levels in two decades. Although, this mathematical advantage is often neutralized by the cost of credit, creating a divergent experience depending on where in the country a buyer is looking.

The current instability is characterized by a tug-of-war between falling asset prices and a restrictive lending environment. For some, particularly in the outskirts of the capital, the window of opportunity is wider than it has been since 2004. For others, specifically in Paris or rural provinces, the financial math remains stubbornly difficult.

The Inflation Illusion: Real vs. Nominal Pricing

A common mistake for buyers is relying on nominal price indices. For instance, looking at raw data from the National Institute of Statistics and Economic Studies (INSEE), one might see a steady climb in prices over the last twenty years. However, when these figures are converted into constant euros (adjusted for the Consumer Price Index), the narrative shifts.

In the provinces, the real price of apartments has not increased by the triple-digit percentages suggested by nominal data. Instead, the real increase has been closer to 50%, with the vast majority of that growth occurring between 2000 and 2007. By the end of 2025, the real price index for provincial apartments hit 150 (based on 100 in the year 2000), marking the lowest level since 2006.

The trend for provincial houses is remarkably similar. The real price index stood at 146 at the end of 2025. To find a real price level lower than this, buyers would have to look back to late 2004. This suggests that while the “sticker price” may feel high, the intrinsic value of the property relative to the cost of living has retreated significantly from the 2021 peak.

