The largest retail chain in Israel, Shufersal, is at a crossroads, with the institutional bodies, which hold most of its shares, debating how to act in the face of the departure of veteran and esteemed CEO Itzik Aberkhan.

Last weekend, Aberhahn officially ended his position at the company, after about ten years in the position and about two months after the announcement of his expected retirement, which fell on the market by surprise. The person who will replace Aberkhan in the position will be the current CEO of the Israel Electric Corporation, Ofer Bloch, who is expected to take up his position in about a month. Until Bloch took office.

Itzik Aberhahn, outgoing CEO of Shufersal / Photo: Eyal Yitzhar

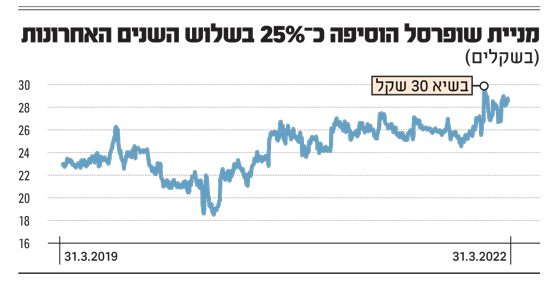

Shufersal It is currently traded at a value of about NIS 7.7 billion, after an 11% increase in the share since the beginning of the year – slightly below the peak level it reached last February. The chain has been operating for almost two years without a core of control, since Discount Investments, under Eduardo Elstein, sold its shares in the company.

Most of the company’s shares are currently held by six large institutional entities: Altshuler Shaham Investment House and the Migdal, Clal, Harel, Menora Mivtachim and Phoenix insurance groups. Each of these holds a share of about 10% of the company’s share capital, so that in total they all together hold about 60% of the company’s capital.

The institutional bodies at Shufersal were the ones that led about a year and a half ago to the election of Yaki and Damani, former CEO of Electra Consumer Products and experienced director in the retail field, to head the board. However, the relationship that has developed since , A centralized manager in his own right, is the one who led to the departure of the latter.

Various initiatives to purchase a share in Shufersal shares

Some of the institutional bodies invested in Shufersal express dissatisfaction with the direction in which the company is heading. These would have preferred to see a CEO with more distinct experience than Bloch in the retail field. Some of them want Abercahn to return to the position, in order to continue to grow the company in a format they have known in the past.

At the same time, initiatives began to emerge from various factors in the market to purchase a share in Shufersal shares. One of them even came to fruition last month, when brothers Yossi and Shlomi Amir, former owners of the Freshmarket food chain, submitted an offer to purchase a quarter of Shufersal shares. However, the two withdrew from their offer just two days later, due to their opposition to the move by energy company Paz (which recently sold the Freshmarket chain it controlled).

It should be emphasized that at Shufersal’s current market value, the acquisition of a share from the company will be an expensive move, which will require anyone who tries to take over the chain to provide equity of between NIS 500 and 700 million and take significant credit from the banks.

“Bring in an inexperienced CEO in the retail field”

“From our acquaintance with Vadmani, at the time of his appointment it seemed to us that this was a proper appointment, so we voted for him,” says a senior official in one of the institutional bodies that hold Shufersal shares. “In the end, in stark contrast to what happened at Paz, for example, where in-depth reforms were needed, and the institutionalists wanted to make a fundamental change – at Shufersal this was not the case.

“This is a company that is a market leader, with management leading over the years changes and innovations. We wanted to appoint someone who could give more push but preserve the existing one. In all the interviews we conducted with the candidates for chairman, it was important for us to understand that he did not change, Abercrombie. Although we did not want him to allow them to have full control of the company, we did want the quality management to remain in the company. ”

Yaki and Damani, Chairman of Shufersal / Photo: Yonatan Blum

With the departure of Aberkhan also came a wave of departures of other senior executives in the company. “What actually happened is that they fired the old management and brought in a new management. They brought in a CEO who is not at all experienced in the retail field. Bloch may be an excellent CEO (in the IEC and other bodies he managed, H. S.), but the starting point is that he has no experience in the retail field, which is 180 degrees from the intention we had as an institutional body. That Aberkhan will leave the company. “

A senior official in another institutional body, who is also a shareholder in Shufersal, says that “what we see in Shufersal is a recurring phenomenon in companies without a controlling interest. Mini Line, which is supposed to be made at a value of close to a billion shekels, was a deal that lit a bright red light for us and a very uncomfortable feeling about the way things are going.

“If there was a homeowner in Shufersal who ‘sweated’ to get where he was, I doubt he would have written the check of this size. It says something about Shufersal’s board of directors and the way it conducts itself. “There will be a choice of directors, and we may decide that it is not right to extend their tenure.”

Regarding the election of the CEO, the senior added that “I have nothing against Bloch, and I do not know him and his skills, but from my conversations in the retail sector it seemed that the appointment of Uri Kilstein (who as far as is known ran for the position) is more natural, and for some reason it did not happen.”

