For most people, the U.S. Dollar is simply the currency used to buy groceries or pay rent. But on the global stage, the dollar functions as something far more consequential: the world’s primary reserve currency. This status means that central banks across the globe hold massive quantities of dollars to stabilize their own economies and facilitate international trade, creating a financial architecture that grants the United States unprecedented economic influence.

While headlines frequently buzz with talk of “de-dollarization” and the rise of alternative trade blocs, the structural reality of the global financial system remains heavily tilted toward the greenback. Understanding why the U.S. Dollar as the world’s reserve currency persists requires looking past current political rhetoric and into the mechanics of liquidity, trust, and a historical legacy that began in the aftermath of World War II.

The current system is not an accident of geography or mere luck, but the result of a series of pivotal shifts in global policy. From the formal agreements of the 1940s to the “Nixon Shock” of 1971, the dollar has evolved from a currency backed by gold into a global utility backed by the strength of the U.S. Economy and its legal institutions.

The Architecture of Dominance: From Bretton Woods to Fiat

The foundation of the dollar’s hegemony was laid in 1944 at the Bretton Woods Conference. With the global economy shattered by war, delegates from 44 nations established a new system where the U.S. Dollar was pegged to gold at $35 per ounce, and all other currencies were pegged to the dollar. This made the dollar the “anchor” of global stability, providing a predictable environment for rebuilding international trade.

However, this system contained an inherent flaw known as the Triffin Dilemma. Named after economist Robert Triffin, the paradox suggests that for the rest of the world to have enough dollars to conduct trade, the U.S. Had to run persistent trade deficits—essentially exporting more dollars than it took back. But running these deficits eventually weakened the confidence that the U.S. Actually had enough gold to back all those circulating dollars.

By 1971, the tension reached a breaking point. Facing rising inflation and a run on gold reserves, President Richard Nixon unilaterally ended the direct convertibility of the U.S. Dollar to gold. This “Nixon Shock” transitioned the world into a regime of floating exchange rates and fiat currency, where the dollar’s value was no longer tied to a physical metal, but to the “full faith and credit” of the United States government.

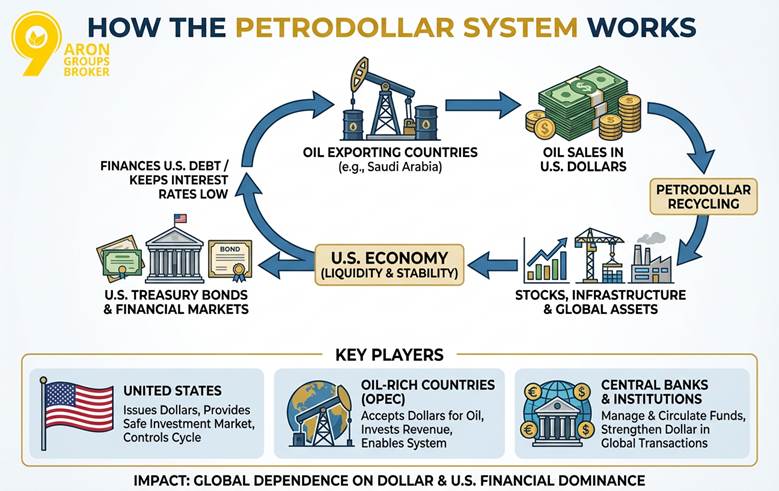

The Petrodollar and the Cycle of Demand

To maintain demand for the dollar after the gold link was severed, the U.S. Entered into strategic arrangements, most notably with Saudi Arabia in the 1970s. This created the “petrodollar” system: oil, the world’s most essential commodity, would be priced and traded exclusively in U.S. Dollars.

This arrangement ensured that every nation needing energy had to maintain reserves of dollars. Many oil-exporting nations reinvested their surplus dollars back into U.S. Treasury securities, creating a circular flow of capital that allowed the U.S. To borrow money cheaply to fund its own government spending. This cycle reinforced the dollar’s utility; the more the world used the dollar for oil, the more liquid the dollar became, and the more attractive U.S. Treasuries became as a safe haven for global savings.

| Era | System | Primary Anchor | Key Characteristic |

|---|---|---|---|

| 1944–1971 | Bretton Woods | Gold / USD | Fixed exchange rates tied to gold. |

| 1971–Present | Fiat / Floating | U.S. Economy | Value based on trust, policy, and trade. |

| Emerging | Multipolar | Diversified | Increased leverage of CNY, EUR, and gold. |

The ‘Network Effect’ and the Difficulty of Exit

Economists often describe the dollar’s dominance through the lens of “network effects.” Similar to how a social media platform becomes more valuable as more people join, a currency becomes more useful as more participants accept it. Because the majority of global trade is invoiced in dollars and the deepest, most liquid bond markets are in the U.S., switching to a different currency is a massive coordination problem.

For a central bank to move its reserves away from the dollar, it must find an alternative that offers similar liquidity—the ability to sell large amounts of the asset quickly without crashing the price. While the Euro and the Chinese Yuan are significant, they lack the same combination of open capital markets and legal transparency. The International Monetary Fund (IMF) data consistently shows that while the dollar’s share of global reserves has declined slightly over the last two decades, it remains the dominant asset by a wide margin.

Beyond liquidity, there is the element of institutional trust. Investors lean toward the U.S. Not necessarily because they agree with U.S. Policy, but because of the predictability of the U.S. Legal system and the independence of the Federal Reserve. In times of global crisis, investors typically flock to “safe haven” assets, which almost always means U.S. Treasuries.

The Modern Challenge: De-dollarization and BRICS

In recent years, the concept of de-dollarization has moved from the fringes of economic theory to the center of geopolitical strategy. The primary catalyst has been the “weaponization” of the dollar. When the U.S. Uses sanctions to cut countries or individuals off from the SWIFT payment system, it signals to other nations that their dollar reserves are subject to U.S. Political will.

This has led to increased cooperation among the BRICS nations (Brazil, Russia, India, China, and South Africa, now expanded), who are exploring ways to trade in local currencies. However, the transition is slow. Trading in local currencies works for bilateral trade—such as India buying oil from Russia in rupees—but it does not yet provide a viable alternative for a global reserve asset that can be used to settle debts with any country in the world.

The challenge for any challenger is not just economic, but political. To replace the dollar, a country would likely need to open its capital markets completely, allowing money to flow in and out freely without government interference—a move that many authoritarian regimes are unwilling to make.

Disclaimer: This article is provided for informational purposes only and does not constitute financial, investment, or legal advice.

The trajectory of the dollar will likely be defined by the balance between U.S. Fiscal discipline and the growth of alternative financial infrastructures. The next critical checkpoint for observers will be the continued integration of digital currencies and the official reporting of foreign exchange reserves in the IMF’s upcoming quarterly updates, which will reveal whether the trend toward diversification is accelerating or remains a secondary ripple in a dollar-dominated sea.

Do you think the world is moving toward a multipolar currency system, or is the dollar’s lead insurmountable? Share your thoughts in the comments below.