Managing a household budget is rarely about a single windfall or a one-time investment. it is an exercise in endurance and foresight. For many families, the challenge lies in balancing immediate needs—such as upgrading to a larger home—with long-term imperatives like university tuition for children and a sustainable retirement fund. The goal is to move beyond simple saving and toward a structured strategy that allows a “tesoretto,” or nest egg, to grow without compromising current quality of life.

Effective financial planning requires a comprehensive map of a family’s entire life cycle. This means identifying specific milestones, from risk coverage and supplementary pensions to the eventual purchase of a second home. The process is not static; it requires a realistic assessment of current and future income streams versus expenditures, ensuring that the chosen investment vehicles are efficient and aligned with the timeline of the goals.

Because life is unpredictable, these plans must be treated as living documents. Financial experts suggest that a strategy requires regular “tune-ups” or revisions whenever significant life changes occur—such as a change in employment, the birth of a child, or a shift in market conditions—to ensure the original hypotheses still hold true.

To illustrate how these principles apply in the real world, Progetica has analyzed three distinct demographic scenarios. These models demonstrate how different life stages and family structures dictate where capital should be allocated to maximize growth and security.

Tailoring Investment Strategies to Life Stages

The approach to investing changes fundamentally depending on whether an individual is building a foundation, managing a growing family, or preparing for a transition into retirement. The primary driver is the “time horizon”—the length of time an investor can exit their money untouched before needing it.

For a 35-year-old single professional, the focus is often on aggressive growth and flexibility. With a longer window before retirement, this profile can typically afford higher volatility in exchange for higher potential returns. The priority here is often the first major asset purchase, such as a primary residence, while simultaneously starting a diversified portfolio that benefits from compound interest over several decades.

In contrast, a family unit—such as two 40-year-old parents with two young children—must pivot toward a multi-layered strategy. Their financial planning must account for “competing priorities”: the need for a larger home to accommodate growing children, the accumulation of funds for university education, and the necessity of robust insurance and risk coverage to protect the dependents. For these households, liquidity and stability turn into as important as growth.

Finally, for a couple in their mid-50s without heirs, the strategy shifts toward wealth preservation and income generation. With retirement approaching, the objective is to ensure that the accumulated capital provides a comfortable lifestyle without the risk of significant depletion. The focus moves from “growing the pot” to “managing the draw-down,” often utilizing supplementary pension schemes to bridge the gap left by state pensions.

Comparison of Financial Priorities by Profile

| Profile | Primary Goal | Risk Tolerance | Key Investment Focus |

|---|---|---|---|

| Single (35) | Asset Accumulation | High | Equity Markets & First Home |

| Parents (40s) | Family Security | Moderate | Education Funds & Real Estate |

| Couple (55+) | Income Sustainability | Low/Moderate | Pensions & Capital Preservation |

