Healthcare M&A Surges to Record Highs as AI Investment Faces Reality Check

Table of Contents

Despite a massive influx of capital, artificial intelligence is proving to be an “additive” rather than “disruptive” force in healthcare, according to a new report.

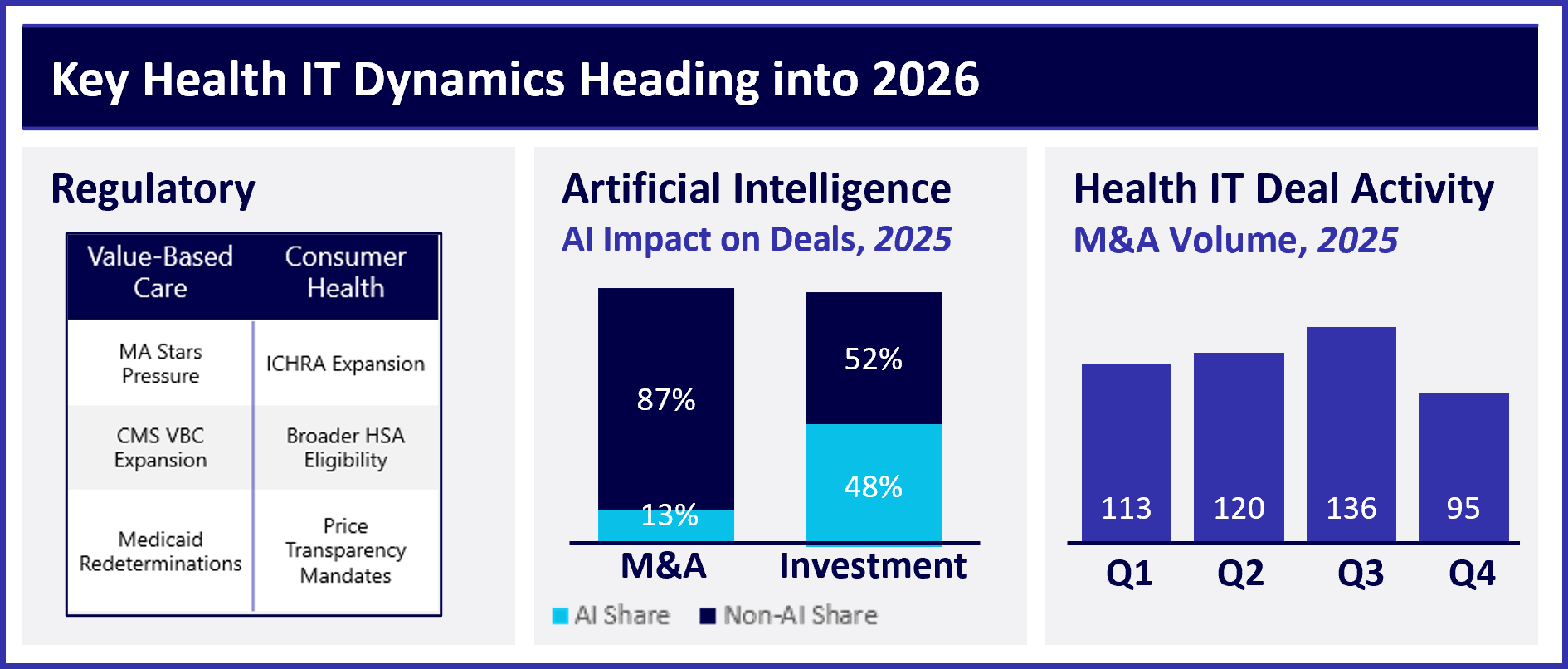

The healthcare technology sector is experiencing a surprising rebound, but a critical shift is underway. A January 2026 market review from Healthcare Growth Partners (HGP) reveals a surge in mergers and acquisitions (M&A) activity, reaching an all-time high in the third quarter of 2025 with 136 deals. However, the report also underscores a sobering truth: two decades of digital transformation have failed to deliver significant economic improvements, with U.S. healthcare spending nearly doubling from $2.5 trillion to $5.3 trillion since HGP’s founding.

The Economic Disconnect

While Health IT has successfully modernized workflows and data capture, its impact on overall healthcare costs and patient outcomes has been limited. “Health IT has meaningfully modernized workflows and data capture,” one analyst noted, “while its impact on outcomes and its economic value has been limited.” This realization is driving a market correction, moving the industry away from a focus on “regulatory compliance” and toward “economic accountability” as inflation moderates to 2.6% and interest rates ease.

The AI Paradox: Hype vs. Reality

Perhaps the most striking finding of the HGP report is the disconnect between investment in artificial intelligence (AI) and actual market activity. In 2025, a full 50% of U.S. Health IT investment dollars flowed to AI-native companies, fueled by the expectation of disruptive innovation. Yet, only 13% of M&A and buyout transactions involved companies heavily marketing AI capabilities.

Strategic buyers, it appears, are prioritizing established businesses with “revenue durability” and “embedded workflows” over unproven algorithms. As one company release stated, acquirers are “buying the track, not the train.” This suggests that incumbents like Epic and Oracle are successfully integrating AI into their existing platforms, rather than being overthrown by new entrants. “So far, AI is proving additive, not existential, for incumbents,” the analysts write.

A Regulatory Divide Emerges

The government’s regulatory approach is further shaping the healthcare landscape, creating two distinct economic models. The Centers for Medicare & Medicaid Services (CMS) is doubling down on value-based care and long-term accountability, exemplified by the new ACCESS model for chronic care. This favors large platforms with robust data capabilities and significant capital.

Simultaneously, affordability concerns are driving a shift toward consumer-directed health solutions, such as Individual Coverage Health Reimbursement Arrangements (ICHRAs) and Health Savings Accounts (HSAs), emphasizing speed, access, and price transparency. Companies attempting to serve both models may face significant challenges. “The result is two parallel investment theses,” HGP notes.

M&A Activity: A Return to Normalcy

Following the inflated valuations of the COVID-19 pandemic, the M&A market has stabilized. Valuations for software companies have settled at 5.1x revenue – a decrease from the 8.1x peak during the pandemic, but still above the pre-pandemic average of 4.6x. The return of a “healthy middle class” in deal-making is also evident in the record-breaking 136 deals completed in the third quarter of 2025.

However, closing these deals requires flexibility. The report highlights a growing trend of “flexible deal structures,” with buyers utilizing earnouts and rollover equity to bridge the gap between cautious valuations and optimistic seller expectations.

The Path Forward: Accountability and Economics

The HGP report suggests that 2026 marks a turning point for the healthcare industry. The focus is shifting away from simply digitizing processes and toward achieving tangible economic results. As HGP concludes, the next decade won’t be shaped by “regulatory incentives” (like Meaningful Use), but by “accountability and economics.” The winners won’t be the ones who digitize the chart; they will be the ones who finally—after twenty years—figure out how to lower the bill.