For many Americans, the wallet has develop into a crowded place. While the allure of cash-back rewards, travel points, and introductory 0% APR offers continues to drive new account openings, a growing number of consumers are beginning to feel the weight of their own portfolios. Recent data suggests a shifting sentiment toward credit management, with one in three Americans with credit cards saying they have too many.

This sense of “card fatigue” comes at a critical time for household finances. As the Federal Reserve has maintained interest rates at elevated levels to combat inflation, the cost of carrying a balance has surged. The psychological burden of tracking multiple payment dates, varying interest rates, and annual fees is beginning to outweigh the marginal benefits of a few extra reward points.

The dilemma is not merely about the number of plastic cards in a wallet, but about the complexity of managing a fragmented financial identity. For some, a diverse mix of cards is a strategic tool for maximizing credit utilization and improving credit scores. For others, it is a recipe for missed payments and accidental debt spirals.

The Psychology of the ‘Reward Trap’

The trend toward over-accumulation often begins with a logical strategy: the pursuit of rewards. Consumers are frequently lured by “sign-up bonuses” that offer hundreds of dollars in value for spending a specific amount within the first few months. Yet, this strategy requires a level of administrative discipline that can become unsustainable as the number of accounts grows.

When a consumer manages five or more cards, the risk of “leakage”—small, forgotten subscriptions or annual fees that travel unnoticed—increases. The temptation to spend more to hit a reward threshold can lead to a disconnect between a person’s actual budget and their spending habits. This phenomenon often leads to the realization that the “free” rewards are actually being paid for through higher spending or interest charges.

Financial analysts note that the impact of having too many cards varies significantly based on the user’s credit discipline. Those who pay their balances in full every month may see a benefit in their credit score due to a higher total credit limit, which lowers their overall credit utilization ratio. However, for those struggling with debt, each new card represents a new potential avenue for overspending.

Evaluating the ‘Ideal Mix’ of Credit

Determining how many cards are “too many” is less about a magic number and more about a person’s ability to track their obligations. A streamlined portfolio generally consists of a few targeted instruments designed for specific purposes.

Most financial planners suggest a core strategy involving three primary types of accounts:

- The Daily Driver: A card with a high cash-back or rewards rate for frequent categories like groceries or gas.

- The Safety Net: A card with a high credit limit and low interest, reserved for genuine emergencies.

- The Specialized Tool: A travel-specific card or a store-branded card used exclusively for high-value, infrequent purchases.

When consumers move beyond this core structure, the administrative overhead begins to climb. Managing ten cards requires ten different logins, ten different statements, and a heightened risk of missing a payment—which can lead to a significant drop in a credit score if a payment is more than 30 days late.

