Mowi‘s Acquisition of Nova Sea: A Boon for Shareholders, Says Fearnley Securities

Norwegian seafood giant Mowi is set to acquire the remaining shares of fellow salmon farmer Nova Sea, a move analysts at Fearnley Securities believe will considerably benefit Mowi’s shareholders.

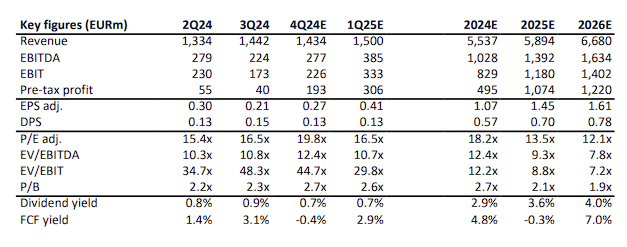

The acquisition,valued at NOK 16 billion (approximately $628.6 million), will give Mowi full control of Nova Sea, a company known for its high-margin operations and top-quality salmon. fearnley Securities has raised its EBIT estimates for Mowi for 2026-27 by 11-13% and EPS estimates by 4-3%,citing the acquisition as a key driver.

The brokerage firm has also increased its price target for Mowi shares to NOK 270 from NOK 244, maintaining its “buy” rating and “favorite” status for the stock.

boosting Volume and Margin

Fearnley Securities highlights several key benefits of the acquisition for Mowi. Firstly, it will significantly boost Mowi’s production volume, potentially allowing the company to reach 600,000 tonnes of salmon production as early as next year. This aggressive growth trajectory aligns with Mowi’s target of reaching 1 million tonnes of production by 2029.

Secondly, the acquisition will enhance Mowi’s overall margin profile, thanks to Nova Sea’s strong operational efficiency and high-quality product. Fearnley Securities estimates a 6% increase in 2026 Farming EBIT/kg for Norway following the acquisition.

Synergies and Future Growth

The analysts also anticipate important synergies from the integration of Nova Sea into Mowi’s operations. While the exact details are yet to be revealed, Fearnley Securities estimates synergies of 34 million euros, a figure they believe is likely conservative.

Further details about Nova Sea’s volume guidance and the full extent of the synergies are expected to be released in the future, potentially leading to further positive market reaction and price recognition for Mowi shares.

Mowi’s Strong Track Record

Fearnley Securities points to Mowi’s consistent track record of meeting its production guidance as a key factor in their bullish outlook. The company’s ability to deliver on its promises instills confidence in the analysts’ projections for future growth.

risks and Opportunities

While the analysts are optimistic about the acquisition, they acknowledge that the primary risk factor remains biological performance. mowi’s share price is currently trading below its 10-year average, suggesting the market is already factoring in some potential for biological challenges.

However, Fearnley Securities believes Mowi is priced attractively and maintains its ”buy” recommendation.

Time.news Editor: We’re seeing a lot of buzz around Mowi’s recent acquisition of Nova Sea. For our readers who may not be familiar, can you break down why this move is generating so much excitement in the investment community?

Expert: Absolutely.Mowi, a leading player in the global salmon farming industry, has secured the remaining shares of Nova Sea, boosting its total ownership to 95%. This deal comes as a major positive for Mowi’s shareholders, as highlighted by Fearnley Securities, a reputable financial analysis firm.

Time.news Editor: Why is Fearnley Securities so bullish on this acquisition?

Expert: There are several compelling reasons. First, Nova Sea is known for its high-margin operations and produces top-quality salmon. Integrating Nova Sea’s strengths into Mowi’s existing portfolio will significantly enhance Mowi’s overall profitability and market standing.

secondly, the acquisition significantly boosts Mowi’s production volume.Fearnley Securities projects Mowi could reach 600,000 tonnes of salmon production as early as next year, putting them well on track to achieve their ambitious target of 1 million tonnes by 2029.

Time.news Editor: This sounds like a recipe for growth. Are there any other anticipated benefits?

Expert: Yes, there’s a strong expectation of notable synergies from merging the two companies. While the exact details haven’t been fully disclosed, Fearnley Securities estimates these synergies could reach 34 million euros, and they believe this is highly likely conservative.

Time.news Editor: What are the potential risks that investors should be aware of?

Expert: As with any major investment, there are always risks. Fearnley Securities acknowledges that biological performance remains a key factor. Fluctuations in factors like disease outbreaks or changes in water conditions can impact production outputs and profitability. The market currently seems to be factoring this risk into Mowi’s share price, which is currently trading below its 10-year average.

Time.news Editor: Given these factors, what is your overall advice for potential investors?

Expert: Despite the inherent risks, Fearnley Securities believes Mowi is attractively priced and maintains a “buy” recommendation for the stock.