The global energy market is currently witnessing a rare and volatile decoupling. Whereas the high-profile futures contracts that dominate financial headlines are beginning to cool, the actual, tangible market for oil is overheating. In a stark divergence, physical crude hits record highs as the industry grapples with a severe supply crunch that paper trading has yet to fully absorb.

For most observers, the health of the oil market is judged by the daily fluctuations of Brent or West Texas Intermediate (WTI) futures. On Tuesday, those benchmarks suggested a moment of stabilization; WTI was trading at $113.7, while Brent slipped to $109.2. However, these figures are increasingly disconnected from the “real-world” cost of securing a barrel of oil for immediate delivery.

In the physical market, the numbers are far more alarming. Dated Brent—the primary benchmark used to price the majority of the world’s physical oil shipments—has surged past $144 per barrel. In some instances, desperate refiners have paid north of $150 per barrel to secure immediate cargoes, reflecting a level of urgency that transcends standard speculative trading.

The Hormuz Bottleneck and the Supply Gap

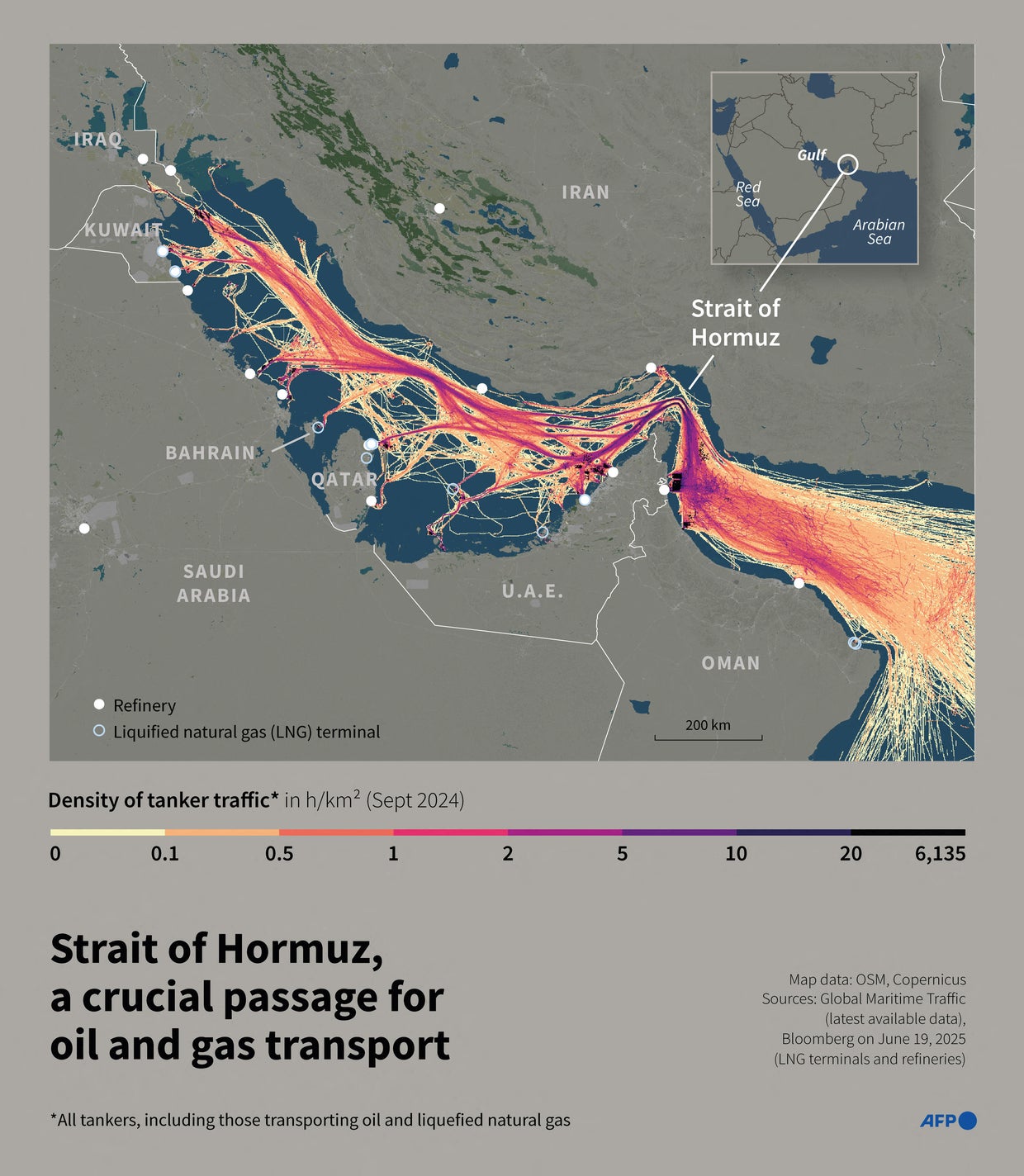

The primary driver of this volatility is a critical disruption around the Strait of Hormuz, the world’s most important oil transit chokepoint. Current market data indicates that at least 12 million barrels per day—representing roughly 12% of total global output—remain effectively shut in. This sudden removal of supply has created a vacuum that cannot be filled by existing inventories.

This is not a crisis of future expectations, but a crisis of immediate access. Because so much of the world’s crude typically flows through the Strait, refiners in Europe and Asia are now forced to scramble for “replacement barrels.” This has shifted the competition toward non-Hormuz sources, specifically those in the North Sea, Africa and the Atlantic Basin.

The result is a bidding war for prompt cargoes—oil that can be loaded and shipped immediately. North Sea Forties crude has already seen record outright prices, and the premiums paid for immediate delivery have spiked. This creates a “backwardation” environment where the current price of oil is significantly higher than the price for delivery months from now, a classic signal of extreme short-term scarcity.

| Metric | Value/Status | Market Context |

|---|---|---|

| Dated Brent (Physical) | $144 – $150+ | Record High / Prompt Demand |

| Brent Futures (Paper) | $109.2 | Cooling / Speculative Pullback |

| WTI Crude (Futures) | $113.7 | Modest Daily Gain |

