The anticipation surrounding the potential public debuts of SpaceX, OpenAI, and Anthropic has created a shimmering mirage of market renewal. On the surface, the arrival of these three titans—representing the vanguard of aerospace and artificial intelligence—should be a catalyst for a new bull run. However, a closer look at the plumbing of the global equity markets suggests that the AI and space sector IPOs market impact may be more disruptive than restorative.

The core issue is not a lack of interest, but a potential lack of liquidity. As these companies eye valuations that challenge the scale of the world’s largest corporations, the market faces a fundamental question: where will the capital come from? In an era of volatile energy prices and uncertain interest rates, the arrival of these giants could trigger a cash crunch, forcing investors to sell off established winners to make room for the newcomers.

For years, these companies have existed in a private equity vacuum where valuations are set by institutional investors who appear to have limitless appetites. Unlike traditional public companies, these entities often operate without traditional price-to-earnings multiples, frequently losing significant capital to fuel rapid growth and maintain a competitive lead. Whereas this “growth-at-all-costs” model is tolerated in private rounds, the public market typically demands a clearer path to profitability.

The Liquidity Paradox and the S&P 500

If SpaceX, OpenAI, and Anthropic were to transition to public markets and subsequently be added to the S&P 500, the resulting reallocation would be immense. There is no dormant pool of trillions of dollars waiting on the sidelines specifically for these IPOs. Instead, index funds and institutional portfolios would likely be forced to sell existing holdings to maintain their weighting requirements.

This creates a “zero-sum” dynamic. The rise of generative AI has already begun to erode the valuations of traditional software-as-a-service (SaaS) and enterprise software firms. As investors pivot toward the “destroyers”—the AI models that may render existing software obsolete—the broader market could see a hollowing out of the mid-cap tech sector. The pressure on the market to absorb these deals could be immense, potentially leading syndicate desks to restrict the “float,” or the amount of stock available to the public, to artificially support prices.

| Company | Primary Market Role | Valuation Context | Market Risk |

|---|---|---|---|

| SpaceX | Aerospace/Satellite | High (Secondary markets often cite ~$210B) | Capital intensity of Starship |

