The aviation industry is facing a volatile new era of operational costs, with Virgin Atlantic leadership warning that higher jet fuel prices are ‘here to stay.’ This shift suggests that the period of relatively cheap energy, which historically allowed airlines to maintain aggressive pricing and rapid expansion, has been replaced by a structural increase in overhead that will likely ripple through ticket prices and route availability.

The warning comes as carriers grapple with a “perfect storm” of geopolitical instability and supply chain fragility. While fuel price fluctuations are a standard part of the aviation business model, the current trajectory is being driven by more than just market volatility; This proves being exacerbated by systemic threats to global oil transit corridors and an accelerating transition toward more expensive sustainable aviation fuels (SAF).

For passengers, this means the era of the “budget” long-haul flight may be under permanent pressure. When fuel costs rise structurally, airlines typically have two choices: absorb the cost and risk insolvency, or pass the expense to the consumer through fuel surcharges and higher base fares. Given the thin margins of the industry, the latter is the more probable outcome.

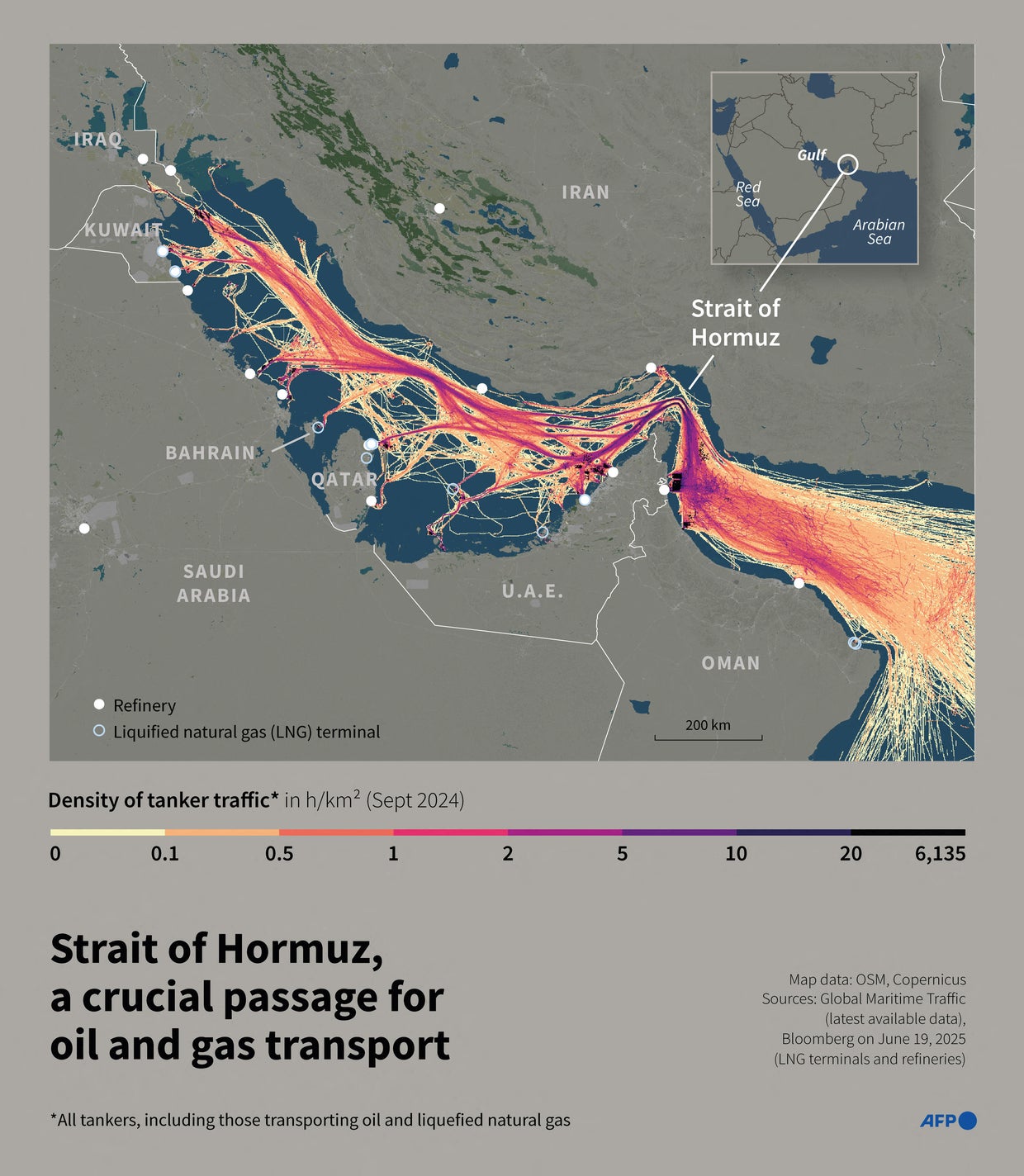

The Geopolitical Choke Point: The Strait of Hormuz

A primary driver of the current fuel anxiety is the precarious state of global oil transit. Industry bodies, including Airports Council International, have issued warnings regarding the potential for severe fuel shortages if the Strait of Hormuz remains closed or becomes impassable. As one of the world’s most critical maritime chokepoints, any prolonged disruption in this region threatens the flow of crude oil and refined products to global markets.

