For the better part of two years, the prevailing wisdom among economists was that a recession was not just likely, but inevitable. The playbook was simple: when the Federal Reserve raises interest rates aggressively to kill inflation, the economy slows down, unemployment rises and growth stalls. It is the economic equivalent of gravity.

Yet, the United States has spent the last several quarters defying that gravity. Despite the most rapid tightening cycle in decades, US economic resilience has remained remarkably stubborn, characterized by a labor market that refuses to crack and consumer spending that continues to drive growth.

This divergence from historical patterns has left policymakers and market analysts questioning whether the old rules of monetary policy still apply, or if a unique cocktail of pandemic-era distortions and new industrial strategies has fundamentally altered the American economic landscape.

The interest rate paradox

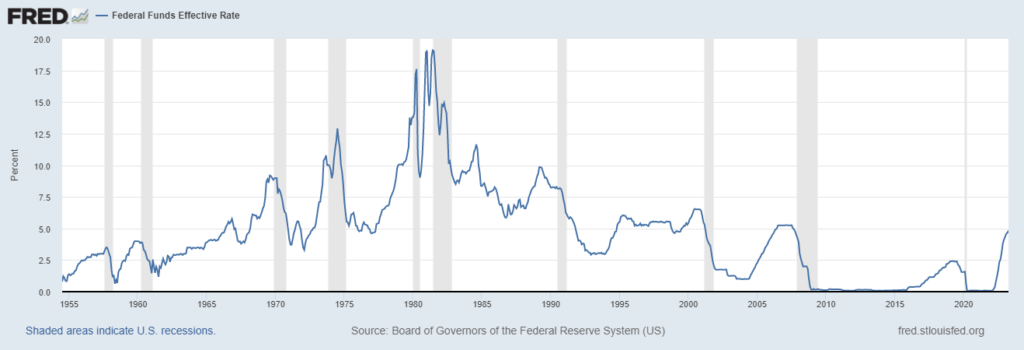

Traditionally, the Federal Reserve uses the federal funds rate as a blunt instrument to cool an overheating economy. By making borrowing more expensive for businesses and consumers, the Fed intentionally slows investment and spending to bring inflation back down to its 2% target.

Beginning in 2022, the Fed embarked on one of the most aggressive hiking cycles in history. Under Chair Jerome Powell, rates were pushed from near zero to over 5% in a remarkably short window. According to standard economic models, this should have triggered a “hard landing”—a sharp contraction in GDP and a spike in unemployment.

Instead, the economy has leaned toward a “soft landing,” a rare scenario where inflation falls without triggering a major crisis. This resilience is partly due to the “wealth effect”; while borrowing costs rose, many households saw their home values and stock portfolios hit record highs, cushioning the blow of higher mortgage and credit card rates.

The engines of unexpected growth

The primary driver of this defiance has been the labor market. Unlike previous cycles where rate hikes led to immediate mass layoffs, the post-pandemic era has been defined by a chronic shortage of workers. This “tight” labor market has given employees more leverage, leading to wage growth that has kept pace with, or even exceeded, inflation for many sectors.

This income support has fueled a relentless appetite for consumer spending. Americans have transitioned from spending on goods (like electronics and furniture during lockdowns) to spending on services, such as travel and dining. According to data from the Bureau of Labor Statistics, employment levels have remained robust, preventing the typical downward spiral of lower spending leading to more layoffs.

Beyond the consumer, a new era of fiscal policy has provided a structural floor for the economy. The US government has shifted away from purely monetary management toward active industrial policy. Massive investments via the Inflation Reduction Act and the CHIPS and Science Act have funneled billions into domestic manufacturing and green energy, creating a surge in private sector investment that offsets the cost of higher interest rates.

Predicted vs. Actual Economic Trends

| Indicator | Common Prediction | Observed Reality |

|---|---|---|

| GDP Growth | Negative/Contraction | Consistent Positive Growth |

| Unemployment | Sharp Increase (5%+) | Historically Low Levels |

| Inflation | Sticky/Persistent | Steady Decline Toward Target |

| Consumer Spend | Significant Pullback | Resilient/High Volume |

The risks of a “higher for longer” regime

While the current trajectory is positive, it is not without fragility. The primary concern for analysts is the “last mile” of inflation—the idea that bringing inflation down from 9% to 4% was easy, but getting it from 4% to 2% may require a level of pain that the economy cannot sustain.

the cost of servicing government debt has risen sharply. As the US Treasury rolls over old debt at newer, higher interest rates, a larger portion of the federal budget is diverted toward interest payments rather than productive investment. This creates a long-term fiscal tension that could eventually limit the government’s ability to stimulate the economy during a future downturn.

There is likewise the question of the “lag effect.” Monetary policy often takes 12 to 18 months to fully filter through the economy. Some economists argue that the full impact of the Fed’s hikes has not yet hit the most vulnerable sectors, such as small businesses and commercial real estate, which are more sensitive to floating rate loans.

Disclaimer: This article is for informational purposes only and does not constitute financial, investment, or legal advice.

The next critical checkpoint for the US economy will be the upcoming series of Federal Open Market Committee (FOMC) meetings and the release of the next Consumer Price Index (CPI) report. These will determine whether the Fed feels confident enough to start cutting rates or if they will maintain the current restrictive stance to ensure inflation is fully extinguished.

We want to hear from you. Do you feel the resilience of the economy in your daily spending, or are the higher rates finally starting to bite? Share your thoughts in the comments below.