Banks (photo by Magma Images)

In December, the banking system provided consumer credit to the considerable extent of NIS 4.3 billion. This credit is very profitable for the banking system (because of the high interest rates) and is good for the economy that absorbs this money through ‘private consumption’. The big problem starts when the credit takers, the households, take too much credit at too high an interest rate that will make it difficult for them in the future.

The obvious should also be said and that is that when the interest rate rises, the credit becomes more expensive and that means that the monthly payments on the loans rise and so on. When this happens the weaker households start taking loans to pay off other loans and this is where we enter a spiral. The stronger households take out loans that burden them (very much) up the road and this creates a problematic situation for everyone.

More in-

So if we understand the dynamics, it is obvious that the banking system will ask to give consumer credit when those who do not need it, would do well not to take it. And those who do need it, would do well to plan their steps wisely, certainly when we are heading for an economic slowdown, not to mention a recession.

You have to remember (again, the obvious) that the economy is entering an economic slowdown (not to say a recession) the labor market is affected either by waves of layoffs or by reductions in wages/bonuses and so on and this impairs the ability of households to deal with excessively large repayments of consumer loans.

Another thing to keep in mind is that when inflation rises, it means that prices rise, therefore in order to maintain the standard of living to which the average household in Israel is accustomed, it must spend more money, and if incomes do not rise accordingly (and for the most part they do not rise), then in order to bridge the gap or lower the standard of living or taking loans to maintain it. And this is already a problematic situation.

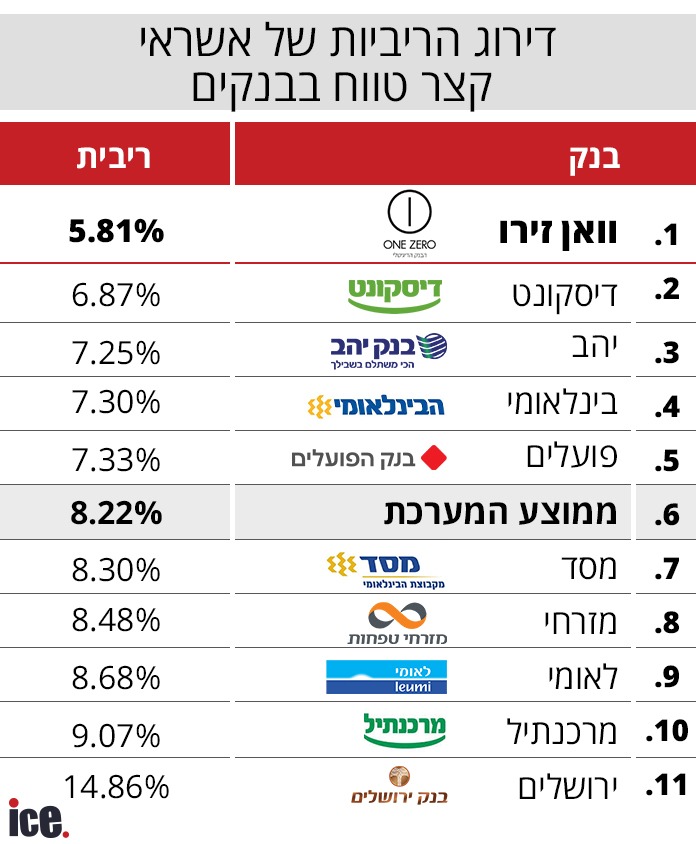

The Bank of Jerusalem responded: “The interest rates charged by the Bank of Jerusalem relate to unsecured loans to customers who do not maintain a current account at the Bank of Jerusalem, and the risk component in them is much more significant, and therefore the interest pricing is high. The comparison to other banks that grant loans to their current account customers is incorrect.”

Comments to the article(0):

Your response has been received and will be published subject to the system policy.

Thanks.

for a new comment

Your response was not sent due to a communication problem, please try again.

Return to comment