The political and economic developments in France after the elections are disturbing the markets as they try to assess the risks and challenges that arise. Bond markets have been in turmoil for weeks, with borrowing costs from France to Italy, Spain and Greece under increasing pressure. There are currently three scenarios for the day ahead in Europe’s second largest economy, and two of them are the most worrying, while the third scenario poses particular challenges.

These are worrying: First, an election result in which neither the extreme right nor the united left nor Macron’s centrists win a majority. Secondly, the possible cooperation of Le Pen with part of the Left for the coalition government. Thirdly, the majority of seats with Le Pen and her wait-and-see attitude following more moderate policies similar to those followed by Italian Prime Minister Giorgia Meloni.

The far right defeat leaves France in shock and chaos

These three cases are presented in a report by investment bank Berenberg and relate to the markets in an environment where investors and institutions, from the European Central Bank to the International Monetary Fund and Brussels, are watching anxiously the pressure on the production. on French government bonds and the entire Eurozone.

It is indicative that the Governor of the Bank of Greece (BoG), Mr. Giannis Stournaras, made specific reference to the developments in France in the BG’s Monetary Policy Report. As he reported, in early June, sovereign bond yields in the eurozone rose again, following the downgrade of France’s sovereign credit rating and the increase in volatility following the euro elections.

Three Berenberg cases

The investment bank Berenberg identifies specific situations for the French elections.

-The “goal”: The most likely result is still a parliament in which neither the far-right nor the United Left nor the centrist Macron can gather a majority. In this case, no new government would be able to move flexibly, as stated.

-The “end worse than dead”. It concerns the possibility that Le Pen’s party and parts of the left could come together to moderate Macron’s pension reform and increase spending, for example through VAT cuts or additional subsidies. Such a development could throw off the country’s already troubled public finances

-The “Marin Meloni” script. Less likely to happen, the house reckons, is that Marine Le Pen’s party could win a majority of seats and install RN leader Jordan Bardela as prime minister. This would be done with the aim of focusing on winning the 2027 presidential election, staying in the more moderate way he expressed during the election campaign. With such a move, Le Pen could try to follow Italian Prime Minister Giorgia Meloni’s lead to a large extent, reports Berenberg. To do this, she can explain to RN voters after a long budget review that most of her initial budget ideas could only be implemented later and over time – or if she is elected president in 2027 .

France’s fiscal problem

With a budget deficit of 5.5% of GDP and public debt rising to 110.6% of GDP in 2023, France faces significant fiscal challenges. To get back on track, the government is likely to have to save up to €25bn in the draft 2025 budget this autumn. But a new government under National Rally Le Pen (RN) could increase spending even more. Such fiscal stimulus could boost GDP in the short term, but the potential rise in risk premiums on French government bonds could be negative for the country, Berenberg said in a previous report.

These three main scenarios suggest that the outlook for France is gradually deteriorating and there is little further progress on key European issues. But they don’t point to an imminent Liz Truss debt crisis, according to the investment house.

Other international houses and banks are not as positive, however. Citi warned clients in notes about market turmoil as reflected in rising risk premiums. In the bond market in particular, investors were worried about plans to raise taxes and boost spending by the right-wing Marie Le Pen party and the left-wing Nouveau Front Populaire (NFP) coalition. Economists have warned that if one of those parties wins a majority and pushes ahead with the economic proposals it put forward before the elections, the state of the markets could even lead to a new debt crisis in the Eurozone, this time through France.

The complex electoral system

France’s complex two-round voting system makes it very difficult to estimate the final distribution of seats – which will be governed by a majority, even if this is not done without a coalition. Three of the country’s biggest polling firms estimate that the RN could win between 230 and 295 seats. With 289 seats needed for a majority and taking into account the huge margin of maneuver in the second round, the RN has little chance of forming a government on its own, according to Politico.

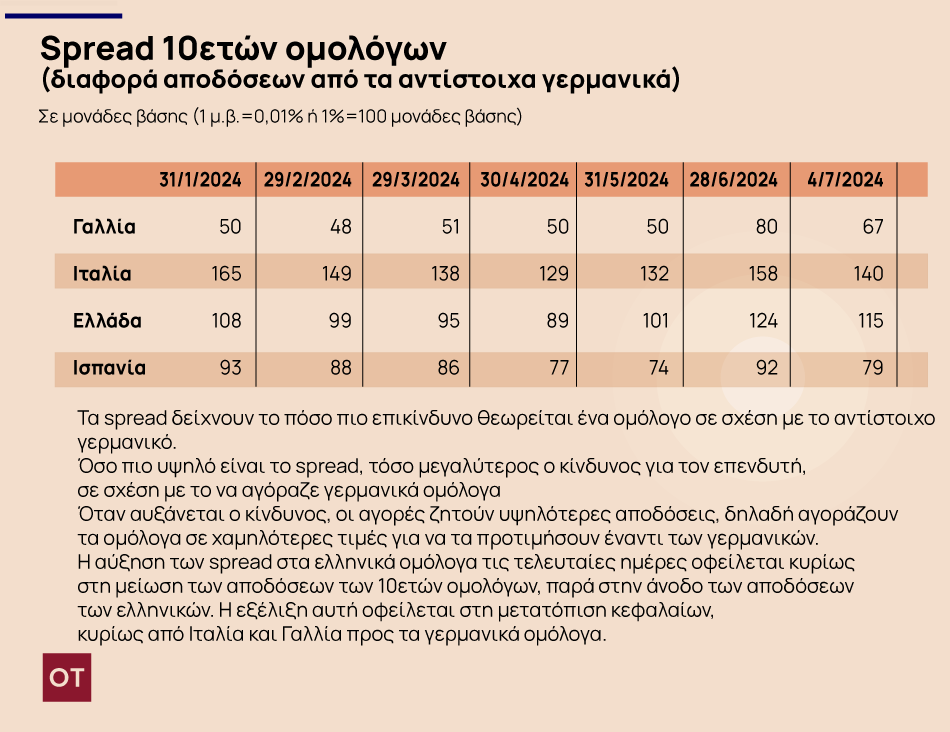

French and Eurozone government bonds under the microscope

Already, French 10-year government bond yields have risen 23 basis points to 3.25% in the past month, closing in on Spain’s.

The European Central Bank is carefully monitoring the developments, and ECB officials said it is still too early to make any assessment.

Markets and the ECB are concerned that developments could be such that investors flee French bonds that central bank intervention is needed if France suffers a “Liz Truss moment” – the debt crisis caused by tax cuts unfunded former British Prime Minister Liz. Truss in 2022.