Global markets are currently navigating a precarious balance, oscillating between the fragile hope of a diplomatic truce in the Middle East and a surge of strategic corporate restructuring. Even as a temporary cooling of tensions between the U.S. And Iran has provided a momentary sigh of relief for investors, the underlying volatility remains high, leaving analysts to scrutinize where the real value lies beneath the surface of geopolitical instability.

For those tracking the current landscape, the primary focus is on i mercati camminano sul filo del rasoio tra tregua in Iran, m&a e banche europee, a combination of factors that is redefining risk appetite for the coming quarters. The tension is most visible in the energy sector, where the threat of supply disruptions continues to clash with a market that is eager to price in a de-escalation.

However, the narrative is not solely one of risk. A significant shift is occurring in European finance, where banks are transitioning from a period of defensive caution to a more aggressive, growth-oriented posture. This resurgence is being driven by a combination of favorable interest rate environments, structural cost reductions via artificial intelligence, and a substantial amount of excess capital ready for deployment.

As we analyze the current state of play, the divergence between “safe haven” assets and growth opportunities has become more pronounced. From the volatility of the Brent crude price to the tactical shifts in gold holdings, the roadmap for investors is no longer a straight line, but a series of calculated bets on stability and corporate transformation.

The European Banking Renaissance and Capital Deployment

The European banking sector is currently experiencing a surprising revival, emerging as a focal point for analysts who see a rare alignment of growth and value. According to data from Citi, earnings for these institutions have been revised upward by approximately 3% since the start of the year, a trend that stands out in a broader market where positive revisions are increasingly scarce.

Several structural drivers are fueling this optimism. First, the interest rate environment remains supportive; expectations for potential rate hikes by the European Central Bank (ECB) have been reinforced by the geopolitical tensions in Iran, which often exert upward pressure on inflation. Second, the integration of AI is no longer theoretical; it is beginning to deliver measurable improvements in operational productivity and cost management.

Perhaps most critical is the issue of excess capital. European banks are generating significant cash reserves, providing them with the flexibility to pursue several strategic paths:

- Share Buybacks: Returning value to shareholders through aggressive repurchases.

- Mergers and Acquisitions (M&A): Using surplus liquidity to consolidate market share or enter latest territories.

- Dividend Increases: Leveraging strong balance sheets to improve yield attractiveness.

Despite a recent rally, many analysts argue that valuations remain attractive, suggesting that the sector is still undervalued relative to its earning potential.