The EU airline industry has echoed these concerns, noting that a closure of the Strait would not only spike prices but could lead to physical fuel shortages. This scenario moves the conversation from a matter of “cost” to a matter of “capacity,” where airlines might be forced to prioritize certain routes or implement fuel rationing to maintain essential operations.

The impact of such a disruption is magnified by the current state of global refining capacity. Because jet fuel is a specific grade of refined product, a shortage of crude oil—or a disruption in the refineries that process it—creates a bottleneck that cannot be solved by simply buying oil from another region. The logistics of moving massive quantities of aviation kerosene are rigid, leaving carriers vulnerable to localized geopolitical shocks.

Structural Shifts and the Cost of Sustainability

Beyond the immediate threat of conflict, there is a long-term financial shift occurring in how planes are powered. The aviation sector is under intense pressure to decarbonize, which involves a transition from traditional kerosene to Sustainable Aviation Fuels (SAF). While environmentally necessary, SAF is significantly more expensive to produce and procure than fossil-based fuels.

This transition creates a “floor” under fuel prices. Even if geopolitical tensions in the Middle East were to resolve, the mandate to integrate greener fuels means that the cost per gallon is unlikely to return to pre-pandemic or historical lows. The “here to stay” nature of these prices refers not just to the price of crude, but to the cost of the energy transition itself.

Airlines are now managing a complex balancing act: they must invest in newer, more fuel-efficient aircraft while simultaneously paying a premium for the fuels they use today. This capital expenditure, combined with higher operational costs, creates a challenging environment for carriers that are still recovering their balance sheets from the COVID-19 era.

Who is affected and how?

The burden of these rising costs is distributed across several stakeholders in the aviation ecosystem:

- The Passengers: Likely to see an increase in “fuel surcharges” and a general rise in ticket prices, particularly on long-haul routes where fuel represents the largest single operating expense.

- The Carriers: Facing squeezed profit margins and a require for more aggressive hedging strategies to protect against sudden price spikes.

- Airport Operators: Dealing with the logistical strain of managing fuel reserves and the potential for flight cancellations if shortages occur.

- Global Trade: As air freight costs rise in tandem with passenger fares, the cost of transporting high-value, time-sensitive goods will likely increase.

The Risk of Fuel Rationing

In an extreme scenario, the industry may face fuel rationing. While this sounds like a relic of wartime economics, the prospect is being discussed by analysts as a contingency for severe supply disruptions. If rationing were to occur, airlines would likely prioritize their most profitable “trunk” routes—such as London to New York—while cutting service to thinner, less profitable regional destinations.

This would create a two-tier aviation system where connectivity for smaller cities is sacrificed to keep the primary hubs operational. For the “big three” airlines and other global carriers, this would mean a strategic retreat from secondary markets, further consolidating the power of the largest hubs and increasing the cost of travel for those in underserved regions.

| Risk Factor | Immediate Impact | Long-term Outlook |

|---|---|---|

| Strait of Hormuz Closure | Supply shortages & price spikes | Increased route volatility |

| SAF Integration | Higher per-gallon cost | Structural price floor |

| Geopolitical Tension | Increased insurance/fuel costs | Shift in global flight paths |

| Refining Bottlenecks | Local fuel scarcity | Need for diversified sourcing |

What Happens Next

The industry is now watching the diplomatic efforts between the U.S. And Iran with extreme scrutiny. The reopening or stabilization of the Strait of Hormuz remains the most immediate variable that could provide short-term relief to fuel prices. However, the broader trend toward more expensive, sustainable energy remains a constant.

The next critical checkpoints for the industry will be the quarterly financial filings of major carriers, which will reveal how much of these costs are being absorbed versus passed on to consumers. Updated mandates on SAF blending percentages from regulators in the EU and US will provide a clearer timeline for when the “green premium” will become a permanent fixture of every ticket price.

Disclaimer: This article is for informational purposes only and does not constitute financial or investment advice.

We want to hear from you. Do you expect your travel costs to rise this year, or have you already seen the impact on your bookings? Share your thoughts in the comments below.