Investors are betting on a quiet August for markets, with currency markets suggesting a lull in volatility after this week’s key events.

The FX options market signals a calm August ahead, prompting a closer look at the popular carry trade strategy amid potentially subdued market volatility.

- FX options markets point to lower volatility after this week’s events.

- Carry trade strategies, especially those funded by the dollar, have shown strong year-to-date performance.

- Emerging markets in Central and Eastern Europe, and parts of Latin America and the Middle East, appear most attractive for carry trades.

- Asia’s underperformance and geopolitical risks make it less compelling for carry traders in August.

Markets are theoretically lining up for a tranquil August, at least according to the foreign exchange options market. After this week’s scheduled event risks, the traded volatility curve shows expected volatility dropping significantly. For instance, one-month EUR/USD is trading at a full vol lower than one-week implied volatility.

The immediate calendar includes Friday’s jobs report and U.S. tariff deadlines on August 1. The prevailing market sentiment is that even if tariffs revert to higher levels for some countries, these increases are likely temporary. The market largely views tariffs as transactional rather than ideological, with a baseline 15% duty achievable if trading partners make substantial commitments to invest in the U.S.

While some argue this market complacency about tariffs is unwarranted, the critical question for August is what could potentially disrupt the calm. Many central bankers, politicians, and investors are on holiday. If major trade agreements, like the U.S.-China trade truce, are extended by another 90 days, the market’s default setting might lean towards delaying significant decisions until September.

A notable risk could arise from secondary sanctions. Washington might target countries like China, India, and Turkey to pressure Russia and its oil buyers.

Despite these potential risks, cross-market volatility levels continue to decline. Barring a major shock, August appears set for low volatility.

Cross-Market Volatility Is Subdued

Carry on Carry Trading

Low volatility naturally shifts focus to the carry trade. This strategy profits from the difference in interest rates between two currencies, assuming the higher-yielding currency does not depreciate enough to offset the interest gains. For example, the Egyptian pound offers annual interest exceeding 20% and has appreciated against the dollar, yielding a 15% total return year-to-date.

Emerging markets are a prime hunting ground for high yields, often linked to higher inflation and sovereign risks. FX investors access these yields via deliverable and non-deliverable FX forward markets.

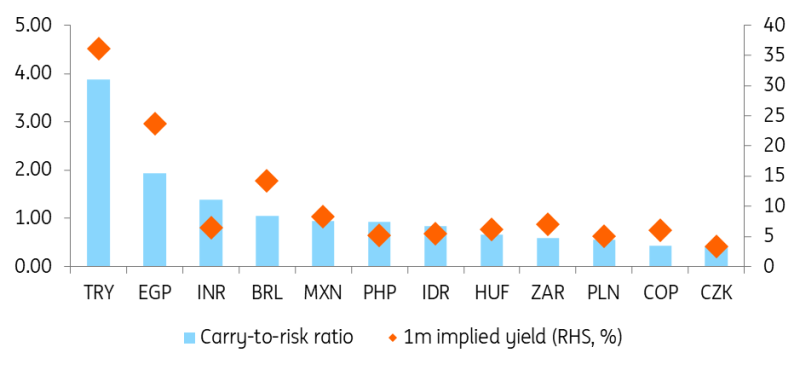

However, high yields must be evaluated against risk. The “carry-to-risk” ratio, which adjusts one-month yields by expected volatility from the FX options market, is crucial. Notably, volatility-adjusted returns show the Turkish lira and the South African rand leading, with the Turkish lira being more attractive than Brazil’s real despite Brazil’s higher interest rates.

Carry-to-Risk Ratios – or Volatility-Adjusted Implied Yields

Back Testing – A Few Important Points

When engaging in carry trades, selecting a funding currency is as critical as choosing the high-yielding currency. Traditionally, the Japanese yen has been favored for funding due to its low borrowing costs, around 0.3% annually. The Swiss franc is also an inexpensive funding option. For those with a directional conviction, the U.S. dollar has been popular, though borrowing costs have been higher, above 4% annually.

