The buyers of 2022 turned to look for apartments in the peripheral areas, mainly in the south, and this is because the prices are relatively low there. The result – the weight of transactions in the demand areas of the center and Tel Aviv decreased compared to 2021, according to the data of the Central Bureau of Statistics (CBS) published for the last quarter of 2022. It can also be learned that more buyers preferred to purchase small apartments compared to previous years, apparently to deal with rising housing prices.

● This week in real estate: why developers are afraid of land parcels on the coast of Haifa

● The foreign passport is moving away: Portugal has put an end to the “golden visa” program

The real estate market is in a kind of dissonance: on the one hand, apartment prices are at an all-time high. An average apartment purchased in the last quarter of 2022 reached an average price of NIS 1.96 million, and the average price of a 4-room apartment in Israel reached NIS 1.97 million. On the other hand, the atmosphere Public RegA is that this is a record, from which the decline will be steep – something that is reflected in the paucity of transactions and a significant drop in the prices of new apartments.

The dissonance: demand is falling but the price continues to rise

A review of the average apartment prices recorded in the various cities reveals that, despite the parameters that indicate a major slowdown in the sector, the prices of apartments purchased in the last quarter of 2022 were higher than those purchased in the previous quarters, when the crisis atmosphere was less.

This can be explained by two reasons: the first – the crisis that is often talked about is manifested at this stage mainly in the decrease in the volume of transactions. This is only one component of a crisis. The second component is price drops – and this is not happening yet. Although there was a significant decrease of 4.3% in the last two months in the index of the prices of new apartments purchased on the free market (this is an unofficial index, which is based on the CBS data, which, unlike the official index, does not include apartments purchased at subsidized prices), but the overall index continues to rise – although by a few tenths of a percent. This indicates that the second-hand apartment market, which makes up about three quarters of the entire market, is still registering increases.

The second reason is the mix of buyers. Analyzes conducted by the Bank of Israel on the mix show that the interest rate hikes in the last few months drove away from the market mainly buyers of apartments at prices of NIS 1-3 million, and less so the buyers of apartments at higher prices. The buyers of the expensive apartments are more affluent, and can better afford their mortgage repayments even when interest rates rise. Another evidence for this explanation can be found in the data showing that the prices of apartments purchased lately are higher than before. The reason for this is apparently not the price increases, but the weight of the more expensive apartments – which has increased.

How can you determine that a market is reaching a crisis | Eric Mirovsky, Commentary

In many articles, including those that appeared in “Globes”, the situation in the residential real estate market has already been defined as a crisis, referring to factors such as a large decrease in the number of apartments being purchased and a decrease in the amount of mortgages being taken out.

But can we already say that the market is in crisis?

How do you define a crisis? There are several definitions, and we prefer the definition according to which a crisis in the housing market includes three components: a drop in demand, a drop in prices and a drop in construction starts. A situation where prices fall, but demand rises (in a situation where, for example, the supply of apartments far exceeds the increase in demand) – does not have to be a crisis. A situation where demand falls but not prices may reflect a situation where the supply is very low, and therefore even here it is not enough to define a “crisis”. A decrease in construction starts is a problem that may be a significant part of a crisis, but cannot alone define a situation as a crisis.

Today the market is in a situation where the demand has decreased to a large extent – but not the prices, therefore, in our view the market is not yet in crisis. In fact, since the beginning of the tsunami of price increases, which began in 2007, the market has faced “almost crisis” situations twice, which in the end turned out to be temporary obstacles: the first time was in 2011, when interest rates were on the rise and the social protest led to a large drop in demand. For a few months, apartment prices even dropped slightly. In 2012, construction starts dropped, because the developers did believe that the market was sliding into a recession.

However, very quickly the situation returned to normal – the interest rate was lowered, the failure of the protest led to the return of demand to the market, and the prices began to rise.

In 2017-2018, the feeling was that “price for the tenant” was going to be successful. Demands stopped due to expectations, and here too prices fell. However, starting in 2019, the situation turned around, prices began to rise, and the rest is history.

In both of these cases, the signs of the crisis were more mature than those the market is currently experiencing. In other words, both the demand and the prices went down, and in 2012 construction also started – however, the crisis did not last long, and had almost no effect.

