The authors are the CEO of the financial consulting firm Complex and an analyst at the company. The parties in the article may invest in securities and / or instruments, including those mentioned in it.

US inflation accelerated to 9.1% in June, a sharp rise from 8.6% in May and the fastest pace since November 1981. This has led to fears that the Fed will make a historic move and raise interest rates by 1% this month.

However, the University of Michigan’s consumer sentiment survey released Friday, which is considered the leading barometer of the U.S. citizen’s situation, revealed encouraging news. Consumers expect inflation to fall to 2.8% in five years, down sharply from 3.1% last month. Inflation expectations for the year also fell to 5.2%. Therefore, the market re-estimated that the Fed would raise the interest rate by “only” 0.75%.

However, in order to analyze in depth the inflation outlook against the contradictory data, and accordingly – the rate of interest rate increases, one must dive in depth into the main factors influencing it. These find that the Fed’s overarching task of curbing inflation without causing a recession is becoming particularly complex.

The power in the workers

The Fed’s main focus on fighting inflation is the boiling labor market in the US. The US economy created 372,000 jobs in June, well above 250,000 job forecasts, and the unemployment index remained at a historic low of 3.6%. According to the US Bureau of Statistics, There were 11.3 million job vacancies, double the number of workers interested in working.

On the other hand, wages in the United States do not keep pace with inflation. In the past year, the average wage has increased by 5.1%, so that wages adjusted for inflation and working hours have fallen by 4.4%, the fastest rate in four decades.

The Fed fears that the combination of high demand for workers and the erosion of real wages will lead to a destructive spiral of wage increases leading to price increases, further pressures to wage increases and so on. The concern is heightened by the power given to workers to demand wage increases in a tight labor market, where it is difficult to hire new skilled workers.

Evidently, employers in one-third of U.S. counties have given workers bonuses, or are considering doing so, to offset high inflation.

Another inflationary risk stems from the fact that despite the erosion of real wages, American consumers have savings of about 10% of the annual GDP in the United States, which leaves them financially strong, and preserves strong consumption.

Half the glass is empty

On the other hand, “less quoted” indices of the labor market present a much more complex and problematic picture. The low unemployment rate only takes into account people who are actively looking for work. However, the number of participants in the labor force (employed and unemployed interested in working) fell to 62.2% in June, a low rate in historical terms.

Had the labor force participation rate been as high as before the corona outbreak in 2020, the unemployment rate today would have stood at 5.5%.

The gap is due to the fact that there are about 11.5 million Americans who did not return to the labor market after the corona crisis, according to the U.S. Census Bureau, and are not included in the calculation. Additional due to fear of infection.

In addition, an additional 2.9 million were laid off or expelled, and a further 2.1 million ceased to work due to the closure of businesses following the corona.

Had some of those people tried to return to work, the shortage of workers would have eased and eased the pressures for wage increases designed to retain workers. However, lack of employment for a long time exacerbates the problem, as it makes it difficult to return to the workforce due to skills erosion, and creates structural unemployment.

The resulting conclusion is that the U.S. labor market is not as boiling as reflected in unemployment data. Worse, the low labor force participation rate, along with the acute need for workers, creates an economy that cannot grow without producing high inflation. Extensive, which will intensify the unemployment rate and the low participation in the labor market, and which may lead to a sharp recession, while maintaining the current situation will involve exacerbating inflation.

Rents will rise and with it inflation

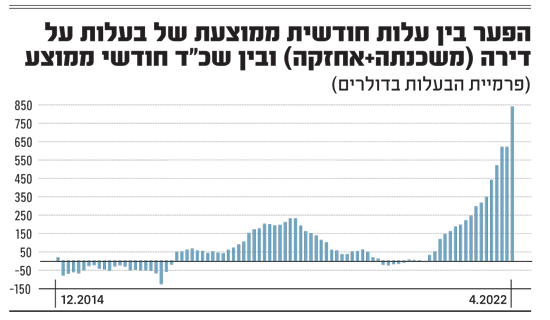

In analyzing the components of the consumer price index, the most significant source of inflationary pressures in the US is the residential real estate market, and in particular the cost of renting homes, which accounts for more than 30% of the index, far beyond any other component. Therefore, the behavior of the residential rental market is much more important than the prices of energy and goods in the headlines, although they are not part of the core index (on which the Fed focuses), due to the high volatility in them.

Rental prices rose 0.8% in June, following a previous 0.6% rise in May. In annual terms, the average rent in the US has risen by 5.8%. In our opinion, this is only the beginning of the rise in rental prices.

This is because residential real estate prices in the US have risen by more than 20% on average in the past year, along with a 30-year rise in mortgage interest rates to 5.8% (double its level in early 2022). As a result, the cost of a mortgage on an average American household has risen to 31.5 percent of the average income, above the 28% limit accepted by U.S. banks. This will prevent many from taking out a mortgage, and for others it will make it unprofitable.

The combination of the increase in the cost of buying a home (due to the jump in prices and mortgage interest rates) and the rising maintenance costs due to inflation, creates an “ownership premium” on an unprecedented scale, relative to rent. As a result, many housing demands are being pushed from the ownership market to the rental market.

In order to return the cost of rent to equilibrium with the cost of ownership, rental prices need to rise significantly.

In our opinion, a counter-scenario, of a sharp decline in real estate prices in order to reduce the gaps, is less likely. This is due to a chronic shortage of millions of housing units in the US, and the lack of financing conditions for a crisis. This situation is caused by the conservative and healthy mortgage market in the US and the high equity that Americans have in homes after rising prices. This capital encourages them to pay, in stark contrast to the conditions created in the subprime crisis.

In conclusion, the combination of data from the labor market and real estate shows that there is significant pressure to continue rising inflation, and that the toolbox that allows the Fed to fight it without causing a recession is narrower than it first appears.

We estimate that the interest rate will rise by 0.75% this month, but the Fed will continue to raise interest rates sharply in the face of continued high inflation later this year, reaching an interest rate of about 4% at the end of the year.