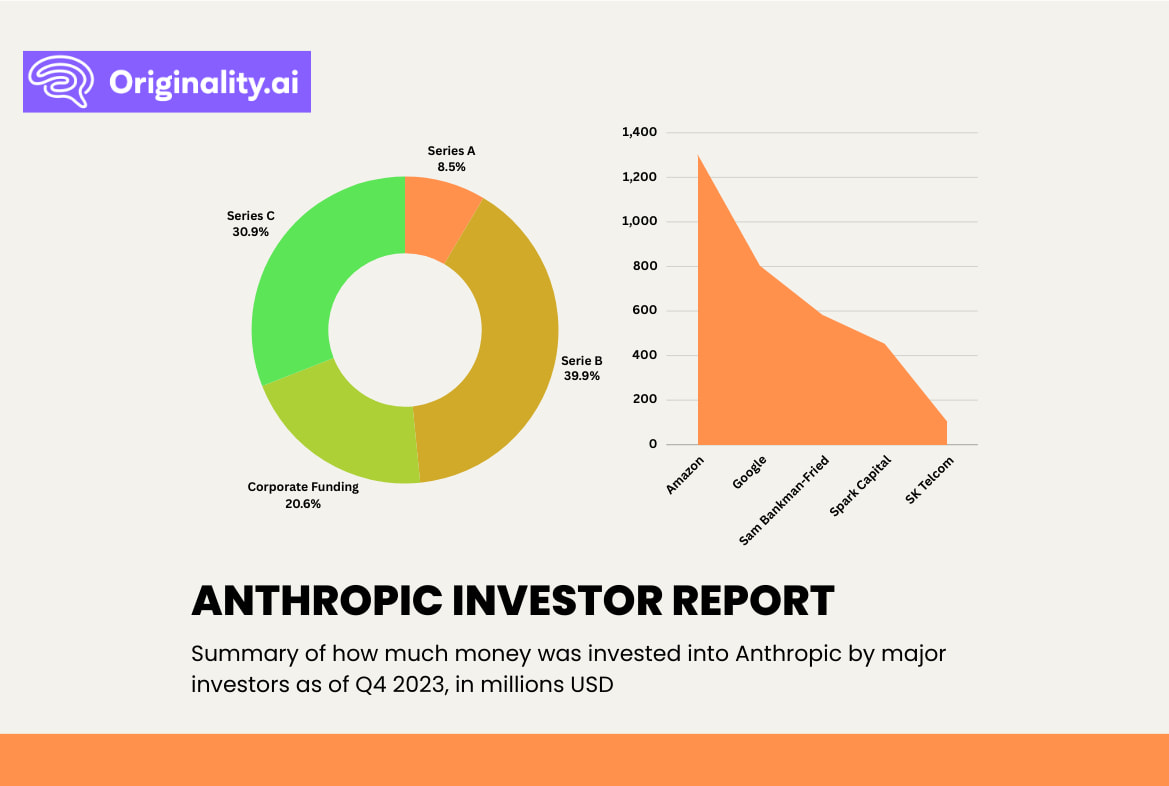

| OpenAI | Generative AI | Extreme (Recent rounds near $157B) | High compute costs; revenue scaling |

| Anthropic | AI Safety/LLMs | High (Rapidly scaling) | Competition with OpenAI/Google |

Geopolitical Drag and the Oil Axiom

The timing of these potential listings is complicated by a fragile geopolitical landscape, particularly in the Middle East. The market remains hypersensitive to the stability of the Strait of Hormuz and the actions of the Iranian regime. Historically, the stock market struggles to sustain an advance when oil prices climb sharply, as energy costs act as a universal tax on both consumers, and corporations.

Recent volatility in U.S. Energy Information Administration (EIA) benchmarks illustrates the inflationary drag of oil. When WTI crude spikes, it doesn’t just affect gas stations; it increases the cost of plastics, aluminum, and transportation, squeezing earnings-per-share across the S&P 500. This inflationary pressure makes it significantly harder for the Federal Reserve to justify rate cuts.

The current political rhetoric has added another layer of uncertainty. The mention of aggressive military strategies—paralleling the “bomb them back to the Stone Age” philosophy associated with General Curtis LeMay during the Vietnam era—suggests a high-risk environment. While some investors hope for a swift resolution to Middle East tensions, the lack of a clear diplomatic off-ramp keeps many institutional players on the sidelines, preferring the safety of cash or short-term treasuries over equity risk.

The Interest Rate Stalemate

Beyond geopolitics, the market is trapped in a waiting game with the Federal Reserve. Many investors are currently comfortable remaining on the sidelines, earning relatively stable returns on cash without exposing themselves to capital risk. Historically cheaper stocks are struggling to find a floor because they cannot rise without a definitive downward trend in short-term rates.

If inflation persists—driven by energy shocks or supply chain disruptions in the Persian Gulf—the possibility of rate hikes, however unlikely, remains a ghost in the machine. A rise in rates would be catastrophic for the high-valuation, non-profitable models that OpenAI and Anthropic currently employ. These companies are essentially bets on the future; when the cost of money increases, the present value of those future earnings drops precipitously.

Who is affected by this transition?

- Retail Investors: May find themselves priced out of the most exciting IPOs if syndicate desks restrict the float.

- SaaS Companies: Existing software firms face “valuation cannibalization” as capital migrates to AI primary movers.

- Institutional Funds: Forced to make difficult “sell-to-buy” decisions to accommodate massive new index additions.

- Global Consumers: Indirectly affected by the inflationary pressure of oil, which limits the overall liquidity available for stock market investment.

the promise of revolutionary technology cannot override the laws of mathematics. The market cannot go up if there is no one left to buy, and it cannot sustain astronomical valuations if the macroeconomic environment is defined by war and inflation. While SpaceX, OpenAI, and Anthropic are undoubtedly transforming their respective industries, their entry into the public markets may be the final stress test for a system already stretched to its limit.

Disclaimer: This article is for informational purposes only and does not constitute financial, investment, or legal advice. Investing in IPOs and volatile sectors involves significant risk.

The next critical checkpoint for the market will be the upcoming Federal Open Market Committee (FOMC) meeting, where any shift in the interest rate trajectory will likely dictate whether the market has the appetite for these massive upcoming deals.

Do you believe the AI boom is creating a sustainable new economy, or is it a liquidity bubble? Share your thoughts in the comments below.