For many American households, the arrival of a tax refund check serves as a yearly catalyst for financial housekeeping. It’s a windfall that often finds its way into high-yield savings vehicles, specifically promotional certificates of deposit (CDs) that lure savers with “teaser” rates significantly higher than the national average.

However, as the interest rate environment shifts, some savers are questioning if their loyalty to these bank promotions is still the smartest move. Specifically, the question of switching from promotional CDs to Treasury bills has gained traction among those looking for a blend of safety, liquidity, and tax efficiency.

The transition can feel daunting for those who have spent years dealing exclusively with local banks or online savings accounts. The terminology—par value, discount rates, and maturity dates—can make government securities feel like the exclusive domain of Wall Street traders, but the reality is far more accessible for the average taxpayer.

The Trade-off: Promotional CDs vs. Treasury Bills

Promotional CDs are designed as customer acquisition tools. Banks offer a high rate for a short window—often 6 to 13 months—to gain new deposits on their books. The catch is usually twofold: the rate is temporary, and the money is locked away. If you necessitate your tax refund back before the term ends, you typically face an early withdrawal penalty that can eat into your principal.

Treasury bills, or T-bills, operate differently. These are short-term debt obligations backed by the full faith and credit of the U.S. Government. Unlike a CD, where you earn interest periodically, T-bills are sold at a discount. For example, you might pay $950 for a bill with a face value of $1,000; the $50 difference is your “interest” paid at maturity.

For those who have “no experience with Treasurys,” the primary hurdle is often the interface. Even as CDs can be opened with a few clicks in a banking app, T-bills are typically purchased through TreasuryDirect, the official government portal, or through a brokerage account. While the government website is functional, it lacks the polished user experience of modern fintech apps, which often intimidates new users.

The ‘Hidden’ Advantage: Tax Treatment

When comparing a 5% promotional CD to a 5% T-bill, the numbers appear identical on paper. However, the after-tax return tells a different story. This is where the switch to Treasurys often becomes a mathematical win for the saver.

Interest earned on CDs is taxable at both the federal and state levels. In contrast, interest from U.S. Treasury securities is exempt from state and local income taxes. For a resident of a high-tax state like New York or California, this exemption can effectively boost the real yield of a Treasury bill by a significant margin compared to a bank CD.

This tax advantage makes Treasurys particularly attractive for those using a tax refund—money that has already been processed through the federal system—to build a liquid emergency fund or a short-term savings bucket.

Comparing the Two Vehicles

| Feature | Promotional CD | Treasury Bill (T-Bill) |

|---|---|---|

| Risk Level | FDIC Insured (up to $250k) | Backed by U.S. Government |

| State Taxes | Taxable | Exempt |

| Liquidity | Penalty for early exit | Sellable on secondary market |

| Entry Point | Bank/Credit Union | TreasuryDirect or Brokerage |

Is Now a Bad Time to Switch?

