2024-04-27 01:19:40

Substantial business and ‘de minimis’ exemptions are partially implemented, raise the tax burden and lead to economy-wide consequences, TEAM warns

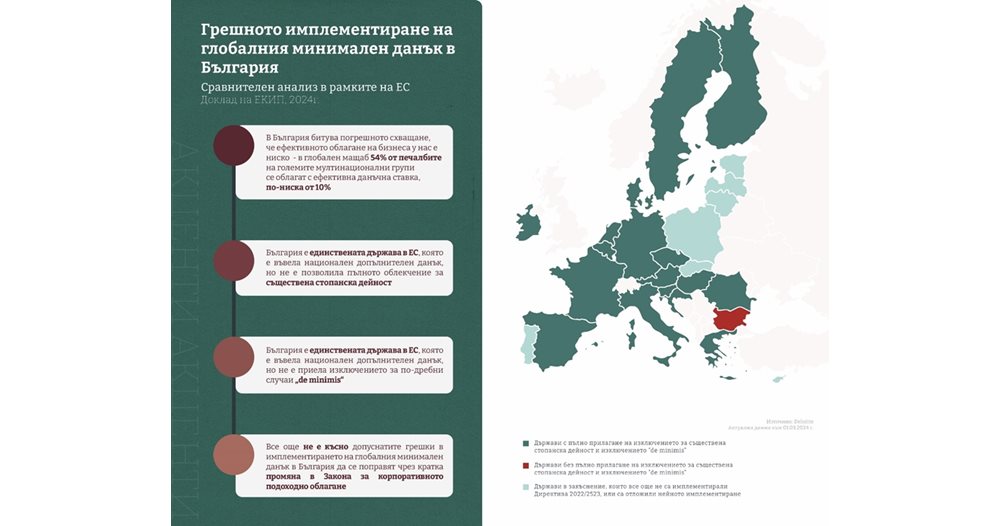

Bulgaria turns out to be the only country in the EU that introduced a national additional tax, popularly known as a global tax on large local and multinational corporations, of 15%, without, however, allowing all the reliefs to be used. This is shown by a study by the Expert Club for Economics and Politics EKIP, announced on their website.

The experts have made a complete review of the regimes for the introduction of the global tax and have found that only in our country two of the reliefs will not work – for essential economic activity and the “de minimis” exception. They are categorical that this puts us in a disadvantageous situation in terms of attracting foreign investments and stimulating the leading Bulgarian industrial groups to international expansion.

It is an indisputable fact that the level of taxation is one of the priorities for attracting significant investments, according to the authors of the study. This fact has been confirmed by almost complete consensus in academic research and recent statements by Western industry partners. In our country, however, the misconception is often heard that the corporate tax of 10% is a low rate and therefore the problem lies elsewhere. Although the barriers to investment are multifaceted, it should be noted that 54% of the profits of large multinational corporate groups are taxed at an effective tax rate of less than 10%. That is, even a flat tax of 10% is higher than the effective rate that international business pays on over half of its profits.

Therefore, the authors of the study recommend that the full package of relief from the global tax of 15% be introduced and that this be one of the priorities of the legislative and executive authorities for this year. They are adamant that this will provide new tools and incentives for the realization of significant investments, which have been lacking in our country in recent years.

This can be done by changing three articles of the Corporate Income Tax Law, which will make us equal and even with tax advantages in attracting multinational investments. The latter is particularly important in view of the processes of outflow of international investments from Europe to the USA and China, and the stagflation in the EU and the Eurozone, which can only be overcome by more investments in the production of goods and services.

The report gives a detailed answer to the question of what is the nature of the reliefs “missed” by the Bulgarian legislators. The first is for substantial economic activity. Both Directive 2022/2523 and the newly adopted texts of the Law on Corporate Income Taxation (CIT) provide for the calculation of the global tax to apply the substantial business exception.Behind this term lies the concept that companies that invest in real business by creating jobs and acquiring tangible assets should not bear an excessive additional tax burden the global minimum tax targets unfair tax practices where corporations take advantage of loopholes and weaknesses in countries’ tax systems, shift profits to lower-tax jurisdictions, or take advantage of multiple tax breaks stated that Bulgaria fully applies the exception for essential economic activity in taxation with primary additional tax, which has very little practical meaning because it affects only 5 large Bulgarian groups. At the same time, we apply a limited exception regarding the national additional tax, which affects about 700 enterprises in Bulgaria, allowing a percentage deduction only from durable tangible assets.

This means that the national additional tax burden will always be higher than the global minimum tax payable in any other country, the authors of the study explain. They are categorical that the chosen policy of imposing an additional tax burden above the minimum required in the EU and the lack of tax relief of practical importance, we risk becoming one of the countries in the EU with the highest level of effective tax burden for the services sector and especially outsourcing and IT.

Similar to the exception for substantial economic activity, the “de minimis” exception applies in Bulgaria only for the purposes of the global tax. However, the idea of ”de minimis” is to give an exception for smaller cases, the TEAM is categorical. Given the extremely voluminous and complex matter of the global minimum tax system, the implementation of the rules is associated with great efforts and administrative costs both on the part of taxpayers and the tax administration itself. Taking into account this need for a balance between the benefits of additional tax revenues and the costs of collecting them, Directive 2022/2523 allows no additional tax to be collected from large groups in countries where the average level of revenue for an enterprise is less than 10 million .euro and the average profit is lower than 1 million euro. However, Bulgaria does not apply the “de minimis” exception. Thus, smaller enterprises, part of large groups located in our country, will not only have a greater effective tax burden, but will also incur unnecessarily greater administrative costs for complying with tax rules. tax, not only exclude smaller cases from its scope, but also respect the “de minimis” thresholds laid down in the directive. This problem concerns all spheres of the economy in which there are smaller Bulgarian subsidiaries that are part of large multinational groups.