| Strategy | Primary Goal | Key Risk | Management Effort |

|---|---|---|---|

| Minimalist | Simplicity/Control | Lower total rewards | Low |

| Balanced | Utility/Credit Health | Moderate fee tracking | Medium |

| Maximizer | Points/Arbitrage | Overspending/Complexity | High |

The Impact on Credit Scores and Debt

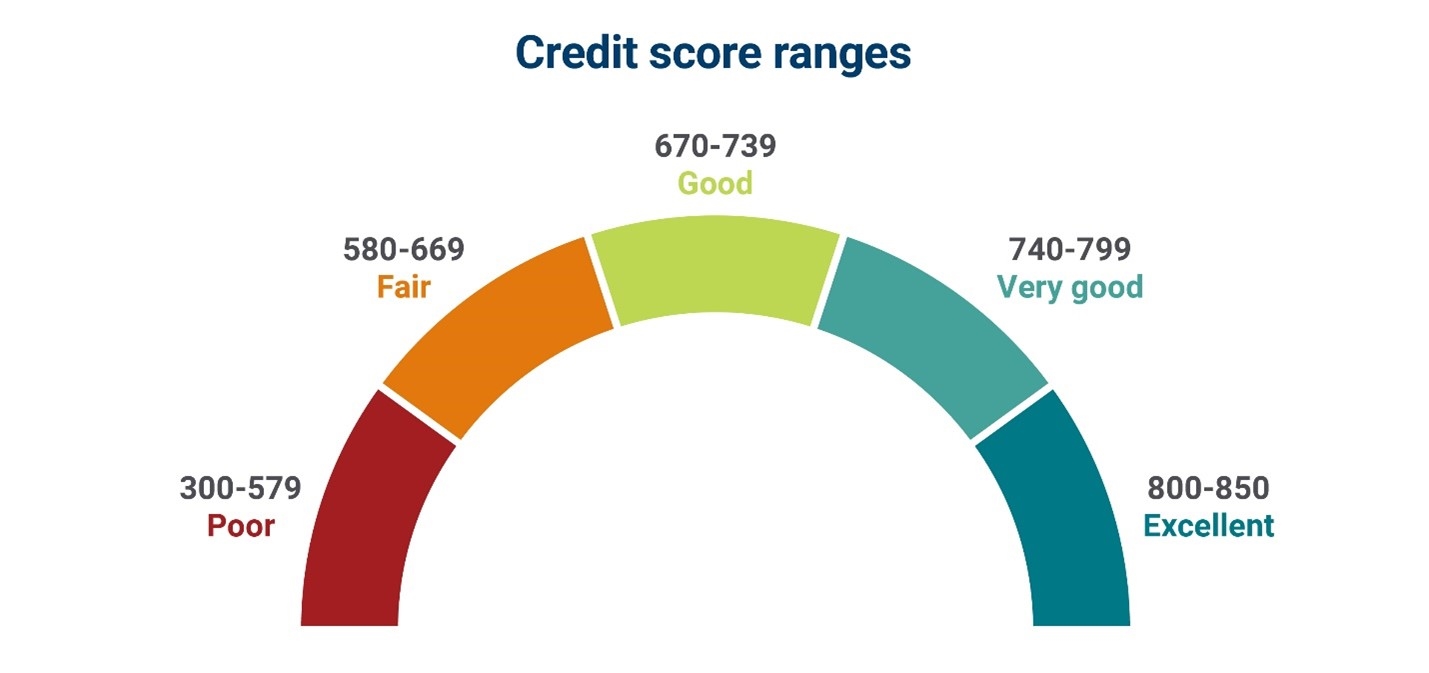

There is a common misconception that closing unused cards automatically helps a credit score. In reality, the opposite can happen. Closing an aged account can reduce the average age of a consumer’s credit history and lower their total available credit, which may inadvertently increase their credit utilization ratio.

However, the danger of maintaining too many open lines of credit is the “invisible debt” factor. When balances are spread across multiple cards, it becomes harder to visualize the total amount of debt owed. This fragmentation can mask the severity of a financial situation until a consumer realizes they are paying interest on several different fronts simultaneously.

For those feeling overwhelmed, the path forward involves a “credit audit.” This process requires listing every open account, its current balance, the annual fee, and the current APR. By identifying cards that provide little value but carry high fees, consumers can begin to prune their portfolios without damaging their credit standing.

Who is most affected?

The burden of “too many cards” is felt most acutely by younger consumers who are aggressive in their pursuit of “credit hacking” and older consumers who have accumulated legacy accounts over decades. Both groups often discover that the digital transition—moving from physical statements to apps—has made it easier to open accounts but harder to maintain a holistic view of their liabilities.

The current economic climate, characterized by volatile pricing for essential goods, makes the simplicity of a few well-managed accounts more attractive than the complexity of a dozen reward-bearing ones. The shift toward “financial minimalism” is a direct response to the mental load of managing a fragmented digital wallet.

Disclaimer: This article is for informational purposes only and does not constitute professional financial, investment, or legal advice. Please consult with a certified financial planner or credit counselor regarding your specific financial situation.

As consumers continue to navigate a high-interest-rate environment, the next major indicator of credit health will be the upcoming quarterly reports from the major credit bureaus, which typically highlight trends in delinquency and account closure rates. These reports will provide a clearer picture of whether Americans are actively downsizing their credit portfolios or continuing to accumulate new lines of debt.

Do you feel you have too many credit cards, or do you prefer a diversified portfolio for the rewards? Share your thoughts and experiences in the comments below.