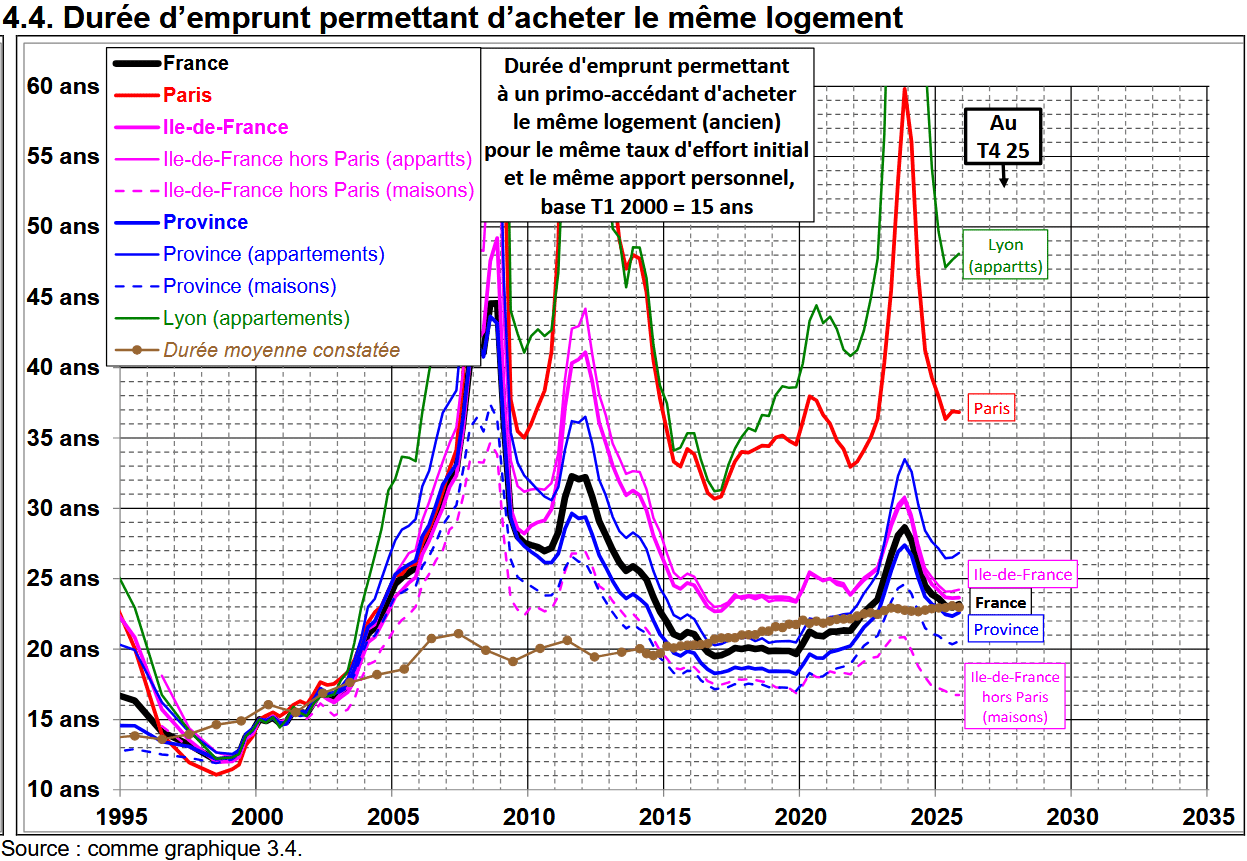

Regional Divergence: Why Location Dictates the ‘Right Time’

The “best time to buy” is no longer a national constant; it is now a regional variable. The most striking opportunity currently exists in Île-de-France, specifically outside the city limits of Paris. For those seeking a house in the Paris region, conditions are currently the most favorable observed in 22 years.

This is not merely a result of lower prices, but a combination of price corrections, disposable income evolution, and the specific duration of loans required to acquire a property. For apartments in the Île-de-France suburbs, the window is also highly favorable, mirroring the best conditions seen between 2015 and 2020.

Conversely, Paris remains a complex outlier. While real prices for Parisian apartments have dropped to an index of 245 (down from a 2021 peak of 285), bringing them back to 2016-2017 levels, the financing environment has deteriorated. During the 2016-2017 period, borrowing rates hovered between 1.00% and 1.50%. Today, rates exceed 3.25%, making the same property significantly more expensive to finance despite the similar real price.

| Region | Real Price Trend | Financing Context | Verdict |

|---|---|---|---|

| Île-de-France (Houses) | Significant correction | Favorable relative to income | Highly Opportunistic |

| Île-de-France (Apartments) | Moderate correction | Strong | Favorable |

| Paris (Apartments) | Return to 2016 levels | Restrictive (High Rates) | Difficult |

| Provinces (General) | Lowest real prices since 2006 | Mixed/Average | Neutral to Fair |

The Credit Constraint and the ‘Rental vs. Buy’ Calculation

The primary risk for 2026 is the trajectory of interest rates. There are indications that borrowing costs may increase in the near term. If property prices do not continue to adjust downward to compensate for these higher rates, the affordability gap will widen, potentially degrading current buying conditions.

Beyond the macro-economic trends, the decision to buy must be grounded in a personal timeline. Because of the high entry costs—including notary fees and taxes—buying a home is rarely more profitable than renting in the short term. The “break-even” point, where ownership becomes cheaper than a comparable rental, typically requires holding the property for several years.

This calculation varies by city and property type. In high-demand urban centers where rents are astronomical, the break-even point arrives sooner. In areas where the gap between property prices and rental yields is wider, the investment takes longer to pay off. Buyers are encouraged to run multiple scenarios, testing different price and rent evolution forecasts to avoid entering a “negative equity” trap.

Disclaimer: This article is intended for informational purposes only and does not constitute financial or investment advice. Real estate investments carry inherent risks, and individual results may vary based on local market conditions and personal financial standing.

As the market moves through 2026, the next critical checkpoint will be the updated quarterly data from the Banque de France regarding credit standards and the evolution of mortgage rates. These figures will determine if the current price corrections are sufficient to sustain a recovery in buyer demand or if further price drops are necessary to align with the new cost of capital.

Do you believe the current price drops justify the high interest rates? Share your thoughts in the comments or share this analysis with others planning their 2026 real estate projects.

Related reading