The writer is a lawyer by education who deals with and is involved in technology. Manages an investment fund in cryptocurrencies, and lives in Silicon Valley. Author of the book “Brief A Money of History” and recorder of the podcast kanamerica.com

The real estate market in the United States does not only consist of households purchasing homes for their residence. Almost one-fifth of buyers today are investors. After the bubble burst in 2009, about six million homes were confiscated by banks for non-compliance with mortgage payments. To these were added, due to Fed policy, zero interest rates on mortgages and a sharp drop in yields on government bonds.

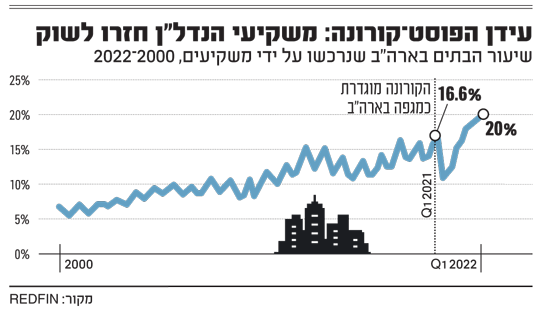

The combination of all these has made investing in homes particularly attractive for both institutional and private investors. The share of investors among homebuyers in America rose from about 6% in 2000 to a high of 18.4% in the last quarter of 2021, and to 20% in the first quarter of 2022 – according to a study by the real estate company “Redfin”. Investors not only bought The millions of homes confiscated by banks after the crisis also began to be invested in the construction and purchase of tens of thousands of housing units in areas of demand. In Atlanta, Georgia.

Since 93% of homes in America are purchased with the help of a mortgage, which covers the vast majority of the purchase price, the total monthly payment that borrowers or tenants can pay is the key to determining the price of the home. After the crisis in 2008, strict rules were set for mortgage issuers regarding the ratio between the monthly repayment and the wages of the borrowers. The rule by which mortgage lenders operate is known as the “28% Law” and means that a borrower is not allowed to spend more than 28% of his monthly income on home payments, including taxes, payments to the management company, and insurance. It is important to note in this context that in the United States there is an annual property tax of about 1.1% of the value of the home paid by the owner. Local taxes such as one-time public expenses approved by the voters may also be added to the tax.

Since the vast majority of Americans have debts other than their mortgage such as student loans ($ 1.61 trillion), credit card debt ($ 850 billion) and car debt ($ 1.47 trillion), the debt-to-income ratio is calculated in relation to the entire credit portfolio and debt of the borrower, and not just repayments. Her mortgage. Lenders want to see that the total monthly repayments of the borrower do not exceed 36% of the monthly income. Only 30% of loans with a debt ratio of 50% or more were approved, compared with 86% of loans with a ratio of less than 39%. A debt ratio of over 43% prevents the receipt of a federal guarantee for her mortgage so few lenders are willing to risk giving it up. For example, the criteria of the mortgage giant Freddie Mac state: “In general, the ratio of the monthly payment of debt to income shall not exceed 33% – 36% of the borrower’s fixed (gross) income.”

Ownership is more expensive than renting

On the real estate website “Zilo”, as well as at the various mortgage lenders, you can find a calculator that helps answer the question “What house can I buy?”.

We included the following data as an example: annual income of $ 80,000 which is the median household income in the US; $ 1,000 per month as payment for other debts such as car expenses, student loans and credit cards; and down payment in the amount of $ 80,000 – about 20,000 The average cost of the median home in America is above the average payment. We wanted to cover the balance of the cost with her 30-year mortgage, at the current interest rate of 5.8%. After taking into account the expected payment for property tax and home insurance Recommended) The calculator informed us that we can buy a house for $ 262,500 – barely two-thirds of the median house.

We tried to move to San Francisco, we upgraded our job to the city’s median salary, we increased the cash payment to $ 250,000 and our situation only got worse, now we could not afford even half the median house. We tried to upgrade our income, moved to the southern Silicon Valley, got a high-tech job, and managed to boost our annual household income to $ 450,000 (gross) – three times the district’s median household salary. We also increased the cash payment for the house to $ 500,000. Now the calculator tells us we can buy a house that costs about $ 2.165 million. A handsome sum by all accounts, but even now we have not reached the cost of the median house in the area.

Apartments For Rent In California, April / Photo: Associated Press, Eric Risberg

Although the purchase remained out of reach, another figure jumped out of the account. While the cost of interest on her mortgage alone was $ 1.665 million, about 77% of the property, and with the addition of property tax to about $ 9,600,000 a month, the rent was left somewhere behind. For example, the average rent for a three-bedroom house in an average town in the area (Sunnyville), barely reached half the interest rate and taxes – according to real estate sites Zamper and Zilo. This gap between “ownership premium” and rental prices is a clear indication of this That the price of the house is far from balanced with the value of the cash flow it produces.This is not a unique situation for Silicon Valley.

