The beverage market in Israel has undergone upheavals in the last two years Quite a few, against the background of the outbreak of the corona plague that affected the manufacturers’ sales mix. From the beginning of the current year, a new tax imposed by the government on sugary drinks has been added to them, the effect of which is not yet fully known, but it is expected to hurt their results.

Against this background, an interesting and surprising move by a company was launched at the beginning of the week Clal Industries and Beverages A minority shareholder in the soft drink company Yafora: Merger with the Carmel Winery Company, which is controlled by the Kedma Private Equity Fund.

All Beverages, whose shares are currently held mainly by institutional entities, has one single asset prior to the planned merger – 30% of the shares of Yafora, one of the three largest soft drink manufacturers in Israel.

As part of the merger with Carmel Wineries (which currently includes 78% of the winery’s shares), the name of Clal Beverages will be renamed Carmel Wineries, after which it will operate the winery, which was founded 140 years ago, with the encouragement of Baron Edmund de Rothschild.

The merger is valued at NIS 840 million for the merged company, based on a valuation of NIS 505 million for all beverages – 34% higher than the market value at which it was traded before reporting.

Completion of the merger is expected to be effected through an exceptional allotment of shares, which will be effected by way of a non-uniform offer through a prospectus, and is therefore subject, inter alia, to the approval of the Securities Authority.

Accordingly, the current shareholders in Clal Beverages are expected to hold 60% of the merged company, and the value derived for the controlling shares in Carmel Winery (as stated, 78%) in the merger is NIS 336 million. Keren Kedma, the current shareholder, has undertaken that within a period of 36 months from the date of completion of the transaction, it will participate in capital raising carried out by the merged company for the purpose of executing transactions in the food and beverage sector, in an amount not less than NIS 300 million. At the same time, the merged company intends to consider issuing rights to all its shareholders.

Came to the stock market following a dispute

Clal Beverages was previously controlled by Clal Industries of Len Belvatnik, and came to the stock exchange about four years ago following a dispute over its holding in the soft drink manufacturer Yafora (30%), which Belvatnik sought to realize. Clal Industries later sold most of its shares in general drinks to institutional entities.

The controlling owner of Bifora, the underlying asset of Clal Beverages, is a company refrigeration Of Roni Gat and Shlomo Rodev (who owns 70% of the shares), who previously clashed with Clal Industries over the latter’s desire to realize the minority holdings in its hands. Last November, Karor offered to buy Clal Bifora’s holding at a value of NIS 450 million – an offer that was rejected despite reflecting a premium on the market price of Clal Beverages (which stood at NIS 375 million at the beginning of the week).

Yafora factory in Rehovot / Photo: Eyal Fischer

Clal Beverages operates without a controlling interest, and is actually held by five institutional entities: the Altshuler investment houses Shaham and Willin Lapidot and the insurance companies Harel, Clal and Phoenix. Institutionalists have an aggregate holding of 65% in all beverages, and in addition the old landlady, Clal Industries, holds a 14% share in the company.

Yafora began its career as a juicer in 1933, when it produced orange juice (Paz juice), and today it also produces soft drinks such as soda whips, Spring, RC Cola brand and the Ein Gedi mineral water brands and Mei Eden.

Yafora’s financial data, as revealed in its financial statements for 2021, show why Refrigeration was willing to pay a handsome premium last year for the minority shares in the company. The company recorded a sharp jump in its business performance last year, after 2020, which was a successful year for it as well.

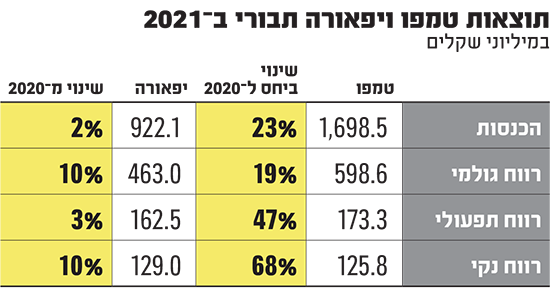

Although Yafora’s revenues rose by only 2% last year to NIS 922 million, its gross profit margin increased by 46% to 50%, a figure that many manufacturing companies can envy. Operating profit maintained a similar rate, at 18%, and stood at NIS 162 million, while net profit climbed by 20% in 2021 to NIS 129 million.

