The near future of the entrepreneurship and construction industry in Israel does not look good. The real estate industry in Israel has a number of structural problems followed by waves of mania and depression, which are reflected in price increases and decreases that cannot be expected. If 14 years ago we felt the difficult start of the industry, in the two years between the first corona closure and the middle of last year we felt the strong acceleration, while Recently the market experienced a long slowdown.

● The Settlements Act has undergone a haircut: what is left out and who benefits? | Globes test

● The price of an average new apartment was cut by NIS 80,000. And this is just the beginning Interpretation

● Prepare for an increase in interest rates: prices are at a 14-year high. All causes and consequences

In an attempt to put our finger on the structural problems of the industry, we dived into the recently published data and analyzed the activity in the market over the last two decades.

Double-Take: The market is cumbersome and reacts slowly to changes

The real estate market is often expected to behave similarly to the capital market. This is a mistake that is repeated every time it seems that the real estate industry is facing a change that the capital market would react to within days, or hours. But the real estate market is not a capital market: it is cumbersome, loaded with financing constraints, planning, laws, inputs and construction methods, personnel, and more, and there is almost no situation or possibility that it will be able to respond in time to a change that is excited about it.

The best example is the events in the Israeli real estate market in the first decade of the 2000s. The first two thirds of that decade passed over the residential real estate sector as a long crisis of price declines, which resulted in a significant decrease in the number of annual construction starts, and dormancy and stagnation in regards to initiation and project planning, and land marketing by Rami, which at the same time encountered a lack of response even to the tenders it issued.

In 2008 the trend reversed andApartment prices began to rise. However, three more years passed before the construction industry began to respond with an increase in construction starts, during which apartment prices rose by more than 50%. In fact, it was only in the second half of the previous decade that the rate of construction began to meet the price increases.

Today, analyzing the situation and the market backwards, it is already clear that a very significant part of those price increases was caused by the late awakening of the construction industry.

Acceleration too strong: The market is racing and cannot stop in time

What happened in the real estate market from the last quarter of 2020 until the end of 2022 cannot be rationally explained. During this period, apartment prices increased by approximately 33% and demand soared. In 2021, over 150,000 apartments were purchased, approximately 25% more than in The previous record, 2015.

However, back in 2015 it was possible to explain the peak in pent-up demand that erupted following the repeal of the “zero VAT” law, and the desire to bring forward the taxation of then Finance Minister Moshe Kahlon on investors, in 2021 the reason was completely different.

In this year, demands erupted for the government’s housing policy, which was expressed in complete stagnation due to the chain of election campaigns that landed on the country between 2019 and recently, in which governments did not last, did not formulate a new housing policy, and did not show the public any perspective.

The planning and construction industry at that time was already ready and operating in full force. The number of construction starts has reached double dimensions and more than those recorded in the “great slumber” of the beginning of the 2000s, and the developers have invested more and more in land and construction, in order to advance the large demand.

However, while the construction industry operated vigorously, the economic data changed and with them also the demand, construction costs and financing costs.

Having trouble braking: The signs of the crisis were already visible in 2021

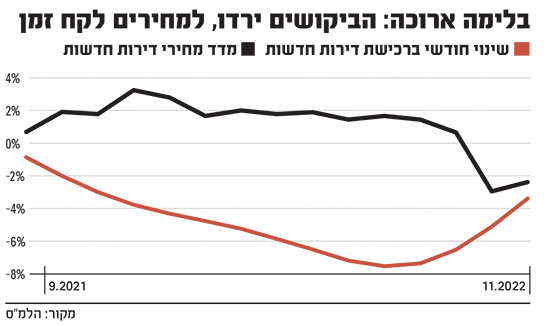

Apparently, the real estate developers had enough time to prepare for a difficult day: one of the surprising figures recently published by the Central Bureau of Statistics is that the stalling trend in the sale of new apartments began as early as September 2021. That is, on paper, a developer could examine the changes and behave differently. It didn’t happen, and for good reason: apartment prices continued to rise at a dizzying pace, and after all, no developer would stop construction in a situation where prices are rising.

This is how 2022 began with price increases that continued the momentum of 2021, while at the same time a strange economic situation arose: the public decreased demand for new apartments every month, but the price index of new apartments sold on the free market (that is, minus the price for the resident) continued to rise.

The month of April has arrived. The decline in the rate of sales of new apartments intensified, but those who purchased apartments were willing to pay more, and the index continued to rise. In July-August 2022, the rate of decline in sales reached a peak, but only in October did the price index for new apartments in the free market show a decrease. Where in the capital market can you see a price reaction that lags so far behind the market data?

The result: those who previously enjoyed the first two features of late ignition and strong acceleration – may pay the price because they did not brake in time. And the price can be expensive.

The big question: Is the construction industry on the way to an accident?

A crisis in the real estate market comes in 3 stages: the first, a significant decrease in demand and the number of transactions; the second, a few months later, an increase in sales by developers and then a real drop in apartment prices; the third – an overall price drop, which is also reflected in the Yad apartment market Second, this is the toughest market in this respect.

At the moment the real estate market in Israel is in its second phase. It is only a matter of time, not long, until the apartment owners will also internalize the new situation they have found themselves in.

The apartment price indices published recently indicated a price drop of 4.3% in the price index of new apartments sold on the free market – all within just two months. Translated into money, this is a drop of more than NIS 80,000 on average, which is quite a bit.

The CBS reports that developers currently own more than 53,000 unsold apartments. In a very conservative estimate, this is an inventory worth NIS 80 billion, which is mainly financed through bank financing that is becoming more and more expensive. On the other hand, financing is also becoming more expensive for the apartment buyers, who are keeping their feet off the market.

In order to benefit from lower prices, the developers initially tried the technical specification promotions, meaning adding accessories to the apartment, such as an improved kitchen, air conditioning and vouchers for the purchase of bathroom accessories. However, such promotions are suitable only for a certain part of the population, and a significant part of the potential buyers were rejected by the banks for mortgages, or were put off by the amount of the loans and the monthly repayments. So kitchen cabinets could not answer them.

In the next step, price reduction began. Data published by the Chief Economist at the Treasury and the Central Bank show that even after these price reductions buyers have not yet returned to the market, indicating that the declines are far from over. If interest rates in the economy continue to rise, as expected, the declines will also be greater.

In such situations, what will determine is the quality of management of the real estate companies. Leveraged companies that have a large inventory of unsold apartments may find themselves in an unpleasant situation. As I recall, in the late nineties and early 2000s, companies were unable to survive the industry recession that occurred at the time, after the great boom of the The Great Ascension.

In those days, one of the leading lawyers in the field of consolidation and liquidation boasted that he was the manager of the leading real estate company in Israel – by virtue of his position as a special manager of quite a few failed companies. Do we hear similar sentences now, 20 years later?