According to a survey conducted by consulting firm John Burns Consulting and published about a week ago, in most US the cost of ownership (i.e. the monthly repayment on a mortgage, taxes and other payments) of an average home is “tens of percent higher than rent in the area”.

The survey also shows that “in the Rally-Durham area in North Carolina the gap was 42% and in Miami in Florida and Austin in Texas the gap was 30%. There were also big gaps in Denver, Colorado and Nashville in Tennessee.” Even in Chicago where the real estate market has never been particularly hot, the “ownership premium” stood at 23%.

“The Fed could lead to negative leverage”

The significance of this gap is explained by economist Or Shai of Flex Capital Group, which specializes in real estate development and investment in Florida. The return, known as ‘cap rate’ (the net income divided by the value of the property), and the interest rate on the financing, “says Shai.” Because real estate investments are built on significant leverage, this ratio is the standard for calculating the viability of the investment, “he adds.

According to Shai, the Fed’s measures could lead to a situation of negative leverage when the interest on the debt is greater than the rate of return on the property. “Similar to bonds in properties, when the price of the property rises, the yield decreases, and vice versa when the price falls.” “The interest paid on government bonds and the return on assets is a major factor that drives the amount of investment in assets.”

Shai cites the residential property rental sector as an example of this phenomenon. In the last five years, this sector has yielded a national average discount rate of about 5.2% and in some geographical areas it has even dropped from 4.5%. “With the rise in interest rates, the sector finds itself in a situation where the spread between the discount rate and the interest rate has narrowed and even crossed the negative ratio threshold at times.

“This is a perfect storm built on rising interest rates, reducing the amount of debt available in the monetary system and inflation hurting the purchasing power of households, including the rise in other debt maintenance costs,” says Shai, who concludes that ” The Fed will keep its word, the new credit environment will be reflected in the value of assets and their price in the market, and this may create opportunities to buy assets at a low, and “under pressure” investments will begin to appear in the market in the coming quarters.

The rise in interest rates changed the financial model

Rising interest rates have suddenly changed the entire financial model in the US real estate market. Rental house prices and yields versus financing costs have led to a situation where in most America, rental income will not cover the cost of the mortgage plus taxes and maintenance. This gap is only expected to increase They will fix themselves soon, and the Fed will continue to raise interest rates.

At the same time, yields on government bonds, the alternative, are slowly climbing and they will continue if the Fed keeps its promises to reduce its balance sheet. An interest rate environment of 5.8% on 30-year mortgages, together with a yield of 3.5% on government bonds, will require a price reduction of between 20 and 30 percent, depending on the region, in order for institutional investment in residential real estate to be interesting and competitive again. This is because continued inflation and the developing recession (Fed estimates are that for the second quarter the economy has shrunk by over 2%) ensure that this gap will not close through increases in rents.

The effect of the rise in interest rates has already begun to give its signals on the mortgage market. According to Atom, a company that consolidates data from real estate markets in America, in the first quarter of 2022 the demand for mortgages fell by 18% from the last quarter of 2021, and by 32% compared to the first quarter of 2021, the largest decline since 2014.

Preserving faith is critical to the success of the Fed

According to Fed Chairman Jerome Powell, the bank is determined to bring inflation back to 2%. “You have to believe that we will do so,” he said at a Senate hearing last week. , Which could lead to a complete loss of control. To that end, Powell is willing to take big risks. In response to a question from one of the senators whether his policy could “fall off the cliff and crash,” he openly replied that “this is not our intention, but it is certainly a possibility.”

The determination shown by the Fed will undoubtedly continue to exhale from the balloon of assets, and the decline in house prices will lead to the deflation in property prices for ordinary households as well.

This month, the Fed announced two milestones in debt. In the first quarter of this year, the debt of the American economy crossed the $ 90 trillion line, and the debt of the federal government crossed the $ 30 trillion line.

As credit and the amount of money shrink, more and more assets will fall in value, many below the debt taken to purchase them. This could be the beginning of a large asset deflation, in which very large amounts of debt and assets will be written off. After all, an economy built on a constant increase in debt and the amount of money cannot stop growing in order to stop inflation without feeling a real impact on the other side of the equation, i.e. liquidity, debt maintenance and asset value.

Now it remains only to wait and see if the Federal Reserve will muster courage and lead the economy to the great deflation of assets or will it scare the demons out of the bottle and return to respect for policies of expansion, negative interest rates and inflation.