“Stock price reflects takeover attempt”

“Obviously the situation of Abercrombie’s departure was surprising,” says Lilach Gross, Rosario’s retail analyst consulting and research. “There was an expectation here that the replacement would come from the field, and that was a bit disappointing. Abercrombie was a highly regarded CEO and is considered the one who had his hand in everything. He knew every price and sign in a business from small to large. We are also seeing a wave of senior exits, which is increasing uncertainty. “

Gross adds that “the share price today reflects an attempt to take over (Shufersal, H. S.). According to the financial results, we would expect the price of the share to fall. When leaving the corona, it was clear that revenues would fall. “However, in 2020 they have risen more than the market, thanks to their online activity and logistics.”

A senior source in the capital market believes that the institutions are making “background noises”, but estimates that in the end, without a dominant shareholder in the company, they will align with the line led by the chairman and Damani and with the appointment of CEO Bloch. According to him, the institutionalists also understand that it is not worth committing another shock to the company, such as the replacement of the chairman of the board and the return of Aberkhan to the management of the network.

“Institutionalists appreciate what Abercrombie did at Shufersal, he brought results and finished the job. Shufersal’s board is strong and includes people who understand high-level retail. Shareholders understand that they can not afford another shock at the company after such a strong CEO finishes the job.” .

The same source adds that “the board has set up an independent committee, unanimously elected the person who runs the electricity company. True, this may not be the sexiest name, but even when Aberkhan took office, many asked where he came from. Bloch comes with a charge of running public companies “He did a glorious job. The capital market likes to ‘cry’, but in the end he understands that if God forbid the chairman of the board changes – it’s like entering the operating room while the doctors are working, and asking to replace the heart, kidneys and pancreas as well.”

Ofer Bloch, incoming CEO of Shufersal / Photo: Yossi Weiss

Shufersal last month concluded 2021 with a final quarter for that year that was weaker relative to its counterpart. Revenues decreased by 7% and amounted to NIS 3.6 billion, the gross profit margin remained stable at 27%. Operating profit in the last quarter was NIS 159 million, a decrease of 21% compared to the last quarter of the previous year; And the net profit amounted to NIS 100 million, a decrease of 17%.

The reasons for the decline in results concerned precisely the corona period at the same time last year, when the public was closed to homes and increased spending on food, also due to the lack of alternatives. Therefore, in the sum of 2021 as a whole, there was a decrease in revenues of 3% to NIS 14.7 billion, which resulted from the very exceptional year of the charge that preceded Shufersal and the retail sector in general. Sales per square meter were NIS 26.3 thousand, a decrease of 5.7% compared to the previous year but an increase of 6.1% compared to 2019.

“Possible scenario of Aberkhan entering the board”

And back to the issue of control of Shufersal. As mentioned, last month the Amir brothers withdrew, just two days later, from a move that could have led to their takeover of the largest food chain in Israel. Earlier, the two proposed that the chain allocate 24.9% of its shares to them, at a price that reflects a small premium of only 3% over the market price, and in exchange for NIS 2 billion, subject to a large dividend that Shufersal will distribute before the purchase. The proposal also included the appointment of seven directors at Shufersal on behalf of the brothers.

Last week, the car importer Carasso Motors, which is controlled by the Carasso family, confirmed that it was interested in making a substantial investment in Shufersal shares: “This examination is in preliminary and preliminary stages only … It should be noted that as of this immediate report, the company does not own Shufersal shares.”

According to the source in the capital market, “In the State of Israel, we have not yet learned the behavioral patterns of a company without a controlling shareholder. Some people will say that they always prefer a controlling shareholder, and I also prefer a situation where there is a landlord, as long as he is not a charlatan.”

The institutional factor also joins the assessment that a takeover is not a reasonable scenario: “Some want public companies to be run like in America, and it will take time to learn how to manage them. Today there are elements who want to take over Shufersal, “Positions regarding the provision of credit in this case, because of what happens with the interest rate. Therefore, in my opinion, this is not a realistic scenario.”

He said, “In Shufersal, the institutionalists have a holding that constitutes control without control, because we are not connected with each other. The way to build control can be like in the partnership mechanism in Paz, where the institutionalists manage their holdings together.

“The other option is for the institutional partnership to have an outside investor-manager like the Carasso family or another entity, and the institutionalists will sell some of their shares to the same partnership. But it’s hard for me to see them do that, that is transferring unrestricted shares to a fund where their shares will be blocked.”

According to the same institutional source, a scenario of Aberkhan entering Shufersal’s board with the support of any of the shareholders is possible, but in the current board structure it is not at all certain that he will be appointed chairman. If Aberhahn is nominated for election, he will run, but that does not mean he will be elected chairman. He may just remain a director.