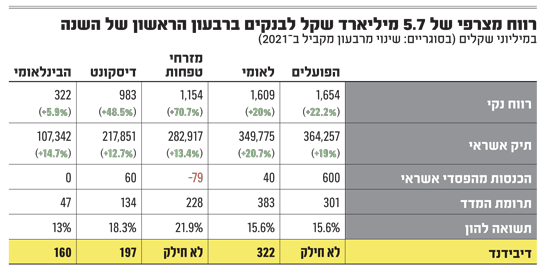

Galloping inflation? Consumption slowdown? War in Ukraine? All of this did not prevent the five largest banks in Israel from recording an aggregate profit of NIS 5.7 billion in the first quarter of the year. This is led by Hapoalim and Leumi, who each recorded a net profit of more than NIS 1.6 billion, while Mizrahi Tefahot and Discount show record profits on their part.

During the quarter, all banks enjoyed credit growth in its various industries, especially the mortgage sector, due to the provision of mortgages inScope Which is estimated at more than NIS 34 billion in the first three months of the year.

Thus, the mortgage portfolio of the five banks has skyrocketed by almost NIS 20 billion since the beginning of 2022, to a total of NIS 498.3 billion. Mizrahi Tefahot is still the bank with the largest market share in the field, 36.4%, but other banks are challenging it more than before, especially Discount, which managed to increase its market share significantly, thanks to 28% growth in the mortgage portfolio.

Leumi – the fastest growing credit in the quarter

However, as mentioned, growth is not just about housing credit. While at the end of the first quarter last year the total credit provided by the banks to the public was NIS 1.15 trillion, within a year it increased by NIS 172 billion, and at the end of the quarter amounted to NIS 1.32 trillion.

Hapoalim still has the largest credit portfolio in Israel, amounting to more than NIS 364 billion, but in the first quarter of this year the fastest growing bank in this respect is Leumi, managed by Hanan Friedman, which increased its credit by 7.6% to NIS 350 billion. It is followed by the growth rate in the reported quarter by international extras (an increase of 5%), Mizrahi Tefahot (4.2%), Hapoalim (3.3%) and Discount (2.2%).

Drama in credit for construction and real estate

While the growth in mortgage portfolios crosses the entire banking system as one line, the real drama took place on the other side of the real estate sector – that of financing for construction. Entrepreneurs financed projects, which often exceeded 100%, ie provided loans in excess of the cost of the project, but Hapoalim and Leumi came very close to the ceiling announced by the Supervisor of Banks – according to which the construction credit rate will not exceed 26% of total credit. Will exceed 22%.

To this end, the two banks have taken a series of actions, from purchasing insurance for part of the portfolio, which provided them with capital to continue providing credit, through promoting syndication transactions (bringing in partners to bear part of the loan) to stopping dividends, as Bank Hapoalim did when publishing the last quarter .

Indeed, Hapoalim managed to reduce its exposure to credit risk to the construction and real estate industries in Israel from NIS 131 billion at the end of last year to NIS 130.4 billion at the end of the quarter.

During the quarter, Leumi, on the other hand, increased its credit portfolio for construction by NIS 7.5 billion, a jump of 9.3% to a volume of NIS 88.3 billion, and accordingly its credit risk in this industry increased by about 10% to NIS 131.8 billion. The vast majority of credit was granted to infrastructure or residential projects and without mall financing, with close supervision, and the bank refrained from entering into projects without strong collateral.

Despite this growth, Leumi has also had to cool down a bit on the credit it gives to entrepreneurs and become more picky. Although this is not a strong pressure on the brake pedal, as the workers in the field did, it is enough to allow the next two banks – Mizrahi Tefahot and Discount – to increase their footprint in the field.

At Discount, the exposure to the real estate industry was 17.33% at the end of the quarter, compared with 17.12% at the end of 2021, after increasing the exposure by NIS 600 million, while in Mizrahi Tefahot the figure fell from 14.7% to 14.4% in the first quarter, despite an increase of 1.5 billion Shekel during the period.

Between the dividend and equity

In order to deal with the high leverage, last March the Bank of Israel submitted to the banks a draft directive according to which in cases of granting credit intended for the purchase of land for development or construction purposes at a rate exceeding 75% of the value of the property purchasedThey will be required to increase the restricted capital to 150%.

This draft has made banks much more cautious about the equity for which they can continue to grow in the credit sector. This is mainly in light of the damage most of them suffered from the rise in interest rates, which in turn led to an increase in government bond yields.

For Hapoalim and Discount, the increase in bond yields resulted in an injury of NIS 800 million each, for Mizrahi Tefahot an injury of NIS 320 million, for International about NIS 50 million and the only one that managed to get out of it with a slight profit was Leumi. This is because these vulnerabilities are partially offset by the Bank’s liabilities to its employees’ pensions, and Leumi’s portfolio is larger than the rest, and even larger than its bond holdings.

It should be noted that Discount foresaw this damage ahead of time, and therefore launched a share issue, in which it raised about NIS 1.4 billion, which will allow the bank to continue providing credit.

The damage due to rising bond yields, along with the Bank of Israel’s draft – which currently contains a clause according to which the additional capital allocation also applies to past transactions with real estate entrepreneurs, plus the uncertainty in the capital market, was immediately translated into the dividend clause in the banks’ reports.

As predicted by estimates first published this week in Globes, Mizrahi Bank has announced that it is halting the dividend distribution for the first quarter profits. Mizrahi joined Hapoalim, which announced this on Monday, and continued the policy it adopted from the fourth quarter of 2021.

Leumi also decided to distribute a reduced dividend, at a level of only 20% of the quarter’s profits, compared to a declared policy of 40%. In contrast, International, which has the highest capital adequacy ratio in the system and the most generous dividend distribution policy (50% of profit), and Discount, which adhered to a 20% distribution, complied with their existing policy and distributed NIS 160 million (the largest international ever) and 197 NIS 1 million, respectively.