| Supply Disruption | ~12 Million bpd | ~12% of Global Output |

The Domino Effect on Refined Products

The pressure is not contained within the crude market. Because refineries are paying record premiums for the raw input, those costs are migrating downstream into the products that power transport and heating. In Europe, prices for diesel and jet fuel are currently hovering near record levels, reinforcing a sense of tightness across the entire energy barrel.

This “prompt market” pressure is where the real economic pain is concentrated. According to analysis from Morgan Stanley, the most intense pricing pressure is located in the immediate delivery window. While a trader might be able to hedge a position for six months from now at a lower price, a refinery that needs oil today to keep its plants running has very little leverage.

For the global economy, this means that the “cooling” seen in futures markets is largely an illusion. The cost of doing business—shipping, aviation, and logistics—is tied to the physical price of fuel, not the speculative price of a futures contract. As long as the physical crude hits record highs, the inflationary pressure on refined products will persist.

Who is Most Exposed?

The current crisis creates distinct winners and losers based on geography and infrastructure:

- European and Asian Refiners: These entities are the most exposed, as they rely heavily on the disrupted flows and must now pay steep premiums for Atlantic Basin alternatives.

- North Sea and West African Producers: These regions are seeing a windfall as their crude becomes the primary alternative to Hormuz-linked supply.

- Aviation and Freight Carriers: With jet fuel and diesel prices spiking, the cost of moving goods and people is rising in real-time.

The fundamental question for the market now is whether replacement capacity can be scaled quickly enough to offset the 12 million barrel-per-day deficit. Historically, the International Energy Agency has noted that diverting global shipping routes and sourcing new grades of crude takes weeks, if not months, to stabilize.

Disclaimer: This article is provided for informational purposes only and does not constitute financial, investment, or legal advice.

The market now looks toward the next official update on shipping transit volumes through the Strait of Hormuz and any potential emergency releases from strategic reserves, which could provide the necessary liquidity to ease the prompt market. Until then, the industry remains defined by a desperate search for immediate barrels.

We seek to hear from you. How are these energy shifts impacting your industry or region? Share your thoughts in the comments below.