The waters surrounding the Muscat Anchorage in Oman often appear still, but for the global economy, they represent one of the most volatile intersections of energy and finance on earth. As oil tankers cluster near the entrance to the Strait of Hormuz, the physical congestion of ships mirrors a growing geopolitical tension that is testing the foundations of the global financial order.

For decades, the “petrodollar” system—the global agreement to price oil in U.S. Dollars—has served as a cornerstone of American economic influence and global market stability. However, escalating frictions involving Iran and the strategic choke points of the Persian Gulf are accelerating a conversation about the petrodollar system stability and whether the world is moving toward a fragmented, multi-currency energy market.

The anxiety is not rooted in a single event, but in a compounding series of pressures. From the threat of maritime disruptions in the Strait of Hormuz to the rise of BRICS-led initiatives for currency diversification, the mechanism that forces the world to hold U.S. Dollars to buy energy is facing its most significant challenge since the 1970s.

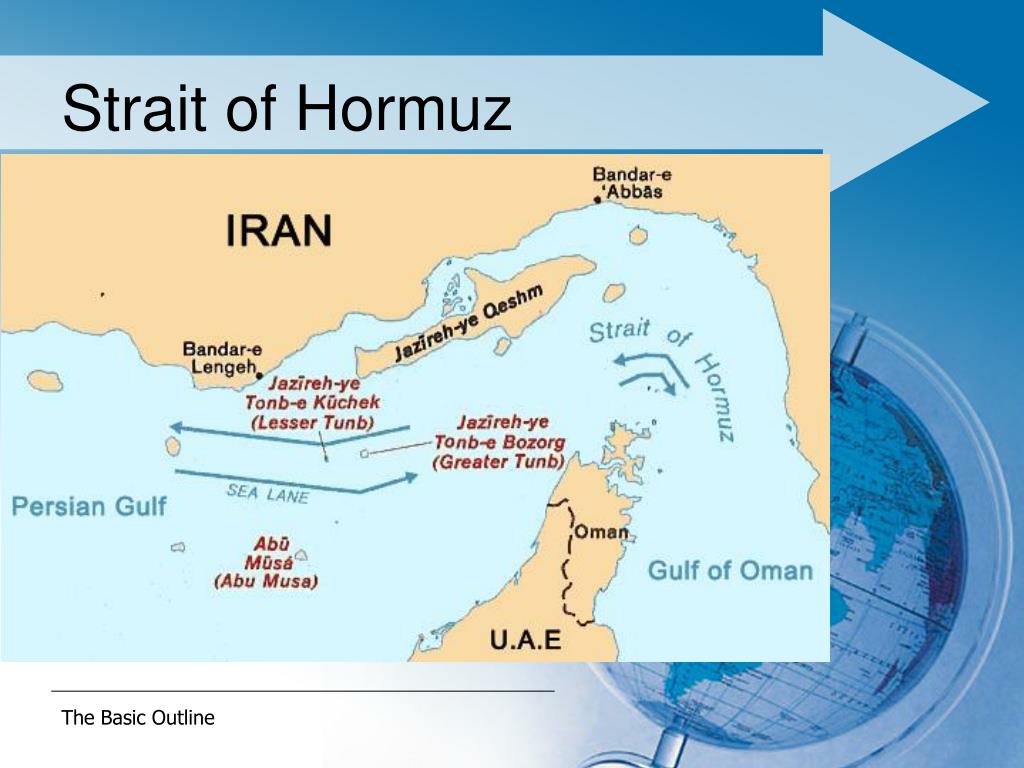

The Strategic Weight of the Strait of Hormuz

The Strait of Hormuz is the world’s most essential oil transit choke point. According to the U.S. Energy Information Administration, roughly one-fifth of the world’s total oil consumption passes through this narrow waterway daily. Any disruption here—whether through military conflict, sanctions enforcement, or Iranian naval activity—immediately injects a “risk premium” into global oil prices.

When tensions rise, the Muscat Anchorage becomes a barometer for global anxiety. Tankers often wait there to time their entry into the Strait, avoiding potential zones of conflict or waiting for security clearances. This physical bottleneck highlights a systemic vulnerability: the world’s energy security is inextricably linked to a region where political stability is perpetually fragile.

This instability does more than raise the price of a barrel of crude; it encourages energy-importing nations to seek hedges against U.S.-led geopolitical volatility. When the U.S. Uses the dollar as a tool for sanctions—as it has extensively with Iran—other nations start to view the dollar not just as a reserve currency, but as a political liability.

De-dollarization and the Shift in Oil Pricing

The petrodollar system relies on a symbiotic relationship: oil exporters sell their resources in dollars and then reinvest those dollars into U.S. Treasuries. This cycle keeps U.S. Borrowing costs low and maintains the dollar’s status as the primary global reserve currency. However, this cycle is beginning to fray.

Several factors are driving this structural shift:

- Currency Diversification: Major importers, particularly China and India, are increasingly settling energy trades in local currencies to reduce their exposure to U.S. Monetary policy and sanctions.

- The BRICS Influence: The expansion of the BRICS bloc has intensified discussions about creating a common trade currency or using a basket of currencies to bypass the dollar in commodity trades.

- Saudi Arabia’s Pivot: Although the U.S. Remains a primary security partner, Saudi Arabia has signaled a willingness to discuss oil payments in currencies other than the dollar, a move that would fundamentally alter the petrodollar’s dominance.

While these shifts are gradual, the friction in the Persian Gulf acts as a catalyst. Every time a conflict threatens the flow of oil, the incentive for nations to build “dollar-free” trade corridors increases.

Analyzing the Impact of Regional Conflict

The discourse surrounding a potential conflict involving Iran often focuses on the immediate spike in oil prices. Yet, the deeper long-term risk is the acceleration of “de-dollarization.” If a conflict were to lead to a prolonged closure of the Strait of Hormuz, the resulting chaos would likely force a rapid transition toward alternative payment systems.

| Feature | Traditional Petrodollar System | Emerging Diversified Model |

|---|---|---|

| Primary Currency | U.S. Dollar (USD) | Multi-currency (CNY, INR, Local) |

| Reserve Asset | U.S. Treasuries | Gold, Diversified Sovereign Bonds |

| Political Risk | U.S. Sanctions Exposure | Fragmented Regulatory Frameworks |

| Market Liquidity | High / Centralized | Variable / Decentralized |

The risk is not necessarily a sudden “collapse” of the dollar, but a gradual erosion of its hegemony. Financial analysts note that the U.S. Dollar still possesses an unparalleled advantage in liquidity and trust. As noted by the International Monetary Fund, the dollar’s role as a reserve currency remains dominant, though the share of non-traditional currencies in global reserves has been climbing.

Who is affected and how?

The stakeholders in this transition are diverse. For the United States, a weakened petrodollar could lead to higher borrowing costs and a diminished ability to project power via financial sanctions. For oil-exporting nations, diversifying currencies reduces their dependence on a single political entity but introduces exchange-rate volatility.

For the average consumer, these high-level financial shifts manifest as volatility at the pump. When the currency used to buy oil fluctuates or the route to transport We see threatened, the cost of energy rises, contributing to global inflation.

Disclaimer: This article is provided for informational purposes only and does not constitute financial, investment, or legal advice.

The next critical checkpoint for the petrodollar’s stability will be the upcoming OPEC+ ministerial meetings, where production quotas and potential shifts in trade agreements are regularly debated. These meetings will provide the first concrete signals on whether the major producers are moving closer to a formal diversification of oil pricing.

We invite you to share your thoughts on the future of global energy trade in the comments below.