For many homeowners, the monthly mortgage payment is viewed as a static obligation—a fixed cost of living that remains unchanged until the loan is paid in full. However, a shift in the financial landscape suggests that a surprisingly small adjustment in interest rates can lead to a substantial increase in long-term savings. In the Spanish housing market, reducing a mortgage interest rate by just half a percentage point can potentially save a borrower as much as €18,000 over the life of the loan.

This financial leverage is not limited to those seeking new loans. Homeowners who already hold a mortgage can often realize these gains by renegotiating their current terms or switching lenders to capture more favorable market conditions. The cumulative effect of a 0.5% reduction is significant because mortgage interest compounds over decades, meaning that a seemingly negligible dip in the rate prevents thousands of euros from being lost to interest payments.

Navigating this process manually often proves daunting for the average consumer. The complexity of comparing various banking offers, understanding the fine print of “linked” products, and negotiating with established lenders can create a barrier to entry. This has led to the rise of fintech solutions designed to democratize access to better mortgage conditions through automated comparison and expert advisory services.

One such platform, Openteca, has positioned itself as a free resource for borrowers to optimize their home financing. By acting as an intermediary that compares multiple banking options, the platform aims to align borrowers with conditions tailored to their specific financial profiles, removing the guesswork from the search for a lower interest rate.

The Mathematics of Interest Rate Reduction

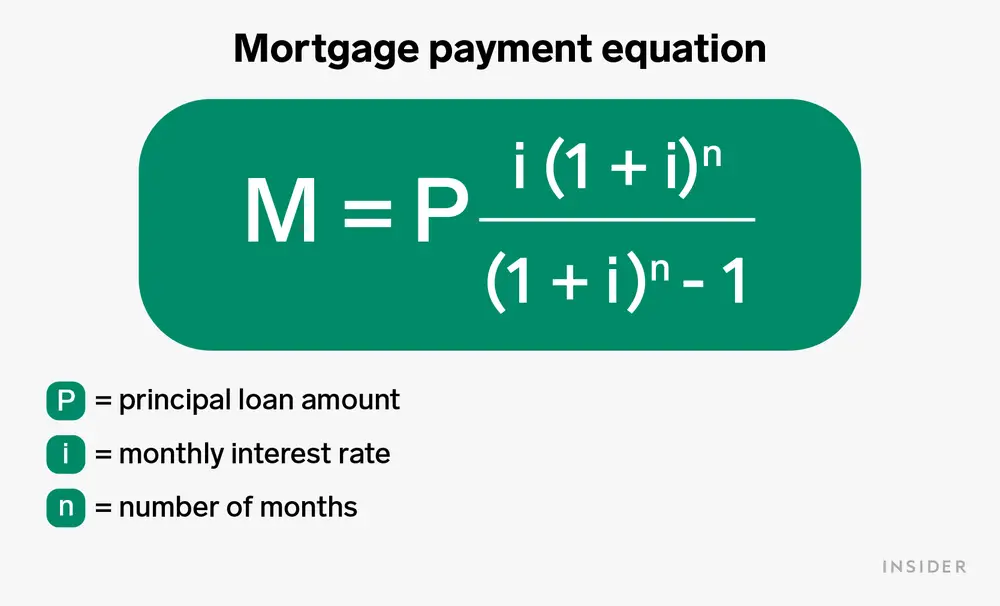

To understand why a half-point drop is so impactful, one must look at the total cost of credit. A mortgage is not merely a loan for the principal amount of a home; This proves a long-term contract where the interest rate dictates the actual price of the property over time. When a borrower secures a rate that is 0.5% lower, they are effectively reducing the cost of the capital they are borrowing every single month for 20 or 30 years.

For a standard mortgage, this reduction lowers the monthly installment, which in turn increases the borrower’s monthly disposable income. More importantly, it reduces the total amount of interest paid to the bank. When calculated across the full term of a loan, these monthly increments aggregate into a sum that can reach the €18,000 mark, depending on the principal balance and the remaining duration of the loan.

The ability to achieve these savings often depends on the borrower’s ability to present a competitive profile to multiple banks. Lenders are more likely to offer lower rates to “low-risk” clients—those with stable income and a healthy equity position. Using a comparison tool allows a borrower to identify which banks are currently aggressive in their pricing for specific profiles, creating a competitive environment that favors the consumer.

Streamlining the Mortgage Comparison Process

The traditional method of shopping for a mortgage involves visiting multiple bank branches, submitting the same documentation repeatedly, and waiting days for a non-binding offer. This fragmented approach often leads to “decision fatigue,” where borrowers settle for a sub-optimal rate simply to complete the process.

Modern advisory platforms like Openteca aim to condense this timeline. The digital transition allows for a more efficient sequence of events, moving from initial registration to a finalized comparison in a fraction of the time previously required.

| Stage | Action | Estimated Timeframe |

|---|---|---|

| Registration | User provides basic financial data and loan requirements | Under 5 Minutes |

| Analysis | Platform compares profile against current bank offers | 12 to 24 Hours |

| Review | User receives a curated list of the best available conditions | Immediate upon delivery |

| Execution | Negotiation and signing of the new mortgage terms | Variable by bank |

By consolidating the search process, borrowers can see a side-by-side comparison of interest rates, commissions, and required linked products (such as insurance or payroll deposits). This transparency is critical, as a lower nominal interest rate can sometimes be offset by expensive mandatory products, making a comprehensive comparison essential for true savings.

Who Benefits Most from Mortgage Renegotiation?

While any borrower can benefit from a lower rate, certain stakeholders are particularly well-positioned to take advantage of these tools in the current economic climate. Those who took out mortgages during periods of peak interest rates may find that the market has shifted in their favor, making a refinance or a subrogation (switching the loan to another bank) highly lucrative.

first-time buyers often lack the leverage to negotiate with large banks. By using a comparison platform, they can enter the market with a clear understanding of the “floor” price for interest rates, allowing them to push back against inflated offers. The goal is to ensure that the mortgage is adapted 100% to the individual’s needs rather than fitting the borrower into a rigid bank product.

The impact extends beyond simple monthly savings. Reducing the cost of a mortgage improves a household’s overall financial health, providing a buffer against inflation and increasing the ability to save for other long-term goals or to pay down the principal faster, further reducing the total interest paid.

For those interested in exploring these options, the process typically begins with a digital registration on the Openteca website, followed by a brief data entry phase to determine eligibility and the best possible market matches.

Disclaimer: This article is provided for informational purposes only and does not constitute professional financial advice. Mortgage conditions vary based on individual creditworthiness, loan-to-value ratios, and specific banking policies. Readers should consult with a certified financial advisor before making significant changes to their loan agreements.

As the European Central Bank continues to adjust monetary policy, the cost of borrowing will likely remain fluid throughout 2025. Homeowners should monitor the European Central Bank’s official announcements regarding interest rate trends to determine the optimal moment to renegotiate their terms.

We invite our readers to share their experiences with mortgage renegotiation in the comments below. Have you successfully lowered your interest rate recently?