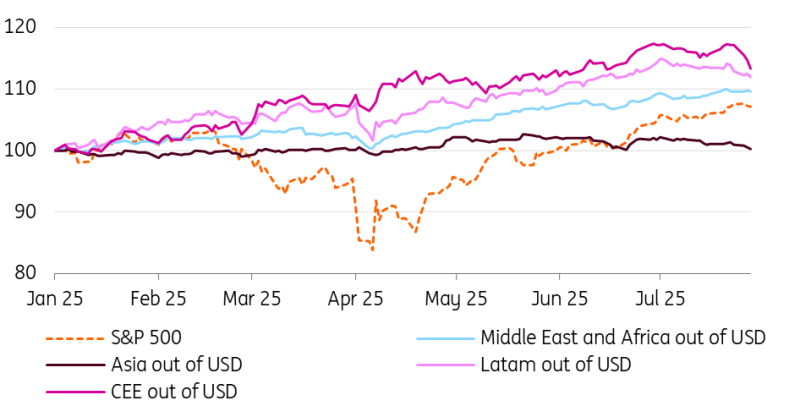

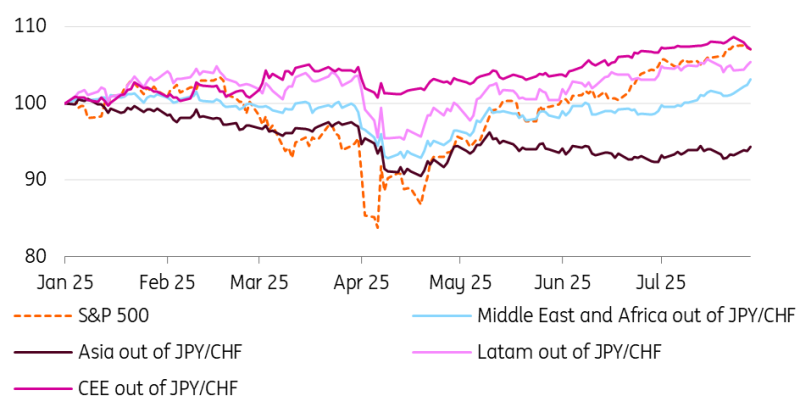

This analysis examines emerging market high-yielders across four blocs: Middle East and Africa (Turkey, Egypt, South Africa), Asia (India, Indonesia, Philippines), Latin America (Brazil, Mexico, Colombia), and Central and Eastern Europe (Poland, Hungary, Czech Republic).

These blocs were backtested year-to-date using equally weighted baskets, funded either by the U.S. dollar alone or by a 50/50 basket of the yen and Swiss franc.

Carry Trade Strategies Funded Out of USD

Carry Trade Strategies Funded 50:50 Out of Yen and Swiss Franc

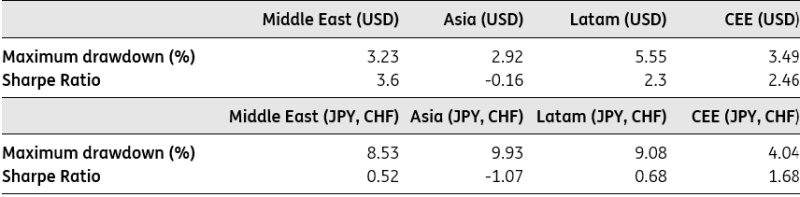

Key financial metrics like maximum drawdown and the Sharpe Ratio, which measures risk-adjusted returns, offer further insights into these strategies.

Financial Metrics of Carry Trade Strategies

Some Observations

- Carry trades funded by the dollar have outperformed year-to-date, a trend likely linked to the dollar’s decline. However, funding through the yen and Swiss franc has resulted in larger maximum drawdowns. This suggests that emerging market currencies, outside of Europe, often move in relation to the dollar, potentially limiting adverse reactions unless a crisis occurs.

- The outperformance of Central and Eastern European currencies is largely tied to the EUR/USD rally, with gains stemming more from spot price movements than interest returns. A call on EUR/USD will be a key driver for this bloc in August. Asia has underperformed, exhibiting high drawdowns and low Sharpe Ratios, making it less attractive for carry trades. Latin America and the Middle East blocs have performed well, though they are susceptible to setbacks, such as the Turkish lira’s sharp fall in mid-March.

The Road Ahead in August

If U.S. data and tariff developments do not disrupt expected quiet trading conditions, carry trade strategies could see continued demand in August. Dollar-funded carry trades have led the pack this year, and following a July bounce, they may remain popular.

Our view is that EUR/USD is likely to find support around the 1.13 level this month, which could favor Central and Eastern European strategies, essentially making it a directional play rather than a pure carry trade.

In the CEE region, investors may be cautious about potential fiscal giveaways in Hungary before next year’s elections. However, this risk is unlikely to deter those seeking the attractive 6% implied yields in the forint. The Czech koruna is expected to remain stable, supported by a hawkish Czech National Bank. The Polish zloty appears to have limited downside risk.

Latin America offers high yields, with the U.S.-Brazil tariff dispute posing the main risk. Tariffs have been raised to 50%, primarily for political reasons, but carve-outs exist for certain products. A seven-day delay in implementation offers hope for a negotiated settlement. Mexico still faces tariffs on goods outside the U.S.-Mexico-Canada Agreement (USMCA). After a notable correction in the Mexican peso to around 18.85, with potential to rise above 19.00, carry trade investors are expected to return to the peso.

For carry trades in Turkey and Egypt, investors may want to remain patient through August. Following a setback for the lira in March, market participants are closely watching Turkish politics. A key court case regarding the eligibility of Özgür Özel to lead the opposition Republican People’s Party (CHP) has been adjourned to September.

Foreign holdings of Egyptian treasury bills are likely substantial. In March, foreign investors held $38 billion, nearly 50% of the total stock. Investments from the UAE, FX liberalization, and higher real rates have supported the Egyptian pound. The South African rand, while part of the Middle East and Africa carry basket, might face more vulnerability this month due to its position within the BRICS bloc.

Asia does not present a compelling case for August. A significant geopolitical risk could be a spike in oil prices if Washington pushes for a ceasefire in Russia. Higher oil prices would negatively impact India and the Philippines, with India potentially facing temporary higher tariffs. Turkey, with its substantial FX reserves, may be better positioned than India to weather currency fluctuations from such oil price movements.