In recent months, there has been a change in behavior among those who traveled abroad. After the Government devalued the official exchange rate in December and modified the taxes that govern the tourist dollar, to bring the price above $1,400, in March Argentines moved even further away from credit cards to pay for their consumption in dollars.

This is clear from the report by the private consulting firm First Capital Group, which reported that credit card purchases in dollars totaled US$346 million in March.which meant a decrease of 0.9% compared to the previous month. In the last 12 months the increase was 52.4%, although the behavior was irregular and alternated between monthly increases and decreases, depending on the price at that time.

“The fall in ‘deregulated’ exchange rates versus the exchange rate applied to card consumption causes users to limit operations”said Guillermo Barbero, partner at First Capital Group. By way of contrast, the MEP dollar closed last Friday at $1,000, while the card exchange rate was quoted at $1,410 at Banco Nación. That is, it is a difference of $410 per dollar, so a traveler can save up to 41% if they choose between one payment method or another.

The use of credit cards in pesos also fell, even though at the beginning of this year the Government launched the Cuota Simple financing program to try to support consumption. In March, transactions for $6,523,158 million were recorded, which meant a nominal increase of 5.1% compared to the previous month. This value is below the inflation projected for that month, which would have ranged between 10% and 13%, according to economic consultants.

“This is a particular month, since the last days of the month have been holidays – Holy Week – and also coincide with a period during which plastic money is traditionally used more frequently and that may differ the calculation of operations towards the following month, so the analysis of the variations can lead to less precise interpretations,” Barbero clarified. Anywayyear-on-year growth was 166.9%, so it would also be below inflation in the same period.

Furthermore, in March private financing was contracted. Even though there was a drop in interest rates and better credit offersloans to the private sector reached a level of $20.1 trillion, which represented a nominal increase of 6% compared to February. The interannual variation was 145.7%, while the inflation forecast for the same period would be around 290%. “Despite the greater supply of credit to the private sector by financial entities, portfolios continue to contract in real values, since nominal increases are not enough to compensate for the fall in the value of the currency,” Barbero added.

When observing specific cases, the personal loan line recorded a jump of $2,488,714 million, a nominal increase of 8.3% monthly. For the partner of First Capital Groupexpectations of layoffs and suspensions in the short term They do not allow demand to “take off,” so family projects that require debt are “relegated for the months to come.”

The line of mortgage credits had a decrease of 1.4% and closed March with a total balance of $590,731 million. While the line collateral credits presented a portfolio balance of $1,090,206 million, which grew by a nominal 5.1% compared to February. Lastly, the commercial loans had a balance increased by 7.6%, up to $8,242,617 million.

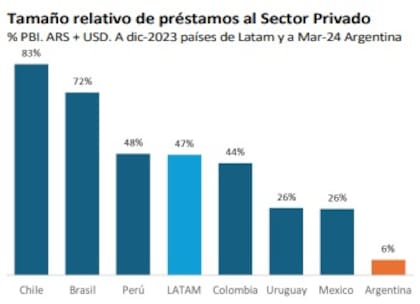

“In Argentina, loans from banks in pesos to the private sector (individuals, companies, families) add up to 6% of GDP, less than a seventh of what was registered in the region“, they noted in Quantum Finance. On the average for Latin America, this ratio is 47%, while countries such as Chile (private loans are 83% of GDP), Brazil (72%) and Peru (48%) stand out.