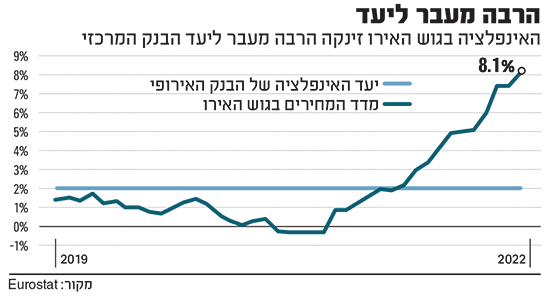

For many months the European Bank hesitated Central to act decisively against the dramatic price increases on the continent. He was the most “June” against the British “Bank of England” and the American “Federal Reserve”. The bank’s president, Christine Lagard, reiterated his experts’ assessments that inflation will start to fall soon and that the situation in Europe is “not similar” to what is happening overseas or to the Lagard Canal also warned of repeating the steps that led to the bloc a decade ago. But with historical inflation rates only rising – 8.1% in the island blocThe whole of May, and 8.7% in its large economy, Germany – the bank was forced to announce a change of direction over the weekend.

The European announcement was a bit “lost” in the shadow of the drama unfolding in the American markets, but in fact, the European Central Bank (ECB) surprised the markets and announced a sharper plan than the experts expected. The central bank, which is responsible for monetary policy in the 19 eurozone countries, has announced that for the first time in a decade it intends to raise interest rates by 0.25% in July, and that a “larger increase” is likely to occur in September if inflation continues.

After eight years of negative interest rates, Europe will return to positive interest rates territory in the autumn. In addition, the Bank will complete earlier than expected its huge quantitative easing program – a massive acquisition of government and banking bonds of the eurozone countries.

A short blanket and a thin rope

Questions about the speed with which interest rate hikes will take place, their effectiveness in lowering inflation and the effects on growth in the eurozone are still open. The Board of Governors of the European Central Bank is in fact divided between northern European countries such as Germany and the Netherlands, and southern countries such as Italy and Spain. The jump in interest rates puts the latter group – all eurozone countries in deep debt – at much greater expense on repayments, not only directly but also because of the excess risk that they will reach insolvency. The debt costs of these countries have skyrocketed since the announcement.

The monetary blanket of the European Central Bank is shorter than that of other central banks because it has to take into account the cross-cutting interests of 19 different economies. What was announced in Amsterdam on Thursday by the Council of Governors of the ECB is a compromise between the two camps.

In fact, the thin rope that the European Central Bank now has to walk is the first of its kind, because current inflation is the highest since the adoption of the single currency in 1999, and in many countries it also breaks four-decade highs. Plus, it’s hard to see how things will get better. In terms of energy, the price of a barrel of crude oil has repeatedly exceeded the $ 120 threshold in recent days. The price of natural gas is skyrocketing.

The question that hovers over the markets

European governments are already subsidizing energy in billions, but this component is still boosting inflation, and it in turn is also affecting the food sector, the second most important factor in the price jump. In Germany, an alarming review was published last week, according to which food producers have not yet rolled the full price increase on consumers, and they are expected to rise even more.

The fact that the markets reacted sharply to the ECB’s announcement is evidence of the level of uncertainty, although some rate hike in July was expected. The euro lost another 1% against the dollar after the announcement, completing a 13% decline against the US currency over the past year. The pan-European stock index Stoxx 600 fell 1.3% after the announcement.

European commentators, and even governors of central banks, have expressed differing views on the effectiveness of the measures. “My impression is that everyone has lost,” one of them told FT anonymously, explaining that the fall in the euro would increase imports, which would further increase inflation, and that the debt costs of southern European countries had already skyrocketed. “This is not what you want to happen in the market,” he said.

Interim: Expect an alternative bond purchase program

The second historic move announced by the central bank, which is the completion of the huge bond purchase program it launched in mid-2014, also contributes to the markets’ hopes of launching an alternative plan, or a partial plan that will help lower southern European debt, but it is unclear In practice, the European Central Bank is set to complete a program in which trillions have been invested in government and corporate bonds in the eurozone. “He, too, will have to start and drastically reduce his balance sheet. Like the Fed, it is not known what impact this will have on the markets and how he will do so.

In an interview with Dutch television last month, the presenter confronted Legard with a picture of the ECB’s balance sheet. “I do not regret the step we took in March 2020, four months into my tenure,” replied Lagard, recalling the corona plague, “that’s all we had, otherwise the economy would have collapsed.” But how do you reduce the mListen now, the interviewer wondered. “It’s going to happen,” Lagard said, silent in front of the audience’s embarrassed laughter; “how?” Tap the facilitator lightly, “At the right time, it will happen,” she replied. “Do you sleep at night when you see it?” Added. “Of course I have to sleep every night, and worry every morning,” she said sharply.

Possible question of the credibility of the ECB is perhaps the most dangerous thing at the moment. Only last December did the central bank announce in its publications that it is estimated that the bond purchase program will continue throughout 2022. Lagard herself said it is “extremely unlikely” that the bank will raise interest rates before 2023 “at the earliest”. The bank and its president are forced to repeat them, change policies, and the question of their ability to fight inflation without dragging a sharp recession or threatening the integrity of the eurozone, hovers over the markets.