Tempo suffered from the corona more than Mifora

Along with Yafora, which is held by two listed companies (refrigerated and including beverages), another player in the beverage world, whose activities are revealed through the capital market, is Tempo, a bond company controlled by Jacques Barr (60%) and the beer company The Dutch company Heineken (40%) produces and markets alcoholic beverages, including Goldstar and Maccabi beers, along with soft drinks such as Pepsi, the XL energy brand and mineral water, and also owns wine, through Barkan Wineries.

Tempo suffered more from the Corona crisis, and its sales weakened in 2020, mainly due to the crisis that befell the “cold market”, ie supplies to the institutional sector, which includes pubs, hotels, restaurants, etc., whose activities were shut down for extended periods during the epidemic. Hot (which is sales to retail chains).

In 2021, with the country exiting the closures in the first quarter, Tempo recorded a significant recovery. It concluded the past year with a 23% jump in revenue, to NIS 1.7 billion. The gross profit margin was 35%, and the operating profit was 10%. The net profit increased by almost 70% compared to 2020, to about NIS 126 million.

Tempo recently announced that controlling shareholder Jacques Barr will vacate the CEO chair after 14 years in the position, and his son Daniel will be appointed to the position. Bar Sr. remains in the position of Tempo chairman.

Tempo: “The tax will have a material adverse effect”

The soft drink market in Israel is mainly divided between three main competitors. The largest is the Wertheim family’s main beverage company, which is known to the public as a Coca-Cola manufacturer, which according to Sterncast data controls about 40% of the market. Yafora holds 38%, and Tempo holds about 16%. Together, the three dominate about 95% of the market.

It seems that the industry is currently facing a crossroads. The government last year imposed a tax on sugary drinks, the sugar tax, which came in from the beginning of 2022. Its implications for the soft drinks sector have not yet been revealed in the financial statements for the past year, but in the companies companies warn of adverse effects that will materially hurt them. For example, Tempo announced during the tax levy last year that it “is likely to have a material adverse effect on the company’s sales and the results of its operations.”

However, it is not inconceivable that the institutional bodies and holders of beverages in general saw this as a stimulating factor for the expansion of activity and a merger with activity in the wine industry of Carmel Wineries, an industry that was not affected by the taxation moves. The business activity of Carmel Wineries has not yet been revealed, but an analysis of profitability by Tempo’s operating segments in 2021 can teach what Clal drinks finds in the emerging merger.

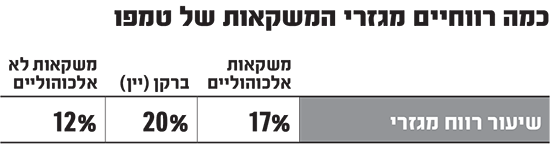

Tempo has three sectors of activity: non-alcoholic beverages, alcoholic beverages and wine (Barkan Wineries). The segment results, which are the gross profit less selling and marketing expenses, show that the highest segment profitability rate – 20% – was achieved in the wine sector. It is followed by the area of alcoholic beverages, which generated a 17% profitability for Tempo; And finally there is the profitability from the non-alcoholic beverages sector, which stood at only 12%.

Carmel Winery, Rishon Lezion / Photo: Tamar Mitzpi

Carmel Winery is one of the leading bodies in the field of wine in Israel. Sterncast data attached to Tempo reports show that in the barcoded wine bottles market, ie the bottles sold in retail chains and liquor stores, Carmel Winery is the largest company with 23.6% of the market, while Barkan (Tempo) wineries have a market share of 24.3%.

The entry of Carmel Wineries into the stock exchange, through Clal Beverages, will allow investors in the share to be exposed to a winery with a significant foothold in its field of activity, and it intends to expand to other fields as well. The merging companies stated that they intend to examine industry-wide business collaborations in the food and beverage market in Israel, with the aim that the merged company will be a significant body in this market.