For millions of Americans, a credit score is more than just a number; It’s a financial passport that determines the cost of a mortgage, the ability to lease a car, or the likelihood of securing a competitive insurance rate. However, recent data indicates that this passport is becoming harder to maintain. The national average FICO score has seen a downward trend, driven largely by a rise in missed or late payments as households grapple with persistent inflation and higher borrowing costs.

While a dip in credit standing can perceive like a permanent setback, financial experts suggest that the path to recovery is often more direct than consumers realize. According to guidance from Fidelity, the fastest way to raise your credit score involves targeting the two most influential components of the FICO model: payment history and credit utilization. While payment history carries the most weight, it is as well the slowest to repair. For those seeking a more immediate impact, managing the credit utilization ratio offers a strategic “fast track” to a higher score.

Understanding the mechanics of these scores is essential for anyone looking to improve their creditworthiness. The FICO score, used by the vast majority of lenders in the U.S., is not a static reflection of financial health but a calculated risk assessment based on five distinct categories of data. When the national average drops, it is typically because a significant portion of the population has slipped in the most critical category: the consistency of their payments.

The Heavyweight: Why Payment History Dominates

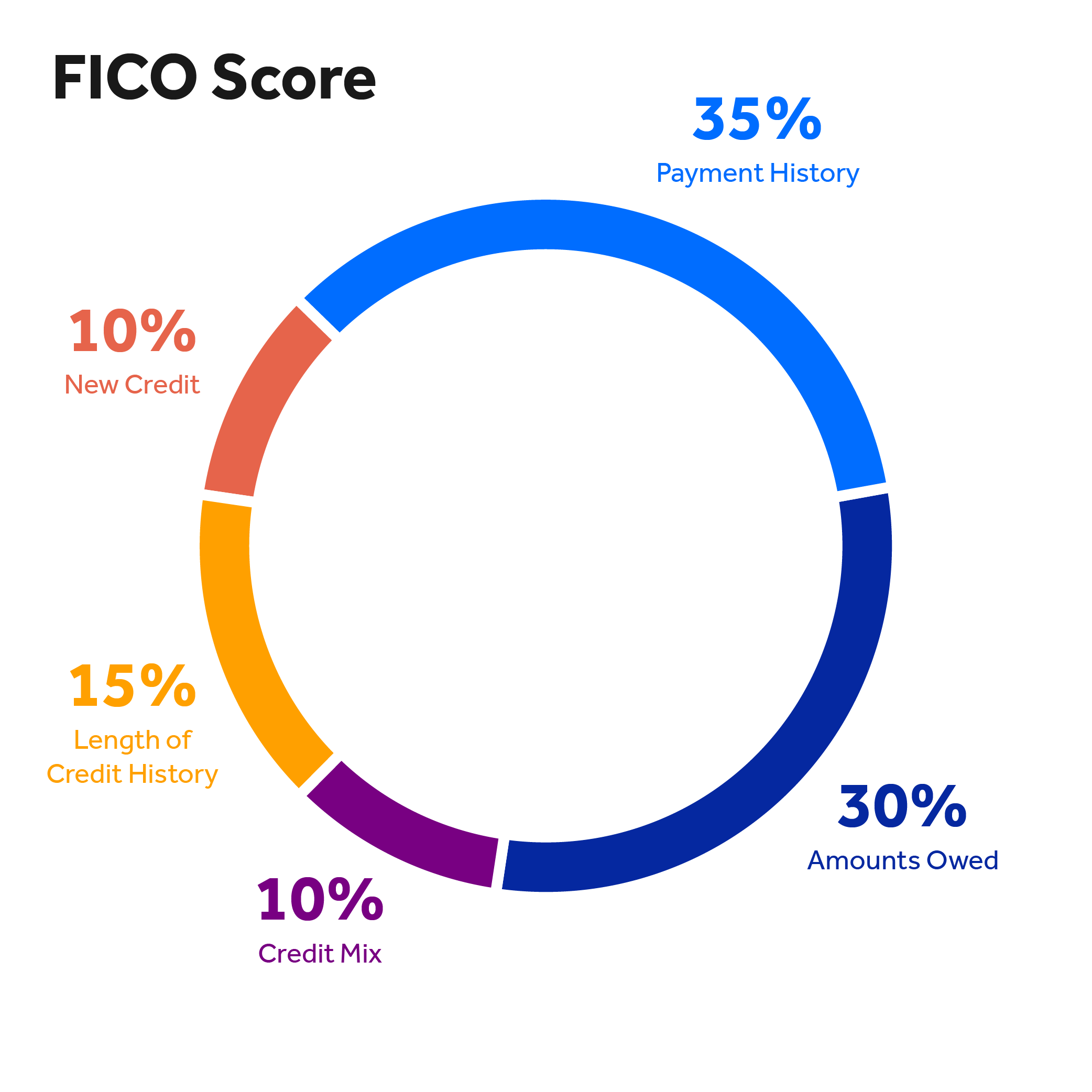

Payment history is the single most important factor in determining a credit score, accounting for 35% of a FICO score. This metric tracks whether a borrower pays their bills on time, the frequency of late payments, and the severity of any delinquencies. Because this category is so heavily weighted, even a single 30-day late payment can cause a significant drop in a previously high score.

The challenge with payment history is the timeline. Negative marks, such as late payments or accounts sent to collections, typically remain on a credit report for seven years. While the impact of a late payment fades over time—provided no new misses occur—there is no “quick fix” to erase a legitimate delinquency. The only verified method to address incorrect reporting is through a formal dispute process with the credit bureaus.

For those whose scores have dropped due to missed payments, the primary goal is stabilization. Establishing a foolproof system for on-time payments—such as autopay for minimum balances—is the first step in stopping the bleed. Once the payment behavior is corrected, the focus can shift to the second-most influential factor for a faster recovery.

The Fast Track: Optimizing Credit Utilization

If payment history is the long game, credit utilization is the short game. This metric, which makes up 30% of the FICO score, measures how much of your available revolving credit you are currently using. It is calculated by dividing your total credit card balances by your total credit limits across all accounts.

Fidelity highlights the utilization ratio as the second-fastest way to influence a score because, unlike payment history, utilization has no “memory” in the FICO model. While some newer scoring models may consider trends, the traditional FICO score primarily looks at your current balance. If a consumer pays down a large credit card balance today, their score can potentially rebound as soon as the credit card issuer reports the new, lower balance to the bureaus—usually within a few days to a month.

