For years, the political landscape of the United Kingdom was defined by a hard line: you were either for the exit or against it. But as the dust settles on the most disruptive constitutional shift in modern British history, a new term has entered the lexicon to describe the prevailing mood across the British Isles: “Bregret.”

This sentiment of Brexit regret is no longer confined to the “Remain” camp. It has evolved into a broader, cross-partisan realization that the promised dividends of total sovereignty—unfettered trade deals and a reclaimed border—have been eclipsed by systemic economic friction and a persistent cost-of-living crisis.

The shift is visible in the data and the daily lives of citizens. From the bureaucratic hurdles facing small businesses exporting to the continent to the labor shortages in hospitality and agriculture, the reality of life outside the European Single Market has proven more cumbersome than the campaign slogans suggested. The transition from the optimism of 2016 to the pragmatism of 2025 reflects a nation grappling with the tangible costs of its independence.

The Economic Weight of Sovereignty

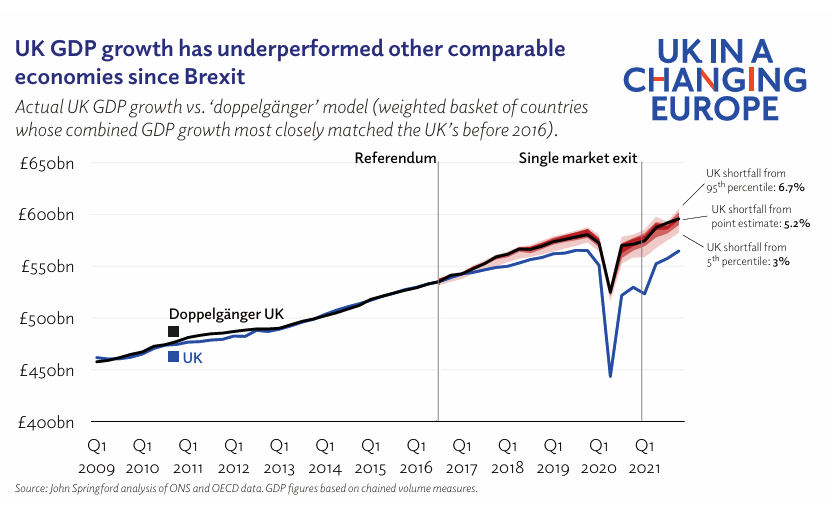

The most quantifiable evidence of this shift lies in the UK’s macroeconomic performance. The Office for Budget Responsibility (OBR) has consistently noted that the UK economy is smaller than it would have been had it remained within the European Union. According to OBR analysis, Brexit is estimated to have reduced the UK’s potential GDP by approximately 4% in the long term.

While the UK avoided a total collapse, the “slow puncture” effect has been more damaging. The implementation of the Trade and Cooperation Agreement (TCA) introduced non-tariff barriers—customs declarations, sanitary checks, and regulatory divergences—that have disproportionately harmed small and medium-sized enterprises. For many, the dream of “Global Britain” has been hindered by the reality that the EU remains the UK’s most vital and accessible trading partner.

| Key Pillar | Campaign Promise | Current Status |

|---|---|---|

| Trade | Faster, global trade deals | Increased friction with EU; limited gains from new deals |

| Labor | “Taking back control” of borders | Acute shortages in social care and agriculture |

| Economy | GDP boost from deregulation | Long-term potential GDP contraction of ~4% |

| Sovereignty | Full regulatory autonomy | Ongoing negotiation over Northern Ireland/Windsor Framework |

A Shift in Public Sentiment

The psychological pivot toward “Bregret” is mirrored in public polling. Data from YouGov has frequently indicated that a majority of British voters now believe the decision to exit the EU was a mistake. This trend suggests that the initial emotional appeal of sovereignty has been worn down by the daily pressures of inflation and stagnant growth.

This shift is not merely about economics; it is about the perceived loss of influence. The UK now finds itself as a “third country,” navigating the complexities of the Trade and Cooperation Agreement, often reacting to EU regulatory changes rather than helping to shape them. For the professional class and the youth, the loss of freedom of movement has removed a critical layer of opportunity and cultural exchange.

The Labor Gap and the Cost of Living

One of the most acute points of friction has been the labor market. The end of freedom of movement created a vacuum in sectors heavily reliant on EU workers. The hospitality, construction, and social care sectors have struggled to fill gaps, contributing to higher service costs and longer wait times for essential care. While the government attempted to solve this with new visa schemes, the administrative burden has often outweighed the benefits for employers.

the “cost of living crisis” has been exacerbated by Brexit-related import costs. Increased tariffs and customs checks on food and chemicals from the EU have added layers of cost that are ultimately passed down to the consumer, making the grocery bill a primary driver of “Bregret” for the average household.

The Political Path Forward

The current administration under the Labour Party faces a delicate balancing act. While there is a clear appetite among the electorate to reduce friction with Europe, there is little political will to reopen the wound of a full membership referendum. The strategy has shifted from “reversing” Brexit to “making Brexit work.”

This involves seeking closer alignment on specific regulatory standards—particularly in chemicals and veterinary checks—to ease trade without returning to the Single Market or the Customs Union. The goal is a “reset” of the relationship, focusing on security cooperation and a veterinary agreement that could significantly reduce border delays.

The situation in Northern Ireland remains the most complex piece of the puzzle. The Windsor Framework was designed to alleviate tensions by creating “green” and “red” lanes for goods, but the region remains a litmus test for whether the UK can maintain its integrity while acknowledging the unique economic necessity of the Irish border.

As the UK moves further away from the 2016 vote, the conversation has transitioned from ideological warfare to a search for stability. The next significant checkpoint will be the upcoming bilateral reviews of the TCA, where both London and Brussels will assess whether the current trade arrangements are sustainable or if a more comprehensive alignment is required to prevent further economic stagnation.

This article is provided for informational purposes and does not constitute financial or legal advice regarding trade or immigration.

We invite our readers to share their perspectives on the current state of UK-EU relations in the comments below. Please share this report with your network to join the conversation.