Energy Volatility: The Hormuz Chokepoint and the Brent Outlook

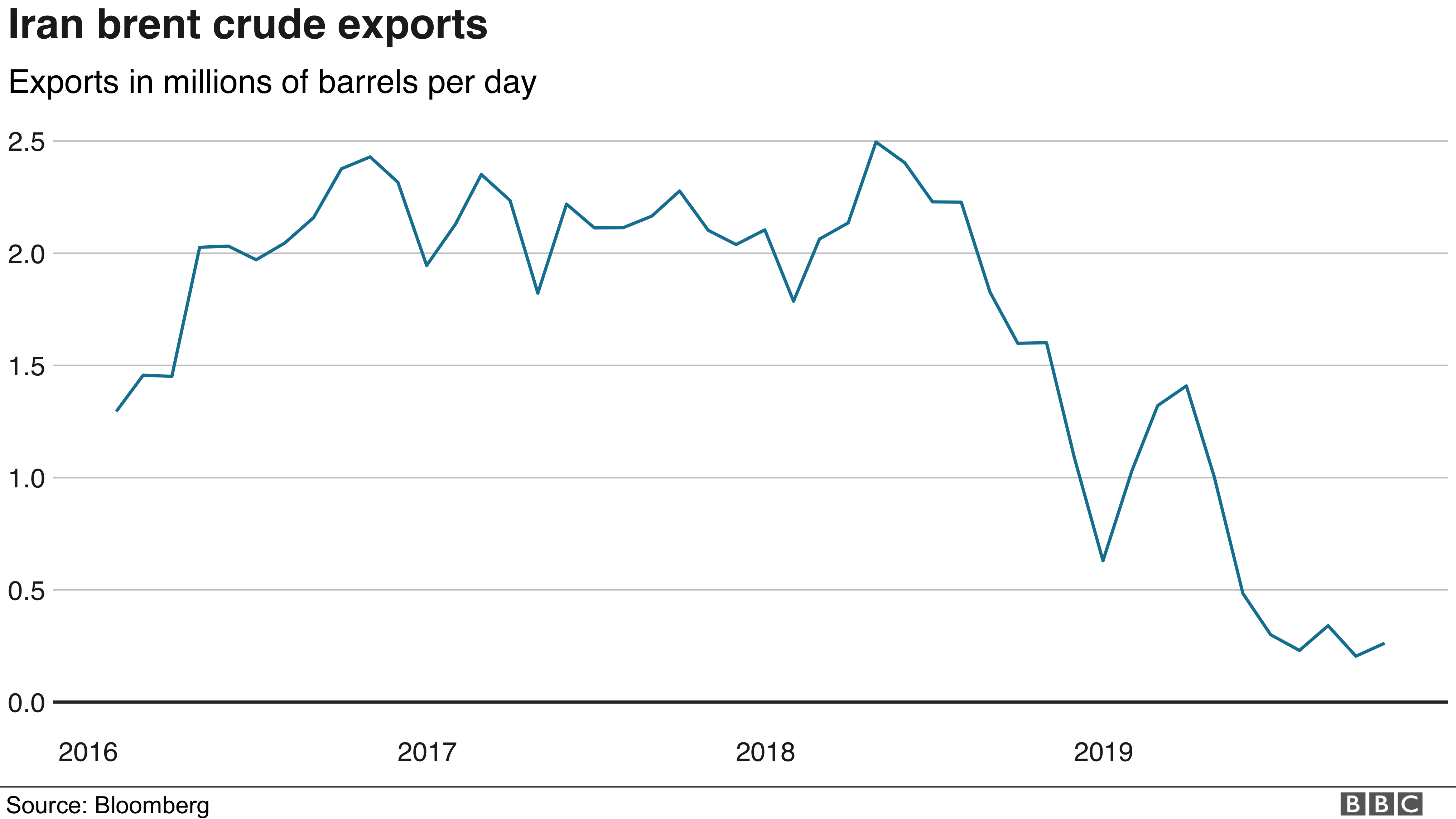

While the financial sector finds its footing, the energy market remains on a knife-edge. The Strait of Hormuz, the world’s most critical artery for oil transit, has seen a dramatic collapse in traffic. Pre-conflict flows of approximately 20 million barrels per day have plummeted to just 2-3 million, with a symbolic low of only 15 tankers in transit following the April 7 ceasefire.

The market is currently attempting to price in a two-week truce between the United States and Iran, leading to a temporary dip in prices. However, this optimism is tempered by the reality of damaged infrastructure. Attacks on Saudi facilities have effectively removed 600,000 barrels per day from global production capacity.

The implications for the global oil market are severe. Experts warn that if transit levels in the Strait of Hormuz remain at their current depressed levels, the Brent crude price could potentially spike toward 190 dollars per barrel, creating a massive inflationary shock that would counteract any gains made by the current truce.

Market Impact Summary: Energy and Commodities

| Asset | Primary Driver | Current Sentiment |

|---|---|---|

| Brent Oil | Hormuz transit collapse / Saudi infrastructure damage | High Risk / Bullish Potential |

| Gold | Turkish central bank sales / ETF outflows | Tactical / Volatile |

| US Dollar | US-Iran negotiations / Fed-ECB divergence | Bearish / Underweight |

Corporate Transformation: From Industrial Shifts to Media Mega-Mergers

Beyond macro-economics, a wave of “transformative” corporate moves is reshaping the industrial and entertainment landscapes. In the automotive sector, Brembo is eyeing a strategic expansion in the United States. The group is reportedly evaluating the acquisition of Tenneco’s suspension division for over 1 billion euros. This move would grant Brembo access to a high-tier client base, including Mercedes, BMW, and Stellantis, and a foothold in the “intelligent suspension” and aftermarket segments.

However, analysts caution that such a deal could be dilutive to margins in the short term, requiring significant synergies to be fully absorbed by the market. A similar tension between ambition and execution is evident in the music industry. Bill Ackman’s Pershing Square has proposed a massive 55-billion-dollar merger between Universal Music Group and Sparc, which would include moving the listing from Amsterdam to New York.

The offer includes a premium of nearly 80% to revalue the label, but the deal hinges on the approval of major shareholder Vincent Bolloré. Without his consent, the proposal remains a speculative venture rather than a guaranteed transformation.

The Tactical Shift in Safe Havens: Gold and Currency

The traditional role of gold as an “eternal” safe haven is being challenged, transforming it into a tactical asset. The market was recently shaken when Turkey sold approximately 20 billion dollars in gold to defend the lira, contributing to the metal’s worst monthly performance since 2008. This coincided with profit-taking by other central banks and significant outflows from gold ETFs, although China has used these dips as an opportunity to increase its reserves.

Simultaneously, the US dollar has weakened as the market weighs the outcome of US-Iran negotiations and the diverging monetary policies of the Federal Reserve and the ECB. Investment firms like Invesco have maintained an underweight position on both the greenback and the British pound, suggesting that the current environment favors a more diversified approach to currency exposure.

Disclaimer: This article is for informational purposes only and does not constitute financial, investment, or legal advice.

The next critical checkpoint for the markets will be the publication of first-quarter 2026 results, with companies like Campari expected to report growth around 5%, potentially outperforming competitors due to their premium positioning. Investors will also be closely monitoring the official diplomatic channels regarding the permanence of the Iran-US truce.

We invite you to share your perspective on these market shifts in the comments below or share this analysis with your professional network.