Financial analysts generally recommend keeping utilization below 30%, but those aiming for the highest possible scores often strive for a ratio under 10%. There are two primary ways to lower this percentage quickly:

- Aggressive Debt Reduction: Paying down existing balances directly reduces the numerator in the utilization equation.

- Increasing Credit Limits: Requesting a limit increase from a credit card issuer increases the denominator. If the limit is raised and the spending remains the same, the utilization percentage drops automatically.

requesting a credit limit increase can sometimes trigger a “hard inquiry,” which may cause a temporary, minor dip in the score. However, for most borrowers, the benefit of a lower utilization ratio far outweighs the small hit from a hard pull.

Decoding the FICO Composition

To visualize how different financial behaviors impact a score, it is helpful to gaze at the weighted breakdown of the FICO model. While utilization and payments are the primary levers, the remaining 35% of the score is composed of factors that require more time and patience to influence.

| Factor | Weight | Impact Speed |

|---|---|---|

| Payment History | 35% | Slow (Years) |

| Amounts Owed (Utilization) | 30% | Fast (Days/Weeks) |

| Length of Credit History | 15% | Very Slow (Decades) |

| Credit Mix | 10% | Moderate (Months) |

| New Credit Inquiries | 10% | Fast (1 Year) |

Managing the Remaining Levers

Beyond the “big two,” borrowers can optimize their scores by managing the remaining components. The length of credit history (15%) rewards those who keep old accounts open, even if they are not frequently used. Closing an old credit card account can inadvertently lower a score by reducing the average age of accounts and simultaneously increasing the utilization ratio.

The credit mix (10%) refers to the variety of accounts a borrower holds, such as a combination of revolving credit (credit cards) and installment loans (mortgages, auto loans, or student loans). While it is not advisable to grab out a loan solely to improve a score, a diversified portfolio suggests to lenders that the borrower can handle different types of debt responsibly.

Finally, new credit (10%) tracks how many accounts have been opened recently. Frequent applications for new credit in a short window can signal financial distress to lenders, leading to a temporary score decrease. This is why experts suggest spacing out credit applications by several months.

Disclaimer: This article is for informational purposes only and does not constitute financial, investment, or legal advice. Credit scoring models can vary, and individual results may differ based on personal financial history.

As the Federal Reserve continues to monitor inflation and adjust interest rates, the cost of carrying revolving debt remains high. Consumers should look for the next quarterly report on consumer credit trends from the Federal Reserve to understand how broader economic shifts are affecting national delinquency rates and credit availability.

Do you have a strategy for managing your credit utilization, or have you seen a recent shift in your score? Share your experiences in the comments below.