The Mechanics of Growing a Nest Egg

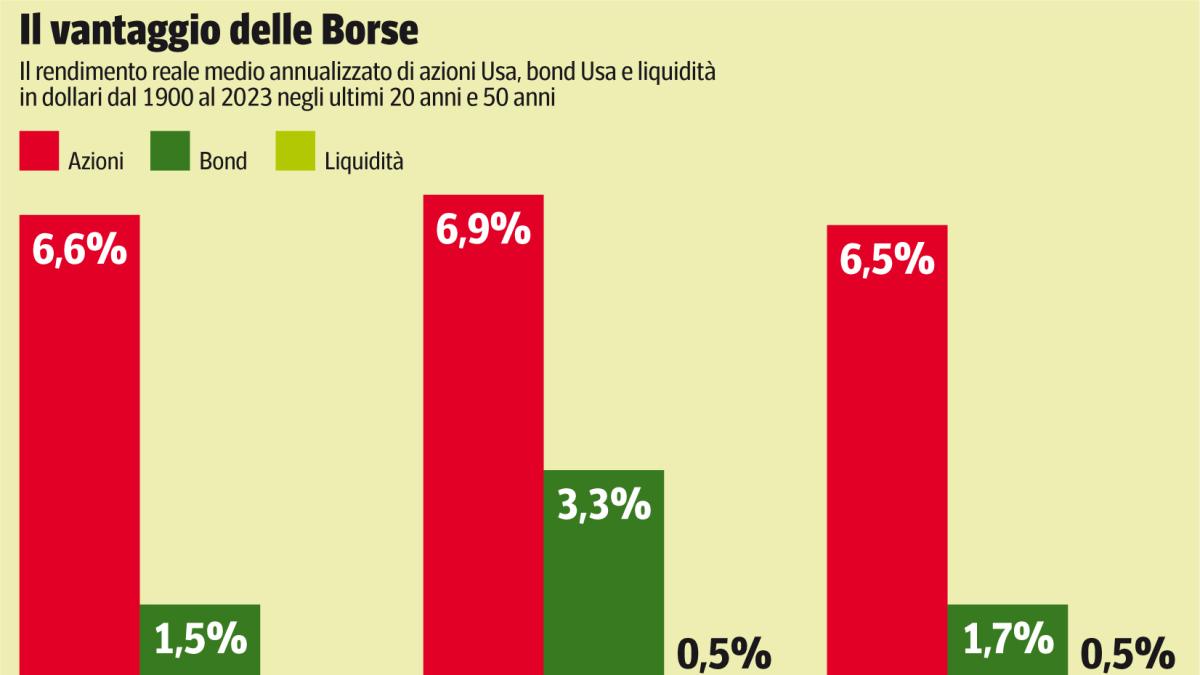

To make a “tesoretto” grow, investors must move beyond traditional savings accounts, which often fail to retain pace with inflation. Diversification is the primary tool for mitigating risk. By spreading investments across different asset classes—such as stocks, bonds, and real estate—investors can protect themselves against a downturn in any single sector.

For those planning for their children’s education, dedicated savings plans or targeted investment accounts can be effective. These allow parents to set aside a monthly sum that grows over 10 to 15 years, reducing the need for high-interest loans when the students reach university age. According to guidelines from the principles of asset allocation, the mix of these investments should shift toward more conservative options as the date the money is needed approaches.

Retirement planning, or “previdenza integrativa,” is equally critical. Relying solely on state pensions can be risky given changing demographics and legislative shifts. Private pension funds or individual retirement accounts provide a tax-advantaged way to ensure that the standard of living is maintained after the final paycheck. In Italy, for instance, the Commissione di Vigilanza sui Fondi Pensione (COVIP) provides oversight and data on how supplementary pensions function to protect savers.

Risk Management and the ‘Financial Tune-Up’

No financial plan is complete without a strategy for risk. This involves “covering the gaps”—ensuring that a sudden illness, disability, or loss of income does not wipe out years of savings. Life and disability insurance are not just expenses; they are hedges that protect the investment plan from being derailed by catastrophe.

the concept of the “financial tune-up” is essential. A plan created at age 30 is rarely applicable at age 40. Changes in the economic landscape, such as fluctuating interest rates or inflation, can erode the purchasing power of a fixed savings goal. Regular reviews allow families to adjust their contribution levels or pivot their investment choices to stay on track toward their goals, whether that is a larger house or a more lavish retirement.

The ultimate success of a financial plan is measured not by the total amount of money saved, but by the alignment of those resources with the family’s actual needs. When the “tesoretto” is grown with intention, it ceases to be a mere sum of money and becomes a tool for stability and freedom.

Disclaimer: This article is provided for informational purposes only and does not constitute professional financial, investment, or legal advice. Readers should consult with a certified financial planner or qualified advisor before making significant investment decisions.

As economic conditions evolve, the next critical checkpoint for many investors will be the upcoming quarterly inflation reports and central bank interest rate decisions, which will dictate the real return on savings and the cost of mortgages for those seeking a larger home. We invite readers to share their experiences with financial planning and their strategies for balancing family needs in the comments below.