The battle for the future of generative AI is shifting from a race of technical benchmarks to a war of attrition fought in app stores and balance sheets. While the industry remains crowded with contenders, the gap in consumer adoption is widening, leaving some of the most hyped projects struggling to find a foothold.

Recent data from Sensor Tower indicates that OpenAI continues to hold a commanding lead in user acquisition. In the Apple App Store’s download charts, ChatGPT remains the primary destination for AI users, followed by Google’s Gemini and Anthropic’s Claude. This hierarchy suggests that while Gemini falls behind ChatGPT in terms of raw momentum, the real struggle is happening further down the list.

xAI’s Grok, the AI venture backed by Elon Musk, has struggled to penetrate the top tier of the market. While it has managed to appear in the App Store rankings—sitting around 22nd place in some metrics—it remains far removed from the “big three” of OpenAI, Google, and Anthropic. Similarly, Microsoft’s Copilot, despite being deeply integrated into the Windows ecosystem, has not mirrored ChatGPT’s explosive standalone app growth.

The Staggering Cost of Intelligence

The disparity in user numbers is only one side of the coin. Behind the interfaces lies a financial requirement that is unprecedented in the history of software development. For the private leaders of the field, the cost of maintaining a competitive edge is becoming a liability.

According to reporting from The Wall Street Journal, OpenAI is projecting an astronomical spend of $121 billion on computing power for AI research by 2028. The financial projections are stark: the company anticipates a burn rate of approximately $85 billion in a single year, even as it scales its revenue. This level of spending on infrastructure and GPU clusters represents a burn rate that has no historical parallel in the tech industry.

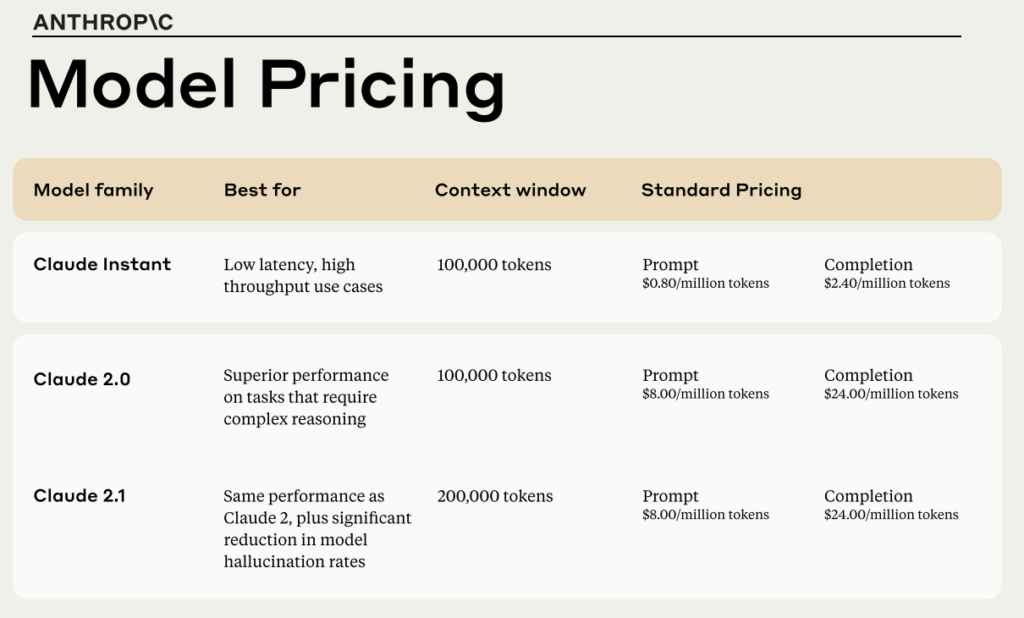

Anthropic is facing similar, though slightly less extreme, pressures. As a primary competitor to OpenAI, Anthropic must similarly invest billions into the compute power necessary to train its next generation of Claude models. This creates a precarious dependency on continuous capital infusions, making the prospect of an Initial Public Offering (IPO) a strategic necessity rather than a mere growth milestone.

Cash Reserves vs. Capital Markets

The competition is currently split between two distinct financial models: the “money machines” of Big Tech and the venture-backed startups. This divide determines how these companies can weather the current “compute crunch.”

Alphabet, the parent company of Google, operates from a position of immense strength. As of its most recent financial filings, Alphabet maintains a treasury of cash, cash equivalents, and marketable securities exceeding $100 billion. This allows Google to fund the development of Gemini internally, absorbing the massive costs of AI research without the immediate pressure to satisfy venture capitalists or public shareholders through a sudden IPO.

In contrast, OpenAI and Anthropic must navigate the volatility of the public markets to sustain their growth. Their ability to raise capital in the coming years will likely dictate their market share. While OpenAI has sought valuations that reflect its dominant market position, the sustainability of such figures depends on whether the company can convert its massive user base into a high-margin, sustainable business model.

| Company | Primary Funding Source | Financial Strategy |

|---|---|---|

| Google (Gemini) | Internal Cash Flow | Direct allocation from Alphabet reserves |

| OpenAI | VC / Strategic Partners | High-burn growth targeting future IPO |

| Anthropic | VC / Strategic Partners | Focused research funding. IPO path |

| xAI (Grok) | Private Equity / Musk Ecosystem | Integration with X and private capital |

The Ecosystem Wild Card

Beyond the direct funding of the AI labs, the industry is seeing a complex web of “indirect” investment. NVIDIA, the provider of the H100 and B200 chips that power these models, has become more than a vendor; it is a strategic stakeholder in the sector’s success. Financial firms are increasingly stepping in to build the physical data centers required for these models, effectively shifting some of the infrastructure risk onto different balance sheets.

For xAI, the path to scaling is inextricably linked to Elon Musk’s other ventures. The company has leveraged massive compute clusters—such as the “Colossus” cluster—to accelerate training. However, without the standalone app adoption seen by ChatGPT or the deep corporate integration of Gemini, Grok remains a niche product primarily tethered to the X platform.

As the industry moves toward 2025, the focus will shift from who has the most capable model to who can afford to keep the lights on. The “compute war” has evolved into a test of financial endurance. For the private players, the goal is to reach a level of broad, indispensable appeal before their capital reserves evaporate.

The next critical checkpoint for the industry will be the upcoming quarterly earnings reports from Alphabet and Microsoft, which will reveal how much of the AI investment is translating into actual revenue growth and whether the burn rates of their partners remain sustainable.

Do you think the massive spending on AI compute will pay off, or are we seeing a financial bubble? Share your thoughts in the comments below.

Related reading