Across the African continent, a quiet but risky shift is occurring in how nations manage their balance sheets. Faced with a brutal combination of soaring global interest rates and crashing local currencies, several African governments are turning to complex derivatives to manage their borrowing costs and hedge against financial volatility.

For years, the standard playbook for emerging markets was straightforward: issue sovereign bonds in US dollars or euros. But as the US Federal Reserve maintained high rates to combat inflation, the cost of servicing that dollar-denominated debt skyrocketed. Now, finance ministries are increasingly utilizing “synthetic” borrowing—using derivatives like currency and interest rate swaps—to lower immediate payments or protect themselves from further currency devaluation.

While these tools can provide essential breathing room for cash-strapped treasuries, they introduce a layer of opacity and risk that often bypasses traditional parliamentary oversight. By shifting the nature of their obligations through private contracts with global banks, some nations are effectively creating “hidden” liabilities that could trigger severe crises if market bets move in the wrong direction.

The mechanics of synthetic borrowing

To understand why African governments are turning to complex derivatives, one must first look at the “original sin” of emerging market finance: the inability to borrow in one’s own currency at reasonable rates. When a country borrows in US dollars but collects taxes in a local currency, any drop in the local exchange rate makes the debt more expensive to pay back.

Derivatives allow governments to essentially “swap” these risks. In a typical cross-currency swap, a government might borrow in a local currency but enter into a contract with a bank to exchange those payments for US dollars at a predetermined rate. This allows the state to lock in costs and avoid the chaos of a volatile foreign exchange market.

Other nations are using interest rate swaps to convert floating-rate debt—which becomes more expensive as global rates rise—into fixed-rate debt. In a high-rate environment, these deals can make a government’s debt profile look more stable on paper, even if the underlying risk remains high.

| Feature | Traditional Eurobonds | Derivative-Linked Borrowing |

|---|---|---|

| Transparency | High (Public Prospectus) | Low (Private Contracts) |

| Cost Structure | Market-driven Coupons | Customized Swap Rates |

| Primary Risk | Default/Credit Rating | Counterparty/Market Volatility |

| Oversight | Legislative/Public | Treasury/Central Bank |

The danger of hidden liabilities

The primary concern for economists and international monitors is the lack of transparency. Unlike a bond issuance, which is registered and public, derivative contracts are often bilateral agreements between a government and a private investment bank. This means the full extent of a country’s obligations may not appear in official debt statistics.

The International Monetary Fund (IMF) has repeatedly warned that “hidden debt” in emerging markets can lead to sudden, destabilizing shocks. When a derivative trade goes against a government, it may be required to post “collateral”—immediate cash payments—to the bank. For a country already struggling with liquidity, these margin calls can trigger a sudden fiscal crisis.

these deals often rely on the stability of the counterparty. If a major global bank faces its own systemic crisis, the “hedge” a government thought it had in place could vanish, leaving the state exposed to the very volatility it sought to avoid.

