For years, environmental, social, and governance (ESG) criteria were treated by real estate investors as a secondary luxury—a “nice-to-have” certification that looked good in a brochure but rarely moved the needle on a balance sheet. That era is ending.

In the high-growth markets of Southeast Asia, a fresh financial reality is taking hold. Climate resilience is no longer a matter of corporate social responsibility; it has turn into a primary driver of asset valuation, liquidity, and long-term cash flow. This shift is most visible in the emergence of bienes raíces adaptativos en Vietnam, where the physical reality of a sinking landscape is forcing a radical rethink of how property is priced and developed.

The transition is being driven by a brutal intersection of geography and economics. As global temperatures push past the 1.5°C threshold above pre-industrial levels, the cost of “business as usual” is skyrocketing. According to Savills World Research, 2024 stood as the hottest year on record, contributing to global insured losses that reached approximately $368 billion. For investors, this has translated into a sharp rise in property insurance premiums and a growing urgency to pivot capital toward assets that can actually survive the next decade of weather volatility.

The Sinking Valuation of Ho Chi Minh City

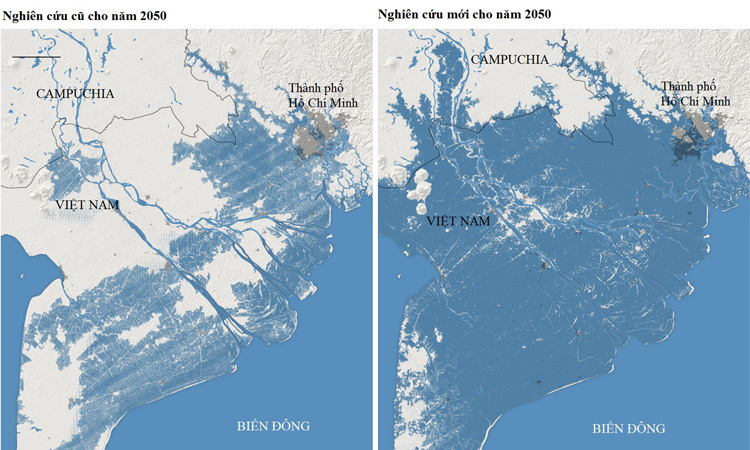

Nowhere is the tension between urban growth and environmental decay more acute than in Ho Chi Minh City. As a sprawling extension of the Mekong Delta, the city is battling a three-pronged threat: rising sea levels, intensifying torrential rains, and land subsidence.

The data reveals a city under siege. The number of flood-prone zones in Ho Chi Minh City has more than doubled, growing from 76 to 159. In many monitoring stations, high tides now frequently exceed 1.8 meters, effectively neutralizing the city’s urban drainage systems. More alarming is the rate of subsidence; the land is sinking at an average rate of 2 centimeters per year, with some hotspots plunging by as much as 7 to 8 centimeters annually. In certain districts, the accumulated subsidence over the last decade ranges between 20 and 50 centimeters.

From a financial analyst’s perspective, this transforms climate risk from a “cyclical” event—something that happens every few years—into a linear, long-term depreciation of the asset. When a property is physically sinking and increasingly inaccessible during high tide, its market value must reflect that permanent impairment.

A Divergence in Asset Performance

Vietnam’s ambition to push its urbanization rate above 50% by 2030 is creating a massive demand for new infrastructure, but this growth is creating a stark divide in the market. We are seeing a “resilience divergence” where properties are being split into two distinct classes: those that can adapt and those that will become stranded assets.

In the industrial sector, the shift is already underway. Next-generation industrial parks are moving toward “eco-models,” integrating renewable energy and sustainable drainage to ensure that supply chains aren’t severed by a single storm. Similarly, the office market is seeing a flight to quality. Grade A buildings with LEED or EDGE certifications are increasingly preferred by international tenants who view these standards as a proxy for operational stability and lower long-term costs.

In the residential sector, the criteria for “prime” real estate are shifting. While location and luxury finishes still matter, buyers are increasingly scrutinizing ground elevation, the sophistication of local drainage systems, and the presence of permeable green spaces that can absorb floodwaters.

| Sector | Key Resilience Drivers | Financial Impact |

|---|---|---|

| Industrial | Renewable energy, eco-park infrastructure | Supply chain continuity, lower risk premiums |

| Office | LEED/EDGE certifications, energy efficiency | Higher occupancy rates, premium international rents |

| Residential | Land elevation, advanced drainage, green space | Price stability, lower vacancy in flood-prone areas |

The New Investment Cycle

The current market climate is defined by caution. High interest rates have slowed general demand, but the scarcity of truly resilient supply is keeping prices firm for high-quality assets. Troy Griffiths, a senior advisor at Savills Vietnam, notes that in this volatile environment, investors and tenants are prioritizing projects that can guarantee functionality during extreme weather events.

The consensus among market experts is that climate adaptability will no longer be a competitive advantage—it will be a baseline requirement for preserving asset value. Without a cohesive public policy that integrates climate data into urban planning and flood control, the cost of inaction will be borne by the broader economy, not just the individual developer.

Disclaimer: This article is intended for informational purposes only and does not constitute financial or investment advice.

The next critical benchmark for the region will be the integration of adaptive standards into official urban zoning laws, as Vietnam continues to navigate its 2030 urbanization goals. The ability of the government to synchronize infrastructure investment with private development will determine whether Ho Chi Minh City can sustain its growth or if the water will eventually dictate the city’s limits.

Do you believe climate resilience should be a mandatory part of property appraisals? Share your thoughts in the comments or share this analysis with your network.