The Minister of Finance is currently declaring that work on the Arrangements Law for the years 2023-2024 is in progress, and he has even decided to bring forward the approval of the next state budget, from the beginning of November to the end of September. Now in the current political situation, after the resignation of Idit Silman from the coalition, it is very doubtful whether this will really happen.

One of the questions that is always on the table when preparing a budget is where the money will come from. One of the answers that comes up every few years is to apply an inheritance tax or estate tax on “extra-large” inheritances, or to call a child by his name: a tax on the inheritances of the rich.

This is one of the most controversial taxes, and it has been coming off the negotiating table time and time again over the last decade at the same rate at which it is rising. But the economic benefit of this tax and the expected revenue to the state from it have never been examined in Israel. Now, ahead of the formulation of the next budget and at the request of MK David Amsalem of the Likud party in the opposition, the Department of Budgetary Supervision at the Knesset Research and Information Institute has conducted research on exactly this question.

MK David Amsalem / Photo: Knesset Spokeswoman, Danny Shem Tov

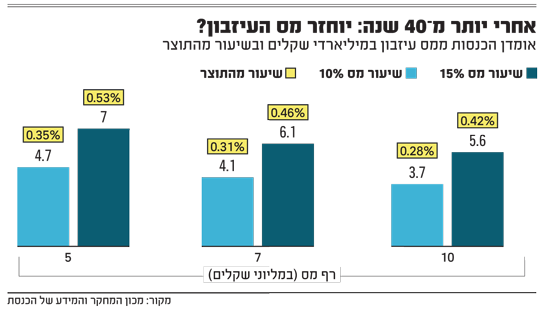

Estimation of state income from estate tax

The study shows that if inheritance tax is applied in Israel, it is expected to generate revenues of between NIS 5 billion and NIS 7 billion a year. Estate tax at a rate of 10% at a threshold of NIS 5 million is expected to yield an annual income of NIS 4.7 billion, and at a threshold of NIS 10 million is expected to yield an annual income of NIS 3.7 billion. Estate tax at a rate of 15% at a threshold of NIS 5 million is expected to generate annual revenues of NIS 7 billion, and at a threshold of NIS 10 million, is expected to generate revenues of NIS 5.6 billion.

A study by the Knesset Research Center focused on claims that revenue from these taxes would not be high, and this claim appears to have been refuted, assuming the tax would be higher than 10% and imposed on very large inheritances.

In Israel, inheritance tax was applied in the years 1981-1949 on the assets that the deceased bequeathed, including those he transferred to another person five years before his death, but in 1981 it was abolished. The tax repeal bill reads: “Over the years the law has been enacted it has become clear that the tax burden is borne mainly by heirs of small estates, while property owners of great value evade paying the tax by transferring their property to their ‘heirs’ while alive. This fact not only causes injustice “In dividing the tax burden, but the income from the tax is also small, so they are not worth the expenses for collecting it.”

Supporters, opponents and interests

Proponents of inheritance tax or inheritance tax argue that this is a tool for reducing inequality in the distribution of income and capital, and especially reducing the transmission of inequality from generation to generation. It has also been argued in favor of inheritance tax that it is a tax with a high level of progressiveness, especially in Israel, where social disparities are among the highest in developed countries. In addition, it has been argued that this is a fiscal tool for increasing state revenues, especially at a time when it is necessary to increase revenues in order to meet the deficit targets.

On the other hand, according to those who oppose the tax, the imposition of the tax may lead to a policy of a general reporting obligation, which does not currently exist in Israel, increase the friction between the taxpayers and the tax authority and lead to an increase in collection. These, argue opponents of inheritance tax, may make the tax economically unviable. Another argument raised against the estate tax and gift tax was that they might increase tax planning and litigation and as a result, incomes would be relatively low, and most of the burden might fall on the middle class or heirs of a person who died suddenly and failed to make tax planning. It is also argued that the tax may offset income from other taxes, such as capital gains taxation, and a host of other claims.

In between there are also unknown political interests, with capitalists pressuring their people in the Knesset to take this debate off the table.

According to MK David Amsalem, who initiated the study, “Inheritance and estate tax is an important, just, egalitarian and social tax – a tax that is mandatory in a reformed society. A correct tax that will close some of the gaps between people in society and return capital to the state treasury, which will serve everyone. The intention is to apply it only to people who have accumulated a fortune of over NIS 50 million – not to a person who left an apartment or two to his children. The graded mechanism is still being examined, after which a complete bill on the subject will be drafted and formulated. “Nothing will happen if the very rich are a little less rich, and inequality and economic disparities in society are reduced.”

Inheritances of the top decile: NIS 53 billion

The study noted that in 2020 global wealth continued to grow, despite the turmoil in the economy following the corona crisis. According to Credit Suisse’s Wealth Report, in 2020 world wealth grew by 7.4% to $ 418.3 trillion compared to 2019. The top decile holds about 52% of revenues and about 76% of the world’s capital and deciles 1 to 5 hold about 8.5% of revenues and about 2% of capital. In Israel in 2018, the share of income of the tenth decile out of the total household income was 23.3% and of the two highest deciles 38.2%. The share of the tenth decile in total household income from capital was 59.7%, and of the two highest deciles 72.2%.

According to an estimate by the Research and Information Center of the capital income of an average household is NIS 2.5 million, and of a household in the top decile is NIS 11.5 million. The total inheritance of households is estimated at NIS 117.8 billion and in the highest decile at NIS 53 billion.

The distribution of financial capital between deciles of households is based on the assessment of the financial capital of the public that may be inherited and on the assessment of the distribution of financial capital between deciles of households. According to the research and information center of the Knesset, the total capital held by households in Israel (excluding pension savings) is about NIS 6.6 trillion, about NIS 3.3 trillion in financial capital and about NIS 3.3 trillion in housing capital.

However, the report noted that life expectancy also affects inheritance, and will affect income from inheritance tax or estate, if it is decided to impose them. “In the last generation, there has been a steady increase in the life expectancy of Israeli citizens. Therefore, the elderly in Israel use more capital than they have accumulated during their lives in the years after retirement, and therefore it is possible that the inheritance of most households decreased in the last generation.”

The tax is accepted in most OECD countries

In 24 OECD countries there is currently an inheritance tax or inheritance tax, and in most of them there is also a gift tax, so that it will not be possible to circumvent the inheritance tax by giving a gift worth the entire inheritance to a family member. These countries include Japan (inheritance), Korea (inheritance), France (inheritance), USA (estate), United Kingdom (estate), Ireland (inheritance), Germany (inheritance), Finland (inheritance), Denmark (inheritance). Inheritance / Inheritance), Turkey (Inheritance) and Greece (Inheritance), Iceland (Inheritance), Italy (Inheritance) etc. The tax rate for heirs in close proximity averages 21% (in the 18 countries examined). The tax rate for other heirs ranges from 8% (Italy) to 75% (Japan), and the average is 36%. The average maximum tax threshold was about NIS 7.5 million.

In 12 countries (including Sweden, Russia, Hong Kong, Singapore, and even Israel) there is no inheritance tax or inheritance, ten of which have been abolished since the 1970s due to lack of political support, tax burden reduction and low tax collection. In 12 developed countries with a per capita GDP higher than Israel (where there is an estate tax), the share of inheritance tax or inheritance tax in 2020 was 0.25% of GDP, and therefore according to the OECD average, the tax revenue is about NIS 3.6 billion.