A systemic struggle for sustainability

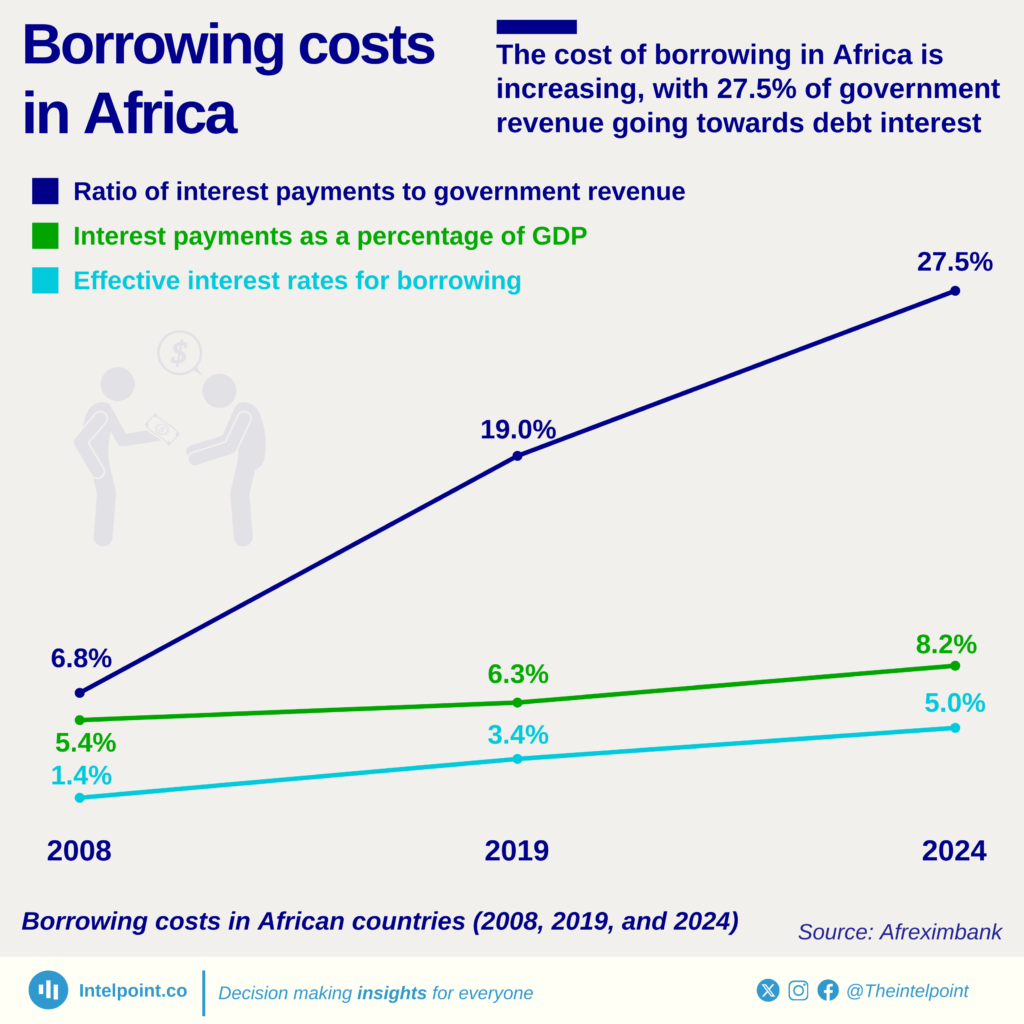

This turn toward complex financial engineering is not happening in a vacuum. It is a symptom of a broader debt crisis across Sub-Saharan Africa. According to World Bank data, many nations in the region are currently at high risk of, or already in, debt distress.

The struggle is compounded by the slow pace of the G20 Common Framework, the global mechanism designed to help poor countries restructure their debt. Because the framework requires consensus between traditional lenders (like the Paris Club) and newer lenders (like China), the process has been agonizingly slow. In the absence of a comprehensive restructuring deal, governments are forced to find “creative” ways to keep the lights on and avoid formal default.

Stakeholders affected by this trend include:

- Domestic Taxpayers: Who may face austerity measures if derivative bets fail and lead to sudden payment spikes.

- International Investors: Who may be blindsided by “hidden” debt that affects a country’s actual creditworthiness.

- Multilateral Lenders: Who must now audit complex private contracts before approving modern rescue loans.

The path forward

The use of these instruments highlights a fundamental gap in the global financial architecture. While derivatives are standard tools for corporate treasuries, their use by sovereign states with limited oversight creates a systemic vulnerability. Experts suggest that moving toward greater transparency—requiring all derivative contracts to be reported to a central registry—is the only way to prevent a repeat of past financial collapses.

For now, the eyes of the market remain on the upcoming debt review cycles of the IMF and the progress of the G20’s efforts to streamline restructuring. The next major checkpoint will be the next series of annual Article IV consultations, where the IMF will evaluate the fiscal health and “hidden” obligations of distressed member nations.

Disclaimer: This article is for informational purposes only and does not constitute financial, investment, or legal advice.

Do you think greater transparency in sovereign debt is possible in the current geopolitical climate? Share your thoughts in the comments or share this story with your network.