Today, as mentioned, the apartment price index is still on the rise, and only in the last two months has there been a noticeable decrease in the price index of new apartments sold on the free market (an unofficial index, which is based on the Central Bank’s new apartment price index, excluding apartments sold as part of a price to settle). Construction is still at a high level Very much so the situation is not a crisis.

However, what does strengthen the assessment that this time the situation is different are the global crisis, the rising inflation, signs of a recession and unemployment and the increase in interest rates in unusual dimensions for the last decade. These are powerful data, which the market cannot remain indifferent to, unless they change. Therefore, even if the crisis has not yet hit the industry – the data shows that it should come, and soon.

The change in the mix of apartment purchases

How does the public deal with price increases? The CBS data shows that the annual increase in apartment prices stands at 17.1%. The interest rate increases, as we have shown, drove away even more buyers who wanted to purchase relatively cheap apartments. But a closer examination shows that there has also been a change in the geographic mix of purchases: a large increase in purchases in the periphery the south and the north, and a significant decrease in purchases in the demand areas.

In 2021, about 18% of apartment purchases were made in the Tel Aviv district, while in 2022 the number dropped to about 14%; In the Central District, about 26% of the apartments were purchased in 2021, while last year the figure dropped to about 24%; In the Haifa district, the weight of purchases decreased from 16.6% to 16%. On the other hand, it increased in the north from 10.2% to 11.6%, and the most significant increase was recorded in the south – by more than 4 percentage points to almost 23%. An increase of about half a percentage point to about 9% was also recorded in the Jerusalem district. In this case it must be assumed that the multiple transactions in the city of Beit Shemesh contributed to this increase. The survey by the chief economist at the Treasury shows that Beer Sheva serves as a refuge for many young couples, due to the relatively cheap prices there.

Another matter we examined is the extent to which the changes in apartment prices led buyers to compromise on the size of the apartments. We divided the mix of apartments into 4-room apartments, smaller than 4-room apartments, and larger apartments. It turned out that between 2021 and 2022 the differences were very small, and probably meaningless. On the other hand, a comparison with 2017 showed that the weight of small apartments in public purchases increased from about 34% to about 36%, the weight of large apartments recorded a slight decrease but remained around 28%, while 4-room apartments reached a weight of 36% in 2022 compared to 38% in 2017.

Our assessment is that the small changes that took place between 2021 and 2022 are due, among other things, to the increase recorded in purchases in the periphery, where buyers could find for themselves at reasonable prices larger apartments than they could purchase in the center of the country.

Tel Aviv continues to increase the gap

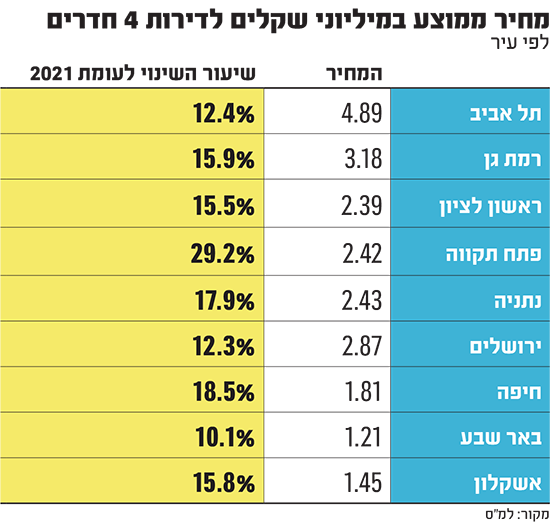

This is the place to examine the average 4-room apartment prices recorded in the last quarter of 2022. In Tel Aviv, the most expensive city, they reached NIS 4.9 million, compared to the cheapest city in Beer Sheva, where they reached NIS 1.2 million. In recent years, apartment prices in Tel Aviv have not only broken every possible record – the ratio between them and apartment prices elsewhere has risen considerably. For example, the ratio between the price of a 4-room apartment in Tel Aviv and that in Be’er Sheva reached 4 times at the end of 2022, while in 2017 it was 3 times greater; Regarding the ratio for 4-room apartments in Haifa, it increased from 2.4 to 2.7, and relative to 4-room apartments in Jerusalem, it increased moderately from 1.6 times to 1.7.

This of course largely explains the shrinking of the Tel Aviv market. It turns out that even relative to its neighbors – Ramat Gan, Rishon Lezion, Petah Tikva and Holon – Tel Aviv has increased the price ratio in the last five years.