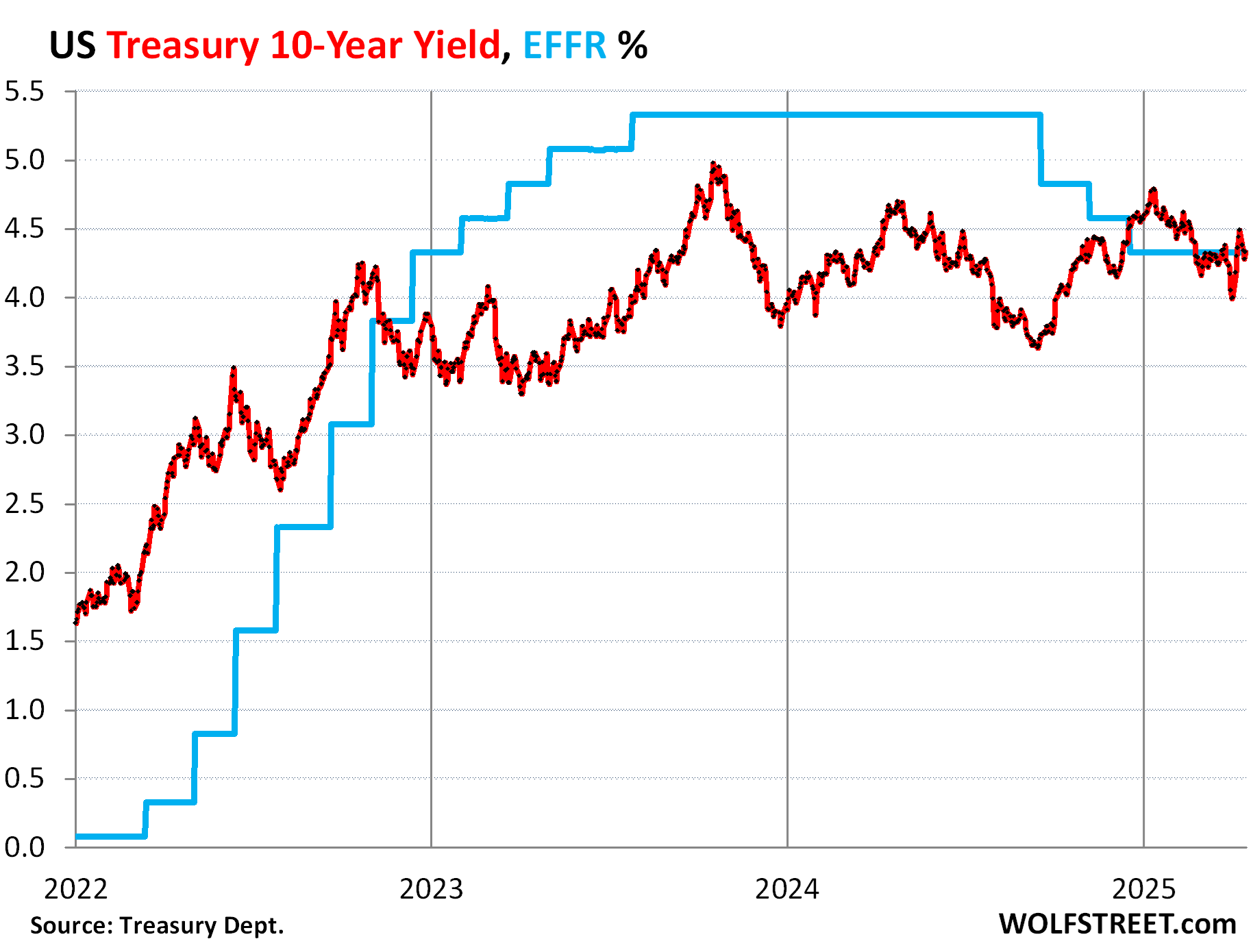

The timing of a switch depends largely on the trajectory of the Federal Reserve’s monetary policy. When the Fed raises rates, new T-bills offer higher yields. When the Fed cuts rates, those who “locked in” a high rate via a CD are protected until the CD matures.

If you currently hold a promotional CD with a rate that is significantly higher than current T-bill yields, it generally does not make sense to pay an early withdrawal penalty to switch. The penalty often outweighs the tax benefits of the Treasury. However, for new money—such as a fresh tax refund—the T-bill is often the more flexible and tax-efficient choice.

T-bills offer superior liquidity. If an emergency arises, a Treasury bill can be sold on the secondary market through a broker. A promotional CD, conversely, is a rigid contract; you either wait for the maturity date or pay the bank for the privilege of taking your own money back early.

Navigating the Learning Curve

Moving into government securities does not require a degree in finance. For the beginner, there are two primary paths:

- The Direct Path: Opening an account at TreasuryDirect. This allows for “automatic reinvestment,” where the government automatically buys a new bill for you when the old one matures, keeping your money working without manual intervention.

- The Brokerage Path: Using a firm like Fidelity, Schwab, or Vanguard. This is often the preferred route for those who want their T-bills to appear alongside their stocks and mutual funds in a single dashboard.

The transition is less about “timing the market” and more about optimizing the structure of your savings. By moving away from the “teaser” cycle of promotional CDs, savers can avoid the constant search for the next high-rate bank and instead rely on a stable, tax-advantaged foundation.

Disclaimer: This article is for informational purposes only and does not constitute financial, legal, or tax advice. Readers should consult with a certified financial planner or tax professional regarding their individual circumstances.

The next major indicator for those weighing this decision will be the Federal Open Market Committee’s (FOMC) upcoming scheduled meetings, where updates on the federal funds rate will directly influence the yields of new T-bill issuances.

Do you prefer the simplicity of a bank CD or the tax perks of Treasurys? Share your experience in the comments or share this guide with a fellow saver.